PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1438277

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1438277

Edible Films and Coating - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

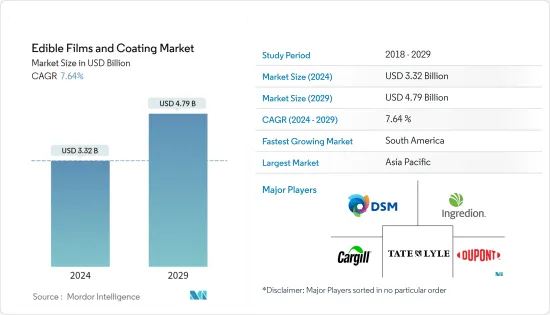

The Edible Films and Coating Market size is estimated at USD 3.32 billion in 2024, and is expected to reach USD 4.79 billion by 2029, growing at a CAGR of 7.64% during the forecast period (2024-2029).

Key Highlights

- The benefit of using edible coating on food products is that it acts as a barrier for carbon dioxide, lipids, moisture, oxygen, and aromas. It improves food quality and extends the shelf life of products. One major advantage of using edible films and coatings is that several active ingredients can be incorporated into the polymer matrix and consumed with food, thus, enhancing safety or even nutritional and sensory attributes. The edible coatings can be made from soybean protein, wheat gluten, whey, gelatin, and many more.

- Demand for plant-based food products is increasing among consumers because of their benefits and health consciousness. The food product manufacturers have increased their efforts to increase the shelf life and improve the existing packaging technology, ensuring the microbial safety and preservation of food from the influence of external factors. Technological institutes and researchers are innovating new technologies to develop edible films with the use of different components.

- For instance, in September 2022, the Indian Institute of Technology, Guwahati, developed an edible coating to extend the shelf life of fruits and vegetables. The coating is made from a mix of microalgae extract and polysaccharides. The marine microalgae Dunaliella tertiolecta, known for its antioxidant properties, is used for its various bioactive compounds such as carotenoids, proteins, and polysaccharides. Thus, new product innovations from manufacturers are expected to contribute to the market growth of the edible films and coatings market.

Edible Films & Coatings Market Trends

Increasing Demand for Edible Packaging from Natural Resources

- Traditional food packaging materials have many shortcomings like environmental effects, pollution, manufacturing requirements, and wastage. The need for alternative packaging materials and packaging formats has increased at a significant level.

- Issues about sustainability, ethics, food safety, food quality, and product costs are all becoming increasingly important factors for modern-day consumers at the time of purchasing food products, and food packaging legislative regulations enforce a number of these issues. All these factors have largely contributed to the rising demand for edible films and coatings in the food packaging industry. These edible films are extracted from natural and organic products.

- For instance, wheat gluten, whey protein, corn zein, waxes, cellulose derivatives, and pectins are some edible films manufactured using fruits, nuts, grains, and vegetables. Additionally, manufacturers are innovating in the edible packaging space by using various protein forms.

- For instance, in June 2022, a scientist named Benedetto Marelli launched a biotech startup called Mori to use silk proteins. These proteins are used to coat garden vegetables, tenderized steaks, fresh poultry, and other perishable and packaged foods.

Asia-Pacific Continues to Dominate the Global Market

- China and Japan are the major consumers of the region's edible films and coatings market. In China, xanthan gum is one of the most commonly used edible coatings in food products, giving rise to the high demand for polysaccharide-based films and coatings.

- However, research to discover other sources of edible coatings is being conducted in the region, which is expected to extend the shelf life and prolong the freshness of products. Moreover, the rising awareness in countries like India is projected to lead to a very promising market scenario in the forecast period.

- In April 2021, BASF launched Joncryl HPB (High-Performance Barrier) in Hong Kong. According to the firm, this specific product is a water-based liquid barrier coating that plays an important role in the latest packaging trends and the conservation of natural resources. The strategy behind this new launch was to expand the company's business.

Edible Films & Coatings Industry Overview

The edible films and coating market is fragmented with global and regional market players. The major players operating in the edible films and coatings market include DuPont de Nemours Inc, Tate & Lyle, Cargill, Incorporated, Koninklijke DSM N.V., and Ingredion Incorporated. Edible film and coatings are a growing market within the packaging segment, where the demand is expected to upscale as consumers seek such options from their regular consumables. The market is poised to witness more innovations over the coming years, and the industry may expect mergers and acquisitions. New brands have emerged recently and have gained significant traction based on their offerings.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.2 Market Restraints

- 4.3 Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Ingredient Type

- 5.1.1 Protein

- 5.1.2 Polysaccharides

- 5.1.3 Lipids

- 5.1.4 Composites

- 5.2 Application

- 5.2.1 Dairy products

- 5.2.2 Bakery and Confectionery

- 5.2.3 Fruits and Vegetables

- 5.2.4 Meat, Poultry, and Seafood

- 5.2.5 Other Applications

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 Germany

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 India

- 5.3.3.2 China

- 5.3.3.3 Japan

- 5.3.3.4 Australia

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 South Africa

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Share Analysis

- 6.2 Most Adopted Strategies

- 6.3 Company Profiles

- 6.3.1 Tate & Lyle PLC

- 6.3.2 DuPont de Nemours Inc.

- 6.3.3 DOHler Group Se

- 6.3.4 Koninklijke DSM N.V.

- 6.3.5 Cargill, Incorporated

- 6.3.6 Ingredion Incorporated

- 6.3.7 RPM International, Inc. (Mantrose-Haeuser Co. Inc.)

- 6.3.8 Nagase & Co Ltd

- 6.3.9 Sumitomo Chemical Co. Ltd

- 6.3.10 Sufresca

- 6.3.11 Pace International, LLC

- 6.3.12 AgroFresh Solutions, Inc.

- 6.3.13 Akorn Technology, Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS