PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1639437

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1639437

Industrial Robotics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

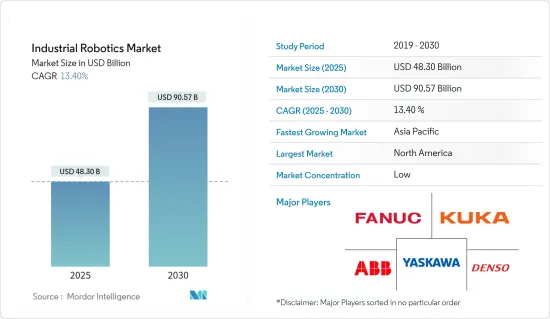

The Industrial Robotics Market size is estimated at USD 48.30 billion in 2025, and is expected to reach USD 90.57 billion by 2030, at a CAGR of 13.4% during the forecast period (2025-2030).

Key Highlights

- Industrial robots play a crucial role in manufacturing industrial automation, with many core operations in industries being managed by robots. With economic growth across regions, e-commerce, electronics, and the automotive industry, among others, have increased.

- Rising penetration of the IoT and investments in robotics across regions have been major contributors to the market's growth. For instance, the 'Made in China 2025' announcement aimed to broadly upgrade the Chinese industry by moving toward quality-focused and innovation-driven manufacturing.

- Industry 4.0, the newest industrial revolution, has fueled the development of new technologies, like collaborative robots, AI-enabled robots, etc., and has enabled industries to use robots to streamline many processes, increase efficiency, and eliminate errors. Increased workplace safety and improved production capabilities have further driven industries to invest in robotic systems.

- Owing to collaborative robots, which are estimated to account for 34% of the total robot sales in 2025 (according to the International Federation of Robots (IFR), the penetration of industrial robots is expected to rise across industries, such as plastics, food and consumer goods, semiconductors and electronics, life sciences, and pharmaceuticals. Another notable factory automation is expected at Apple's factories through Foxconn's robots. Semiconductor industry IC foundries have been among the adopters that have impacted the current market demands.

- Some of the major factors driving the market include rising demand for high-quality products (which need proper end-to-end visibility in the manufacturing process), the need for energy conservation, and rising focus on workplace safety. Incremental advancements in technology, coupled with a sustained increase in the development of manufacturing facilities, are also expected to drive this market, for instance, According to the Association for Advancing Automation (A3), which monitors industrial robot sales in North America. Companies ordered 44,196 robots in 2022, 11% more than in 2021.

Industrial Robotics Market Trends

Automotive Industry to Hold Major Share

- For the past 50 years, the automotive industry has used robots in its assembly lines for various manufacturing processes. Currently, automakers are exploring the use of robotics in more procedures. Robots are more efficient, flexible, accurate, and dependable for such production lines. This technology enables the automotive industry to remain one of the most significant robot users and possess one of the most automated supply chains globally.

- Furthermore, the growing adoption of automation in the automotive manufacturing process and the involvement of AI and digitalization are the primary factors increasing the demand for industrial robots in the automotive sector.

- In today's automotive industry, the advancement of robotics technology has accelerated to keep up with the rapid changes in the automotive industry. A robotics solution simulation and virtual commissioning will utilize the maximum benefits of factory automation for OEMs, startups, and suppliers in the present automotive industry.

- For instance, For instance, Europe's second-largest car manufacturer, PSA Group, modernizes its European manufacturing sites with Universal Robots' UR10 collaborative robots. According to UBS, around 6.3 billion electric vehicles are forecast to be sold in Europe in 2025.

- To cater to the changing landscape of automotive manufacturing, many players in the industry are adopting industrial robots. For instance, in January 2022, Huayu Automotive Systems Co., which does business as HASCO, and ABB Group announced that they have created a joint venture building on their existing relationship "to drive the next generation of smart manufacturing." The companies claimed that the joint venture would enable them to further develop HASCO's leading position with automated solutions that benefit customers in China.

- Further, the growing automotive sector worldwide supports the growth of industrial robotics for welding car parts, palletizing, part insertion, pick-and-pale applications, and many other uses. Moreover, in July 2022, Yamaha Motor Robotics announced to showcase of its latest robots for Advanced Automation at Motek 2022. The company will demonstrate SCARA, cartesian and single-axis robots, and the LCMR200 linear conveyor module, highlighting their speed, accuracy, and flexibility.

North America to Hold a Significant Market Share

- The government in the region is also encouraging the adoption of robotics by taking initiatives to support the development of modern technologies in the robotics market. For instance, the US federal government has commenced the National Robotics Initiative (NRI) program to bolster the capabilities of building domestic robots and encourage research activities in the field.

- In February 2022, United States Steel and Carnegie Foundry, a robotics and AI studio, announced a strategic investment and relationship. The two Pittsburgh-based startups will collaborate to accelerate and expand industrial automation powered by advanced robotics and artificial intelligence. Carnegie Foundry will use this funding to market and scale its industrial automation portfolio of robotics and AI technologies in advanced manufacturing, industrial robots, integrated systems, autonomous mobility, speech analytics, and other areas.

- In March 2022, Kinova Robotics introduced Link 6, Canada's first industrial collaborative robot. Link 6 is Canada's first industrial collaborative robot, with automation solutions that increase daily productivity while enhancing product quality and consistency. The Link 6 robotic arm is developed and constructed with any user in mind, both for experienced industrial integrators and operators with no particular robotic expertise, achieving quick cycle times through longer reach and fast movements. The Link 6 controller from Kinova has the market's most processing power and memory capacity. It supports an optional GPU, making it ready for use with future AI solutions while keeping the controller compact.

- Association for Advancing Automation (A3), companies in North America ordered 9,853 million robots in the second quarter of 2021, which is a significant increase compared to 2020, with 5,196 sales, leading to new job opportunities. Further, according to Robotic Industries Association (RIA), the most critical driver of the year-to-date increase in industrial robots was an 83% growth in units purchased by automotive OEMs for process automation.

Industrial Robotics Industry Overview

The industrial robotics market is highly fragmented. Industry 4.0, with digitalization initiatives across regions, provides lucrative opportunities in the industrial robots market. The degree of transparency is high, considering the number of robotic trade exhibits across conducted areas occasionally. Overall, the competitive rivalry among existing players is high. The acquisitions and collaboration of large companies with startups are predicted, focusing on innovation. A few major players in the market are ABB and Yaskawa. Some of the key developments in the area are:

- May 2024: ABB, an industrial robot manufacturer, unveiled its latest modular large robots at Automate 2024. These robot arms, in conjunction with the previously released IRB 5710-5720 and IRB 6710-6740 models, now present a lineup of 46 variants. These variants are capable of managing payloads ranging from 70 to 620 kilograms (approximately 150 to 1,350 pounds).

- March 2024: Mobile Industrial Robots has unveiled its latest product, the MiR1200 autonomous pallet jack. Equipped with advanced 3D vision technology, the MiR1200 Pallet Jack is designed to streamline labor-intensive materials handling. This robot can adapt its route dynamically, ensuring navigation even in the presence of obstacles, such as loose objects on the floor or overhead hindrances.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHT

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of the Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increased Emphasis on Workplace Safety

- 5.1.2 Emerging Technologies in Industrial Robots

- 5.2 Market Restraints

- 5.2.1 Lack of Skilled Workforce

6 MARKET SEGMENTATION

- 6.1 By Type of Robot

- 6.1.1 Articulated Robots

- 6.1.2 Linear Robots

- 6.1.3 Cylindrical Robots

- 6.1.4 Parallel Robots

- 6.1.5 SCARA Robots

- 6.1.6 Other Types of Robot

- 6.2 By End-user Industry

- 6.2.1 Automotive

- 6.2.2 Chemical and Manufacturing

- 6.2.3 Construction

- 6.2.4 Electrical and Electronics

- 6.2.5 Food and Beverage

- 6.2.6 Machinery and Metal

- 6.2.7 Pharmaceutical

- 6.2.8 Other End-user Industries (Rubber, Optics)

- 6.3 By Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 United Kingdom

- 6.3.2.2 France

- 6.3.2.3 Germany

- 6.3.3 Asia

- 6.3.3.1 Japan

- 6.3.3.2 China

- 6.3.3.3 India

- 6.3.3.4 South Korea

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East and Africa

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 ABB Ltd.

- 7.1.2 Yaskawa Electric Corporation

- 7.1.3 Denso Corporation

- 7.1.4 Fanuc Corporation

- 7.1.5 KUKA AG

- 7.1.6 Kawasaki Robotics

- 7.1.7 Toshiba Corporation

- 7.1.8 Panasonic Corporation

- 7.1.9 Staubli Mechatronics Company

- 7.1.10 Yamaha Robotics

- 7.1.11 Epson Robots

- 7.1.12 Comau SPA

- 7.1.13 Adept Technologies

- 7.1.14 Nachi Robotic Systems Inc.

8 INVESTMENT ANALYSIS

9 FUTURE OUTLOOK OF THE MARKET