PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073487

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073487

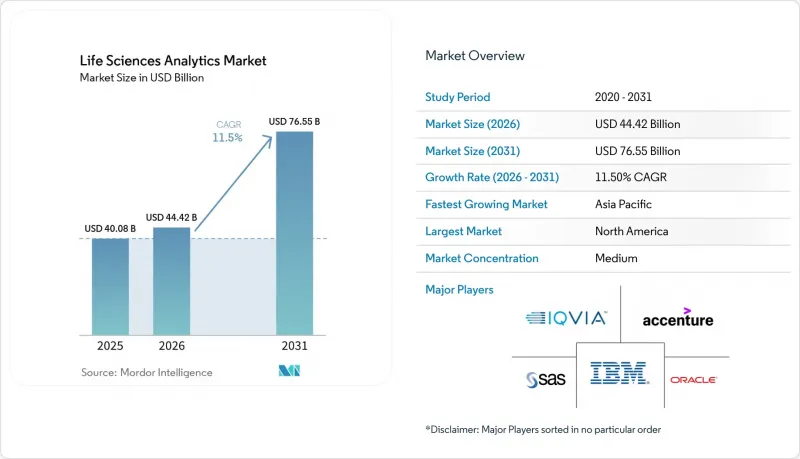

Life Sciences Analytics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the life sciences analytics market size is expected to grow from USD 40.08 billion in 2025 to USD 44.42 billion in 2026 and is forecast to reach USD 76.55 billion by 2031 at 11.5% CAGR over 2026-2031.

This report is Segmented by Product Type (Descriptive, Predictive, and Prescriptive Analytics), Component (Software Platforms and Services), Deployment Mode (On-Premise and Cloud-Based), Application (R&D, Pharmacovigilance, and More), End User (Pharma & Biotech, and More), and Geography (North America, Europe, and More). Market Forecasts are Provided in Terms of Value (USD).

Global Life Sciences Analytics Market Trends and Insights

Exponential Growth of Multimodal Life-Science Data Sets

Sequencing, imaging, and wearable-sensor streams now double every 18 months, outpacing on-premise capacity and prompting sponsors to adopt cloud-native analytics that integrate omics and electronic health record feeds. The National Institutes of Health confirmed its All of Us program amassed 10 petabytes of participant data by mid-2025[1]. Single-cell RNA studies, each producing 1 terabyte, are routine in oncology, yet only a minority of firms maintain pipelines to align these files with imaging archives. The velocity challenge is equally daunting because continuous glucose monitors and implantable devices trigger adaptive-dose algorithms that react within minutes. Companies that master multimodal fusion reduce biomarker discovery timelines from years to quarters, whereas laggards face regulatory queries for missing evidence diversity.

Strict Regulatory Push for Evidence-Based Drug Lifecycle Management

The FDA requires ongoing benefit-risk analytics instead of sporadic safety reviews, compelling perpetual ingestion of claims data, EHRs, and patient-reported outcomes. EMA's adaptive-pathways guidance similarly mandates quarterly effectiveness reports[2]. Large sponsors build in-house observatories, while mid-size firms lean on vendors that compress Sentinel-style surveillance from months to days. Estimand rules in ICH E9(R1) also require statisticians to pre-define analytic scenarios, thereby heightening the demand for prescriptive platforms that automate sensitivity analyses.

Persistent Data Silos and Lack of Interoperability Standards

Fewer than 25% of U.S. hospitals achieved full HL7 FHIR interoperability by the end of 2024 despite the Centers for Medicare & Medicaid Services mandates. Fragmented lab codes and custom connectors stretch project timelines fourfold and inflate the total cost of ownership. Academic centers holding rich longitudinal data often resist sharing due to competitive concerns, reinforcing the advantage for firms with existing collaborations.

Other drivers and restraints analyzed in the detailed report include:

- Escalating R&D Cost Pressures Encouraging Analytics-Led Efficiency

- Shift Toward Precision Medicine and Biomarker-Driven Trials

- Heightened Global Data Privacy Regulations Inflating Compliance Burden

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Descriptive analytics held 45.23% of the Life science analytics market in 2025. Prescriptive Analytics, supported by the FDA's endorsement of model-informed development, is growing at a 13.56% CAGR and is poised to transform trial-design processes. Predictive Analytics bridges the two by delivering risk scores that inform enrollment and dosing. Vendors respond by integrating all three capabilities in unified suites, easing workflow continuity for statisticians.

Prescriptive adoption still faces a scarcity of clinical data scientists, prompting vendors to release low-code interfaces. Predictive growth relies on expanding real-world data, while Descriptive tools plateau as dashboard infrastructure matures. IQVIA's 2024 Orchestrated Analytics illustrates platform convergence, enabling users to transition from summary visualizations to in-silico dose optimization within a single session.

Services controlled 55.32% of spending in 2025 due to the complexity of legacy integration. Software Platforms are advancing at a 13.87% CAGR as vendors pre-train algorithms and embed industry-specific templates, reducing deployment time from half a year to six weeks. Large firms select platforms for flexibility, whereas mid-size sponsors keep services for outsourced expertise in protocol design and regulatory interpretation.

Global consultancies acquire specialist boutiques to deliver strategy-through-operations offerings. Meanwhile, cloud providers roll out natural-language interfaces, broadening user access beyond statisticians. ISO 13485 quality standards prompt platform vendors to invest in change-control rigor, thereby raising barriers to entry for smaller code shops.

Complete Report Scope:

- By Product Type

- Descriptive Analytics

- Predictive Analytics

- Prescriptive Analytics

- By Component

- Software Platforms

- Services

- By Deployment Mode

- On-Premise

- Cloud-Based

- By Application

- Research & Development

- Pharmacovigilance & Safety

- Supply-Chain & Manufacturing QA/QC

- Sales, Marketing & Market Access

- Commercial Real-World Evidence / HEOR

- By End User

- Pharmaceutical & Biotechnology Companies

- Medical Device Companies

- Other End Users

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle-East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America commanded 41.36% of the Life science analytics market in 2025, powered by the FDA's progressive trial-design guidance and NIH's 10-petabyte All of Us dataset that fuels algorithm training. The region offers mature EHR penetration and abundant high-performance computing, giving domestic sponsors a head start in deploying multimodal analytics. Federal cloud-security authorizations also accelerate the migration of regulated workloads.

Asia-Pacific records the fastest 12.64% CAGR, reflecting synchronized regulatory moves. China's National Medical Products Administration aligned its real-world evidence rules with ICH E9(R1) in 2024, allowing sponsors to pool Asian cohorts with Western studies. India's Digital Health Mission aims for universal EHR coverage by 2027, while Japan's PMDA introduced submission templates for post-market data, spurring analytics adoption across oncology, metabolic, and rare-disease programs.

Europe posts steady but slower growth due to stricter data-transfer rules. The 2024 EU Health Data Space introduces additional approval steps on top of GDPR, increasing compliance efforts for cloud-based analytics. Nevertheless, strong academic research networks, deep AI talent pools, and access to Horizon Europe funding sustain ongoing investments in the platform. The Middle East and Africa remain nascent; South Africa's 2024 national repository signals early momentum, but high-performance computing deficits limit omics workloads.

- Accenture

- Clarivate

- Cognizant

- Dassault Systemes

- Exl Service

- IBM

- IQVIA

- MaxisIT

- Microsoft

- Optum Life Sciences

- Oracle

- SAP

- SAS Institute

- TAKE Solutions Ltd.

- Veeva Systems

- Wipro

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Exponential Growth of Multimodal Life-Science Data Sets

- 4.2.2 Strict Regulatory Push for Evidence-Based Drug Lifecycle Management

- 4.2.3 Escalating R&D Cost Pressures Encouraging Analytics-Led Efficiency

- 4.2.4 Shift Toward Precision Medicine and Biomarker-Driven Trials

- 4.2.5 Rapid Adoption of Federated Learning to Enable Cross-Border Data Collaboration

- 4.2.6 Emergence of Real-Time Digital Twins for Adaptive Clinical Operations

- 4.3 Market Restraints

- 4.3.1 Persistent Data Silos and Lack of Interoperability Standards

- 4.3.2 Heightened Global Data Privacy Regulations Inflating Compliance Burden

- 4.3.3 Limited Validation Frameworks for AI Models In Regulated Environments

- 4.3.4 Rising Cloud-Compute Costs Hindering Large-Scale Omics Analytics

- 4.4 Regulatory Outlook

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Descriptive Analytics

- 5.1.2 Predictive Analytics

- 5.1.3 Prescriptive Analytics

- 5.2 By Component

- 5.2.1 Software Platforms

- 5.2.2 Services

- 5.3 By Deployment Mode

- 5.3.1 On-Premise

- 5.3.2 Cloud-Based

- 5.4 By Application

- 5.4.1 Research & Development

- 5.4.2 Pharmacovigilance & Safety

- 5.4.3 Supply-Chain & Manufacturing QA/QC

- 5.4.4 Sales, Marketing & Market Access

- 5.4.5 Commercial Real-World Evidence / HEOR

- 5.5 By End User

- 5.5.1 Pharmaceutical & Biotechnology Companies

- 5.5.2 Medical Device Companies

- 5.5.3 Other End Users

- 5.6 Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle-East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials As Available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Accenture PLC

- 6.3.2 Clarivate

- 6.3.3 Cognizant Technology Solutions

- 6.3.4 Dassault Systmes

- 6.3.5 ExlService Holdings, Inc.

- 6.3.6 IBM Corporation

- 6.3.7 IQVIA

- 6.3.8 MaxisIT Inc.

- 6.3.9 Microsoft Corporation

- 6.3.10 Optum Life Sciences

- 6.3.11 Oracle Corporation

- 6.3.12 SAP SE

- 6.3.13 SAS Institute Inc.

- 6.3.14 TAKE Solutions Ltd.

- 6.3.15 Veeva Systems Inc.

- 6.3.16 Wipro Limited

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment