PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1444446

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1444446

North America Lab-on-a-chip and Microarrays (Biochip) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

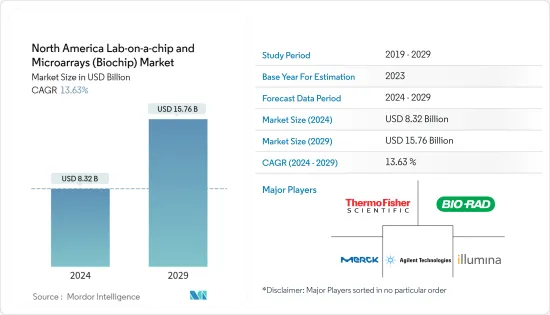

The North America Lab-on-a-chip and Microarrays Market size is estimated at USD 8.32 billion in 2024, and is expected to reach USD 15.76 billion by 2029, growing at a CAGR of 13.63% during the forecast period (2024-2029).

Key Highlights

- The COVID-19 pandemic had a significant impact on the market under study because healthcare services dramatically increased due to their involvement in analyzing various biological samples. Microfluidics provided quick and reasonably priced point-of-care diagnostic instruments for COVID-19 diagnostics, which remained essential in controlling the pandemic and helped with COVID-19 diagnosis. Hence, microfluidics played a pivotal role during the pandemic phase.

- Additionally, as per an article published in December 2021 in the Viruses Journal, a microarray-based technique was created by researchers in Russia to identify immunoglobulin G (IgG) and immunoglobulin M (IgM) antibodies against type I interferons (IFN-Is), betacoronaviruses (SARS-CoV-2, SARS, MERS, OC43, and HKU1), and other respiratory viruses. This multiplex assay was used to monitor antibody cross-reactivity caused by prior exposure to comparable viruses and to pinpoint antibodies against IFN-Is as the indicators for severe COVID-19. Such research during the later phases of the pandemic fueled the adoption of microfluidics and micro-array technology for detection, leading to significant growth in the market.

- In the current times, where everything is normalized to pre-covid levels, diagnostics procedures are regularly operating, increasing the demand for microarrays. This is expected to further drive the market growth over the forecast period.

- Factors such as an increasing application of proteomics and genomics in cancer research, technological advances in microfluidics materials, and the growth of personalized medicine are anticipated to fuel the market growth over the analysis period.

- The incidence of chronic diseases is increasing the healthcare burden in countries across North America, including Canada and Mexico. For instance, as per the statistics provided by the Heart and Stroke Foundation of Canada (HSFC) in February 2022, around 750,000 people were living with heart failure in 2021, and nearly 100,000 people are diagnosed with this incurable condition each year in Canada. Thus, this statistics shows that there is a burden of CVD and associated diseases in the country, and this is further expected to increase the need for the availability of advanced CVD detection tools.

- The need for microfluidics to identify cardiovascular illnesses is rising due to the effectiveness of microfluidics devices in multiplexing the capture of several cardiac biomarkers at clinically significant concentrations. Thus, the increasing burden of chronic diseases is fueling the growth of the lab-on-chip market, as it can offer a high-throughput screening of these diseases.

- However, factors such as low commercial acceptability due to the high costs and lack of skilled labor are predicted to hinder market growth.

North America Lab-on-a-chip & Microarrays Market Trends

Microarray are Anticipated to Hold Significant Share in the Studied Market

- A microarray is a miniaturized two-dimensional array on a solid substrate used to assay biological materials with multiplexed, parallel processing, and high-throughput screening methods. Additionally, the molecular basis of relationships can be studied using microarrays on a scale that is not conceivable with traditional research. This method allows for the simultaneous analysis of the expression of thousands of genes. Thus, with the advantages of microarrays in studying gene expressions and increasing advancements in product development, the segment is predicted to witness growth.

- Market players are taking several measures, such as product development, partnerships, and many others, to increase their presence in the market, which is expected to aid market growth. For instance, in March 2022, Quotient Limited received Conformite Europeenne (CE) Mark for its MosaiQ Extended Immunohematology (IH) Microarray. The CE marking confirms that the Extended IH Microarray meets the European Medical Devices Directive (EMDD) requirements. Such developments are expected to impact the segment's growth positively.

- Owing to the rising demand for point-of-care diagnostics and increasing accessibility of microarray techniques, market players are developing novel products. For instance, in December 2021, Bionano Genomics, Inc., launched version 6.1 of BioDiscovery's NxClinical software with expanded capabilities for next-generation sequencing (NGS) data in genetic diseases and cancer. These developments are anticipated to fuel segment growth.

- Therefore, the abovementioned factors are expected to accelerate the segment's growth during the forecast period.

United States is Expected to Hold a Significant Share in the Market Over the Forecast Period.

- The United States holds a significant market share in the North American lab-on-a-chip and microarrays (biochip) market and is expected to maintain its stronghold during the forecast period. One of the key factors propelling the biochips market growth is the availability of complete drug development platforms. The demand for biochip and bio-array techniques is rising in North America due to the need to shorten turnaround times and miniaturize biological and clinical tests used for research and diagnosis. Rapid technological advancements associated with these techniques and a broad product line-up also accelerate the growth of the biochips market.

- As per the 2022 statistics published by the National Brain Tumor Society (NBTS), approximately 88,970 people are expected to be diagnosed with a primary brain tumor in the United States in 2022. In addition, as per the same source, an estimated 4,170 new cases of childhood brain tumors and 12,072 new cases of adolescent and young adults brain tumors are expected to be diagnosed in 2022 in the United States. This is expected to increase the need for an advanced tumor detection tool. As microfluidics exhibits high sensitivity and accuracy for detecting cancer-specific biomarkers at low concentrations, the demand for microfluidics is increasing for brain tumor detection. Thus, the increasing burden of chronic diseases is fueling the growth of the lab-on-chip market in the United States.

- Strategic activities such as mergers, acquisitions, and partnerships, along with product launches and approvals by the market players in the country, are expected to accelerate market growth. For instance, in April 2021, PathogenDx, Inc. received the Food and Drug Administration (FDA) emergency use authorization (EUA) approval for DetectX-Rv, an RT-PCR and DNA microarray hybridization test. It is intended for the use of qualitative detection of nucleic acids from the SARS-CoV-2 virus. Such developments are driving market growth in the United States.

- Therefore, the above-mentioned factors are expected to promote market growth in the country during the forecast period.

North America Lab-on-a-chip & Microarrays Industry Overview

The North America lab-on-a-chip and microarrays (Biochip) market is competitive and consists of significant global and regional players. In terms of market share, few major players currently dominate the market. Some companies currently dominating the market are Abbott Laboratories Bio-Rad Laboratories, GE Healthcare, and F. Hoffmann-LA Roche Ltd., among others, which hold a substantial market share in the lab-on-a-chip and microarrays (Biochip) market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Application of Proteomics And Genomics in Cancer Research

- 4.2.2 Technological Advances in the Materials in Microfluidics

- 4.2.3 Growth of Personalized Medicine

- 4.3 Market Restraints

- 4.3.1 Lack of Standardization

- 4.3.2 Availability of Alternative Technologies

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Type

- 5.1.1 Lab-on-a-chip

- 5.1.2 Microarray

- 5.2 By Product

- 5.2.1 Instruments

- 5.2.2 Reagents and Consumables

- 5.2.3 Software and Services

- 5.3 By Application

- 5.3.1 Clinical Diagnostics

- 5.3.2 Drug Discovery

- 5.3.3 Genomics and Proteomics

- 5.3.4 Other Applications

- 5.4 By End User

- 5.4.1 Biotechnology and Pharmaceutical Companies

- 5.4.2 Hospitals and Diagnostics Centers

- 5.4.3 Academic and Research Institutes

- 5.5 Geography

- 5.5.1 United States

- 5.5.2 Canada

- 5.5.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Abbott Laboratories

- 6.1.2 Agilent Technologies Inc.

- 6.1.3 Danaher Corporation (Beckman Coulter Inc.)

- 6.1.4 Biomerieux SA

- 6.1.5 Bio-Rad Laboratories

- 6.1.6 Illumina, Inc.

- 6.1.7 PerkinElmer Inc.

- 6.1.8 F. Hoffmann-LA Roche Ltd

- 6.1.9 Thermo Fisher Scientific

- 6.1.10 Sysmex Corporation

- 6.1.11 Fluidigm Corporation

7 MARKET OPPORTUNITIES AND FUTURE TRENDS