PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1639385

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1639385

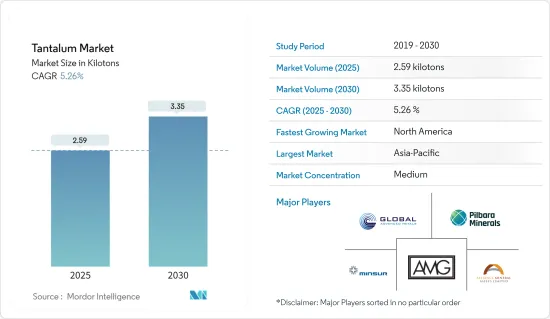

Tantalum - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Tantalum Market size is estimated at 2.59 kilotons in 2025, and is expected to reach 3.35 kilotons by 2030, at a CAGR of 5.26% during the forecast period (2025-2030).

The COVID-19 pandemic hurt the tantalum market globally as end-user industries were significantly affected. However, growth in the electrical segment is improving in the industry, which will assist the market development. The tantalum market has recovered from the pandemic and is growing significantly.

Key Highlights

- Over the short term, the growth of the electrical and electronic industry and the extensive usage of tantalum alloys in aviation and gas turbines are projected to fuel market growth throughout the forecast period.

- Replacing solid capacitors with polymer tantalum capacitors is expected to act as an opportunity for the studied market.

- On the flip side, the harmful effects of tantalum and the decrease in demand from end-user industries are hindering the market's growth.

- Asia-Pacific dominates the market across the world, with the largest consumption from countries such as China and South Korea.

Tantalum Market Trends

Capacitor Segment is Anticipated to Hold a Significant Share

- A tantalum electrolytic capacitor is made of tantalum (Ta) metal as anode material, which can be divided into foil and tantalum powder sintered types according to different anode structures. Among tantalum powder sintered tantalum capacitors, there are tantalum capacitors with solid and non-solid electrolytes due to different electrolytes. The shell of tantalum electrolytic capacitors is marked with CA, but the symbol in the circuit is the same as that of other electrolytic capacitors.

- Tantalum electrolytic capacitors are widely used in communications, computers, aerospace, and military, as well as advanced electronic systems, portable digital products, and other fields.

- Since tantalum electrolytic capacitors are made of very fine tantalum powder, and the dielectric constant of the tantalum oxide film is higher than that of the alumina oxide film, the capacitance per unit volume of tantalum electrolytic capacitors is large.

- Tantalum electrolytic capacitor can work normally at the temperature of -50 ~100 . Although the aluminum electrolytic capacitor can work in this range, its electrical performance is not as good as that of the tantalum electrolytic capacitor.

- Tantalum oxide film in tantalum electrolytic capacitors is not only corrosion-resistant but also maintains good performance for a long time.

- According to the Japan Electronics and Information Technology Industries Association (JEITA), the global computers and information terminal devices export reached JPY 378,097 million (~USD 2,862.95 million) in 2021, with a growth of 106.5%. This is further expected to grow in the coming years, thereby enhancing the demand for the tantalum market.

- Additionally, according to ZVEI, the global consumer electronics market is expected to grow by 5% in 2022. In 2022, the lighting segment should again manage a slightly higher growth of 6% to EUR 138.5 billion (~USD 147.08 billion), while domestic electric appliances (to EUR 287.4 billion (~USD 305.20 billion)) and consumer electronics (to EUR 268.7 billion (~USD 285.34 billion)) might each increase by 5%. This growth is expected to enhance the demand for tantalum-based capacitors from consumer electronics applications.

Asia-Pacific to Dominate the Market

- Asia-Pacific was the major market for the consumption of tantalum, owing to increasing consumption from countries such as China and South Korea. The increase in demand from end-user industries, including electronics, aerospace, and medical equipment, primarily drives the region.

- China is one of the major consumers of tantalum globally. Due to the increasing demand from its industries, the market studied is expected to grow in China in the coming years. China is the largest base for electronics production in the world. Electronic products, such as smartphones, TVs, wires, cables, portable computing devices, gaming systems, and other personal devices, recorded the highest growth in the electronics segment. The country not only serves domestic demand for electronics but also exports electronic output to other countries and is also a leading manufacturer of various components worldwide.

- China is one of the largest aircraft manufacturers and one of the largest markets for domestic air passengers. The civil aircraft fleet in the country has been increasing steadily for the past five years. Moreover, Chinese airline companies plan to purchase about 7,690 new aircraft in the next 20 years, which were valued at approximately USD 1.2 trillion. Boeing estimated that the domestic average RPK (Revenue Passenger Kilometer) growth rate in China is expected to increase at an annual rate of 6.1% in the next 10 years. Therefore, the demand for capacitors and engine turbine blades aerospace application is increasing, which further is expected to boost the demand for the market studied.

- India is expected to have a digital economy of USD 1 trillion by 2025, and the Indian electronics system design and manufacturing (ESDM) sector is expected to generate over USD 100 billion in economic value by 2025. Several policies, such as Make in India, National Policy of Electronics, Net Zero Imports in Electronics, and Zero Defect Zero Effect, offer a commitment to growth in domestic manufacturing, lowering import dependence, and energizing exports and manufacturing.

- The government launched new schemes to promote electronics production in India, the scheme for Promotion of Manufacturing of Electronic Components and Semiconductors (SPECS) and the scheme for modified Electronics Manufacturing Clusters (EMC 2.0), alongside Production Linked Incentive (PLI). According to the PLI scheme, the government is likely to offer incentives as manufacturers increase production in India with USD 5.5 billion available over five years. This is likely to boost the production of electronics in the country.

- South Korea is another important export-based economy in the Asia-Pacific region. South Korea has the third-largest electronics industry in the world in terms of production and fifth-largest in terms of consumption. In 2021, the electronics are valued at USD 200.79 billion.

Tantalum Industry Overview

The tantalum market is partially consolidated in terms of tantalum mining companies. The major companies (not in a particular order) include Global Advanced Metals Pty Ltd, AMG Advanced Metallurgical Group NV, Pilbara Minerals, Alliance Mineral Assets Limited, and Minsur (Mining Taboca).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand from the Electrical and Electronics Industry

- 4.1.2 Extensive Usage of Tantalum Alloys in Aviation and Gas Turbines

- 4.2 Restraints

- 4.2.1 Harmful Effects of Tantalum and Decrease in Demand from End-user Industries

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

- 4.5 Import-Export Trends

- 4.6 Technological Snapshot

- 4.7 Price Index

- 4.8 Regulatory Policy Analysis

5 MARKET SEGMENTATION (Market Size by Volume)

- 5.1 Product

- 5.1.1 Metal

- 5.1.2 Carbide

- 5.1.3 Powder

- 5.1.4 Alloys

- 5.1.5 Other Product Forms

- 5.2 Application

- 5.2.1 Capacitors

- 5.2.2 Semiconductors

- 5.2.3 Engine Turbine Blades

- 5.2.4 Chemical Processing Equipment

- 5.2.5 Medical Equipment

- 5.2.6 Other Applications (includes Ballistics, Cutting Tools, Optical Applications)

- 5.3 Geography

- 5.3.1 Production Analysis

- 5.3.1.1 United States

- 5.3.1.2 Australia

- 5.3.1.3 Brazil

- 5.3.1.4 China

- 5.3.1.5 Congo

- 5.3.1.6 Ethiopia

- 5.3.1.7 Nigeria

- 5.3.1.8 Rwanda

- 5.3.1.9 Other Countries

- 5.3.2 Consumption Analysis

- 5.3.2.1 Asia-Pacific

- 5.3.2.1.1 China

- 5.3.2.1.2 India

- 5.3.2.1.3 Japan

- 5.3.2.1.4 South Korea

- 5.3.2.1.5 Rest of Asia-Pacific

- 5.3.2.2 North America

- 5.3.2.2.1 United States

- 5.3.2.2.2 Canada

- 5.3.2.2.3 Mexico

- 5.3.2.3 Europe

- 5.3.2.3.1 Germany

- 5.3.2.3.2 United Kingdom

- 5.3.2.3.3 Italy

- 5.3.2.3.4 France

- 5.3.2.3.5 Rest of Europe

- 5.3.2.4 South America

- 5.3.2.4.1 Brazil

- 5.3.2.4.2 Argentina

- 5.3.2.4.3 Rest of South America

- 5.3.2.5 Middle-East and Africa

- 5.3.2.5.1 Saudi Arabia

- 5.3.2.5.2 Rest of Middle-East and Africa

- 5.3.1 Production Analysis

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles (Overview, Financials, Products and Services, and Recent Developments)

- 6.4.1 AMG Advanced Metallurgical Group NV

- 6.4.2 Alliance Mineral Assets Limited

- 6.4.3 China Minmetals Corporation

- 6.4.4 CNMC Ningxia Orient Group Co. Ltd

- 6.4.5 Ethiopian Mineral Development Share Company

- 6.4.6 Global Advanced Metals Pty Ltd

- 6.4.7 Jiangxi Tungsten Industry Group Co. Ltd

- 6.4.8 Minsur (Mining Taboca)

- 6.4.9 Pilbara Minerals

- 6.4.10 Piran Resources Limited (Pella Resources Limited)

- 6.4.11 Tantalex Resources Corporation

- 6.4.12 Tantec GmbH

- 6.4.13 Techmet (KEMET GROUP)

- 6.4.14 Taniobis GmbH

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Replacement of Solid Capacitors with Polymer Tantalum Capacitors

- 7.2 Other Opportunities