PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1906897

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1906897

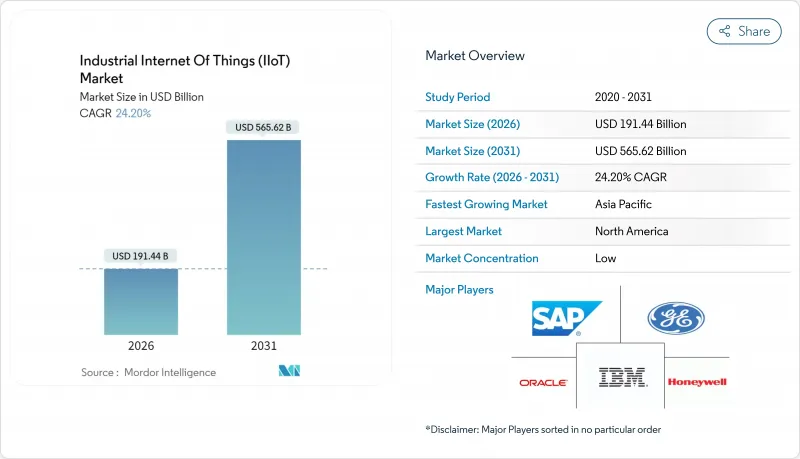

Industrial Internet Of Things (IIoT) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The industrial internet of things market is expected to grow from USD 154.14 billion in 2025 to USD 191.44 billion in 2026 and is forecast to reach USD 565.62 billion by 2031 at 24.2% CAGR over 2026-2031.

The growth trajectory reflects a sharp decline in sensor prices, wider private-5G roll-outs, and chiplet-based edge-AI designs that allow real-time analytics at the point of operation. Manufacturers are accelerating deployments to move from reactive to predictive maintenance, improve overall-equipment-effectiveness, and cushion supply-chain shocks. Cloud resources remain pivotal for fleet-wide analytics, yet hybrid edge-cloud architectures are being favored for latency-sensitive control loops. Competitive dynamics reveal stronger collaboration between operational-technology vendors and cloud hyperscalers as outcome-based service models become the norm.

Global Industrial Internet Of Things (IIoT) Market Trends and Insights

Integration of Advanced Sensors and Falling Device Costs

Unit-level sensor prices keep falling while embedded processors add neural acceleration, enabling AI-ready devices such as STMicroelectronics' STM32N6 MCU that runs in-situ inference without a discrete accelerator. Manufacturers, especially in brownfield plants, now blanket legacy assets with non-intrusive sensors instead of complete system swaps. Low-power wide-area options like LoRaWAN extend coverage to remote assets, and smart-sensor self-diagnostics feed lifetime event logs into analytics hubs. Expanded visibility drives stronger return-on-investment cases, speeding projects that previously stalled due to retrofit costs. Consequently, the industrial internet of things market enjoys a larger addressable base among cost-sensitive mid-tier factories.

Push for Predictive Maintenance and OEE Improvement

Operations heads see unplanned downtime as a strategic liability. Continuous condition data equips machine-learning models that flag anomalies weeks in advance, cutting unscheduled stoppages by double-digit percentages. Vibration, thermal, and acoustic signatures guide maintenance crews toward prioritized tasks, freeing scarce labor for higher-value assignments. Digital-twin overlays simulate service scenarios across multiple lines, optimizing spare-parts inventory and technician dispatch. In process industries, every avoided shutdown saves millions in lost throughput, explaining why predictive systems draw premium budgets despite capital discipline.

OT Cybersecurity and Legacy System Vulnerabilities

Industrial-control gear that predates the internet now sits on converged networks, enlarging the attack surface. Extended equipment lifecycles mean patches may never be issued, leaving PLCs exposed. Departments sometimes install unvetted IoT nodes, creating "shadow OT", that bypass central security controls. Low-code development platforms accelerate application rollout but, without governance, can propagate insecure code. Operators must weigh production gain against cyber risk, often delaying internet-connected upgrades until layered defenses and zero-trust frameworks are in place.

Other drivers and restraints analyzed in the detailed report include:

- Government-backed Smart-Manufacturing Initiatives

- Private 5G Campus Networks in Heavy Industry

- Lack of Cross-Vendor Interoperability Standards

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware retained 46.15% of industrial internet of things market share in 2025, anchored by sensors, gateways, and industrial PCs. Sensors and actuators form the backbone of condition monitoring, while edge gateways pre-process telemetry to manage bandwidth. However, Services and Connectivity is registering a 25.12% CAGR, underlining how integration pain points are reshaping procurement decisions. Professional-service teams retrofit brownfield assets to modern protocols, and managed offerings attract mid-market factories that lack in-house OT-IT talent.

In practice, hardware vendors increasingly bundle device-management portals and remote-monitoring subscriptions, blurring product-service boundaries. Systems integrators earn annuities from operating the infrastructure they once commissioned. As low-code dashboards become mainstream, operational teams build custom visualizations without coding, reducing reliance on enterprise IT. The industrial internet of things market thus gravitates toward life-cycle partnerships rather than one-time capital purchases.

Cloud platforms accounted for 52.91% of industrial internet of things market size in 2025 by offering elastic analytics at lower upfront cost. Yet pure cloud cannot meet sub-10-millisecond control requirements; hence, hybrid edge-cloud deployments are growing at 25.28% CAGR. Manufacturers process vibration spectra or machine-vision frames on-site and forward aggregated insights to the cloud for fleet-level optimization.

Private-5G backbones accelerate this fusion by providing deterministic, low-latency uplinks. Containerized microservices let engineers drop AI modules anywhere along the compute continuum, conforming to data-sovereignty rules in pharmaceuticals and defense. On-premises only models persist in niche, high-regulation niches, but hybrid architectures are expected to become the default for next-generation roll-outs in the industrial internet of things market.

The Industrial Internet of Things Market Report is Segmented by Component (Hardware, Software, and Services and Connectivity), Deployment Model (On-Premises, Cloud, and Hybrid/Edge-Cloud), Connectivity Technology (Wired, Short-Range Wireless, Cellular, and LPWAN), End-User Vertical (Discrete Manufacturing, Process Manufacturing, Oil and Gas, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America's 38.36% share in 2025 stems from its advanced manufacturing base, strong venture funding, and early adoption of private-5G pilots. Federal programs that incentivize reshoring and resilience amplify demand for visibility across domestic supply chains. Regulatory frameworks, notably FDA process-monitoring rules, push real-time quality logging in life-sciences plants.

Asia Pacific, growing at 24.98% CAGR, benefits from the world's largest electronics production clusters and government subsidies that lower initial deployment costs. China's tier-one cities spearhead large-scale smart factories, while India's tech centers extend low-cost integration services to neighboring ASEAN exporters. Cross-border component trade encourages interoperable solutions, further enlarging the industrial internet of things market.

Europe balances stringent data-privacy laws with sustainability directives. GDPR steers architectures toward local edge processing, and the continent's 2050 carbon-neutral goal mandates granular energy metering. Germany's automotive primes adopt OPC UA over TSN to converge IT-OT backbones, providing reference models replicated across the European Economic Area.

- Amazon Web Services Inc.

- Telefonaktiebolaget LM Ericsson

- Fujitsu Ltd.

- Mitsubishi Electric Corporation

- SAP SE

- Siemens AG

- Honeywell International Inc.

- Emerson Electric Co.

- OMRON Corporation

- International Business Machines Corporation

- Robert Bosch GmbH

- Oracle Corporation

- PTC Inc.

- Telit IoT Platforms Limited

- NXP Semiconductors N.V.

- Cisco Systems Inc.

- Infineon Technologies AG

- Rockwell Automation Inc.

- Advantech Co. Ltd.

- Schneider Electric SE

- ABB Ltd.

- Hitachi Ltd.

- General Electric Company

- Intel Corporation

- Arm Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Integration of advanced sensors and falling device costs

- 4.2.2 Push for predictive maintenance and OEE improvement

- 4.2.3 Government-backed smart-manufacturing initiatives

- 4.2.4 Private 5G campus networks in heavy industry

- 4.2.5 ESG-driven energy-intensity benchmarking

- 4.2.6 Chiplet-based industrial edge AI accelerators

- 4.3 Market Restraints

- 4.3.1 OT cybersecurity and legacy system vulnerabilities

- 4.3.2 Lack of cross-vendor interoperability standards

- 4.3.3 Scarcity of brown-field digital-twin talent

- 4.3.4 Rising shadow-IT risk from low-code IoT apps

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Intensity of Competitive Rivalry

- 4.6.5 Threat of Substitutes

- 4.7 Investment and Funding Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.1.1 Sensors and Actuators

- 5.1.1.2 Edge Gateways and IPCs

- 5.1.1.3 Industrial Robots and Controllers

- 5.1.2 Software

- 5.1.2.1 Device Management Platforms

- 5.1.2.2 Analytics and Visualization

- 5.1.2.3 MES/SCADA and Digital-Twin Software

- 5.1.3 Services and Connectivity

- 5.1.3.1 Professional and Integration

- 5.1.3.2 Managed Services

- 5.1.3.3 Connectivity Services (MNOs, LPWAN, Satellite)

- 5.1.1 Hardware

- 5.2 By Deployment Model

- 5.2.1 On-premises

- 5.2.2 Cloud

- 5.2.3 Hybrid/Edge-Cloud

- 5.3 By Connectivity Technology

- 5.3.1 Wired (Ethernet, PROFINET, Modbus-TCP)

- 5.3.2 Short-Range Wireless (BLE, Wi-Fi 6/6E)

- 5.3.3 Cellular (4G LTE-M, Private 5G)

- 5.3.4 LPWAN (LoRa WAN, Sigfox, NB-IoT)

- 5.4 By End-user Vertical

- 5.4.1 Discrete Manufacturing

- 5.4.2 Process Manufacturing

- 5.4.3 Oil and Gas

- 5.4.4 Utilities (Power, Water)

- 5.4.5 Transportation and Logistics

- 5.4.6 Mining and Metals

- 5.4.7 Healthcare and Pharmaceuticals

- 5.4.8 Other End-user Verticals

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Russia

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 India

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Amazon Web Services Inc.

- 6.4.2 Telefonaktiebolaget LM Ericsson

- 6.4.3 Fujitsu Ltd.

- 6.4.4 Mitsubishi Electric Corporation

- 6.4.5 SAP SE

- 6.4.6 Siemens AG

- 6.4.7 Honeywell International Inc.

- 6.4.8 Emerson Electric Co.

- 6.4.9 OMRON Corporation

- 6.4.10 International Business Machines Corporation

- 6.4.11 Robert Bosch GmbH

- 6.4.12 Oracle Corporation

- 6.4.13 PTC Inc.

- 6.4.14 Telit IoT Platforms Limited

- 6.4.15 NXP Semiconductors N.V.

- 6.4.16 Cisco Systems Inc.

- 6.4.17 Infineon Technologies AG

- 6.4.18 Rockwell Automation Inc.

- 6.4.19 Advantech Co. Ltd.

- 6.4.20 Schneider Electric SE

- 6.4.21 ABB Ltd.

- 6.4.22 Hitachi Ltd.

- 6.4.23 General Electric Company

- 6.4.24 Intel Corporation

- 6.4.25 Arm Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment