PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1432887

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1432887

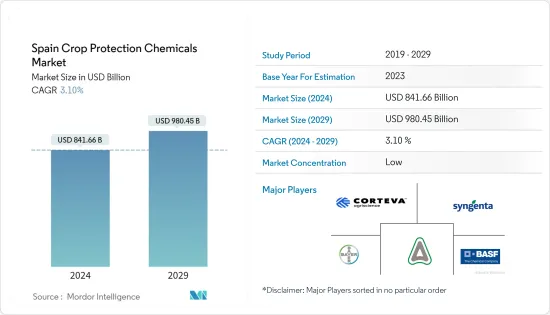

Spain Crop Protection Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

The Spain Crop Protection Chemicals Market size is estimated at USD 841.66 billion in 2024, and is expected to reach USD 980.45 billion by 2029, growing at a CAGR of 3.10% during the forecast period (2024-2029).

Key Highlights

- In Spain, food security and safety have become a major concern over the last few years. Therefore, the biological control of insect pests in the agricultural field has gained importance in the recent past, especially due to food safety and environment-friendly nature. In this regard, bacterial insecticides offer better alternatives to chemical pesticides. Thus, the market for bioinsecticide is anticipated to grow at a significant pace during the forecast period.

- Bayer CropScience AG, BASF SE, Adama LTD, and Syngenta Internation AG are some of the major players operating in this market.

Spain Crop Protection Chemicals Market Trends

The rise in Adoption of Biopesticides

The use of biopesticides is fully aligned with the current trend that promotes healthy eating without neglecting environment conservation. There is a growing interest in Spanish consumers to eat residue-free food. This is quite reflected in an increase in area under organic cultivation in the region. In 2018, the area under organic farming had increased from 2.24 million hectares as compared to its 2.01 million hectares in 2016, as reported by the Research Institute of Organic Agriculture (FiBL) statistics. By crop type, organic grapes are cultivated around a total of 106,000 hectares in the region. The growth in the biopesticides market is further supported by technological developments undertaken in the segment. Many regional companies, such as Seipasa, are investing in their R&D activities to develop new biological crop protection solutions to improve the efficiency of these products.

Insecticides Dominating the Market

There is a growing demand for insecticides in the region due to a rise in the number of yield losses caused due to insects. Cereals and fruits corner the highest share of insecticide usage in the region. According to FAO, during the period 2015-16, the insecticide share in the overall pesticide use has significantly increased from 11.6% in 2015 to 12.3% in 2016. Pyrethroids are the most commonly used insecticide active ingredients in the country in 2016, totaling 118 metric tons. A significant decline of nearly 57.2%, in the usage of pyrethroid active ingredient, has been evident, especially owing to the impact of restrictions on neonicotinoid and fipronil insecticides on pest management in maize, oilseed rape and sunflower crops. This decline in usage of other classes of insecticides plummeted the sales of pyrethroid based insecticide products in the country.

Spain Crop Protection Chemicals Industry Overview

Spain's crop protection chemical market is highly competitive, with the presence of many regional and international players operating in the market. Bayer CropScience AG, BASF SE, Adama Ltd, and Syngenta Internation AG are some notable players having their presence in the region. These players have an extensive distribution network and are making collaborations with local players, which gives them a competitive edge over other players in the market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porters Five Force Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Origin

- 5.1.1 Synthetic

- 5.1.2 Bio-Based

- 5.2 By Type

- 5.2.1 Herbicide

- 5.2.2 Fungicide

- 5.2.3 Insecticide

- 5.2.4 Other Types

- 5.3 By Application

- 5.3.1 Grains and Cereals

- 5.3.2 Pulses and Oilseeds

- 5.3.3 Fruits and Vegetables

- 5.3.4 Commercial Crops

- 5.3.5 Other Applications

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Bayer CropScience AG

- 6.3.2 BASF SE

- 6.3.3 FMC Corporation

- 6.3.4 Corteva Agriscience

- 6.3.5 Sumitomo Chemical Co., Ltd (Kenogaurd)

- 6.3.6 Syngenta International AG

- 6.3.7 Adama LTD

- 6.3.8 Novozymes Biologicals

7 MARKET OPPORTUNITIES AND FUTURE TRENDS