PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1685730

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1685730

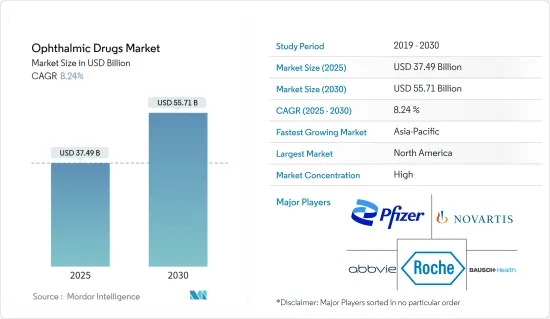

Ophthalmic Drugs - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Ophthalmic Drugs Market size is estimated at USD 37.49 billion in 2025, and is expected to reach USD 55.71 billion by 2030, at a CAGR of 8.24% during the forecast period (2025-2030).

It is witnessing significant growth, underpinned by various factors driving both innovation and expansion in the industry. Key drivers include the increasing prevalence of eye-related disorders and advancements in drug development technologies, which are reshaping the market landscape.

Megatrends Shaping the Industry: The global rise in ocular conditions, an aging population, and advancements in drug formulation technologies are creating robust foundations for market growth. These factors, along with specific industry drivers, are pushing the ophthalmic drugs industry to new heights.

Increasing Incidence and Prevalence of Eye-related Disorders: The growing number of individuals with vision impairment is a major factor driving the market growth. Data from the National Eye Institute projects that by 2030, age-related macular degeneration will impact 3.7 million individuals in the United States. Additionally, the same source estimates that glaucoma will affect 4.3 million Americans by 2030. The high burden of these eye diseases underscores the urgent need for new and effective ophthalmic treatments, driving the market forward.

Rising Research and Development Pertaining to the Development of Novel Drugs: Global ophthalmic drugs market research says that the industry is benefiting from increased R&D activity aimed at creating novel therapeutic solutions. The rise in clinical trials and drug approvals highlights this trend. In 2023, the FDA accepted a New Drug Application for CyclASol, a novel anti-inflammatory product for dry eye disease. Similarly, the European launch of a ranibizumab biosimilar by Xbrane Biopharma AB and STADA Arzneimittel AG showcases the surge in cost-effective treatment options. These innovative drugs are expanding the therapeutic landscape and boosting the market at a decent growth rate.

Increasing Focus on Developing Combination Therapies: The emphasis on combination therapies within the ophthalmic drugs market is growing. These treatments offer superior therapeutic results for managing complex ocular diseases. For instance, in July 2023, Tenpoint Therapeutics secured funding to spearhead its launch aimed at combating degenerative eye diseases. The company specializes in combining various cell-based therapeutics and crafting treatments tailored to individual cases. Their approach centers on rejuvenating eye cells compromised by age-related or inherited ailments. Such partnerships are fueling innovation in the field, accelerating market expansion by addressing unmet medical needs.

Global industry is on a steady growth trajectory, driven by these market trends and developments. Future advancements in drug innovation, personalized treatments, and increased access to eye care will continue to shape the industry. As public awareness around eye health rises and early intervention becomes more critical, the market is poised for sustained growth.

Ophthalmic Drugs Market Trends

Prescription Drugs: Driving Force in Ophthalmic Treatments

Segment Overview: Prescription drugs play a pivotal role in ophthalmic treatments, addressing a wide range of conditions including glaucoma, dry eye, and retinal disorders. These drugs require medical oversight due to their potency and precision. Prescription ophthalmic medications account for approximately 65% of the market share, illustrating their dominant role in eye care management.

Growth Drivers: The rising prevalence of chronic eye disorders, such as age-related macular degeneration and glaucoma, is boosting demand for prescription ophthalmic drugs. Advances in sustained-release technologies and combination therapies are further enhancing patient compliance and treatment outcomes. The global aging population is particularly susceptible to these disorders, which, along with increasing industry research and development efforts, are expected to bolster the growth of this segment.

Competitive Landscape: Leading companies in the prescription drug market are focusing on innovation to gain a competitive edge. The development of advanced drug delivery systems, such as intravitreal implants, is providing new solutions for complex eye conditions. Strategic collaborations and acquisitions are expanding product portfolios, while the rise of personalized medicine is driving the development of targeted therapies. However, potential disruptions, including gene therapies and regenerative medicine, may reshape the market.

North America: Leading the Charge in Ophthalmic Innovation

Regional Dynamics: North America continues to lead the global ophthalmic drugs market size, exhibiting robust growth and innovation. With a highly developed healthcare infrastructure and strong market presence, North America is expected to expand at a compound annual growth rate (CAGR) of over 8% from 2024 to 2029. This growth is fueled by technological advancements, increasing healthcare investments, and rising awareness around eye health.

Market Catalysts: Several factors are driving North America's dominance in ophthalmic drugs. The region's aging population and the prevalence of lifestyle-related ocular disorders contribute to a significant patient base. Favorable reimbursement policies and a supportive regulatory environment also encourage drug innovation and patient access to treatments. With strong funding for industry research and a focus on precision medicine, North America is expected to maintain its leadership in ophthalmic drug development.

Strategic Imperatives: To maintain their market position, companies are investing in research areas like gene therapy and regenerative medicine. Collaborations with biotech firms and academic institutions are essential for accelerating innovation. Additionally, digital health solutions, including telemedicine and artific ial intelligence (AI), are increasingly integrated into eye care. Companies should also prepare for potential shifts in the competitive landscape, driven by tech entrants and value-based care models.

Ophthalmic Drugs Industry Overview

Market Dynamics: Global Players Dominate Consolidated Landscape

This global industry is largely controlled by major multinational pharmaceutical firms with broad product portfolios. Leading companies such as Novartis, Roche, and Regeneron hold substantial ophthalmic drugs market share due to their expansive R&D capabilities and strong distribution networks. The market is consolidated, with a few market leaders and key players dominating a large portion of the total revenue. High entry barriers, complex regulatory frameworks, and the need for significant investment in R&D make it challenging for new entrants to compete with established players.

Market Leaders: Innovation and Pipeline Strength Drive Success

Leading companies like Novartis, Roche, and Regeneron Pharmaceuticals Inc. have made significant strides in retinal disease treatments and other areas of ophthalmology. Novartis' innovations in retinal therapies and Regeneron's success with EYLEA in treating age-related macular degeneration exemplify this. These market leaders are also bolstered by their strong product pipelines, with several late-stage clinical candidates set to launch in the coming years. Their vast global presence and deep relationships with healthcare stakeholders solidify their competitive advantage.

Strategies for Future Success: Focus on Unmet Needs and Emerging Technologies

To capture future market growth, companies must focus on unmet needs in ophthalmology, particularly in treating conditions like dry eye disease and diabetic retinopathy. Leveraging emerging technologies such as gene therapies and sustained-release drug delivery systems could provide a competitive edge. Companies developing long-acting intraocular implants for glaucoma, for instance, could capture significant market share from traditional treatments. Expansion into high-growth regions such as the Asia-Pacific will be critical, alongside partnerships with biotechnology firms and research institutions to foster innovation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Incidence and Prevalence of Eye-related Disorders

- 4.2.2 Rising Research and Development Pertaining to the Development of Novel Drugs

- 4.2.3 Increasing Focus on Developing Combination Therapies

- 4.3 Market Restraints

- 4.3.1 Loss of Patent Protection for Popular Drugs

- 4.3.2 Lack of Health Insurance in the Developing Countries

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value- USD)

- 5.1 By Drug Class

- 5.1.1 Anti-glaucoma Drugs

- 5.1.2 Dry Eye Drugs

- 5.1.3 Ophthalmic Anti-allergy/Inflammatory

- 5.1.4 Retinal Drugs

- 5.1.5 Anti-infective Drugs

- 5.1.6 Other Drugs

- 5.2 By Product Type

- 5.2.1 OTC Drugs

- 5.2.2 Prescription Drugs

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Aerie Pharmaceuticals Inc.

- 6.1.2 AbbVie (Allergan)

- 6.1.3 Bausch Health Companies Inc.

- 6.1.4 Bayer AG

- 6.1.5 F. Hoffmann-La Roche Ltd

- 6.1.6 Novartis AG

- 6.1.7 Viatris Inc.

- 6.1.8 Regeneron Pharmaceuticals Inc.

- 6.1.9 Santen Pharmaceutical Co. Ltd

- 6.1.10 Alcon

- 6.1.11 Sun Pharmaceutical Industries Ltd.

- 6.1.12 Teva Pharmaceutical Industries Ltd.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS