PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1910538

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1910538

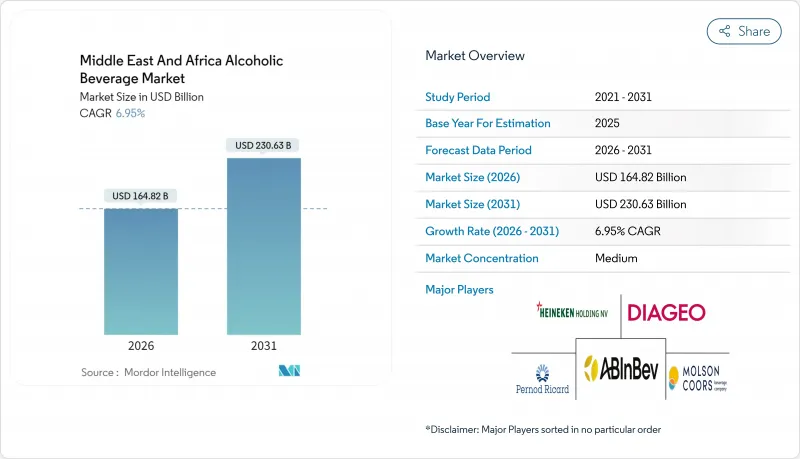

Middle East And Africa Alcoholic Beverage - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

Middle East and Africa alcoholic beverages market size in 2026 is estimated at USD 164.82 billion, growing from 2025 value of USD 154.11 billion with 2031 projections showing USD 230.63 billion, growing at 6.95% CAGR over 2026-2031.

The market advancement is fundamentally driven by substantial macroeconomic progression, notable demographic transformations, and evolving consumer behavioral patterns. The region's progressive urbanization trajectory and escalating disposable income levels are catalyzing consumption dynamics, particularly among the young adult demographic and affluent consumer segments pursuing premium beverage offerings. South Africa, the United Arab Emirates, and Nigeria represent the principal growth territories, supported by sophisticated manufacturing infrastructure, an expanding expatriate demographic composition, and robust tourism sectors. Market evolution is further fortified by systematic product innovations, encompassing specialized flavored formulations and ready-to-consume variants that address contemporary consumer preferences regarding product diversification and accessibility.

Middle East And Africa Alcoholic Beverage Market Trends and Insights

Cultural influence of expatriates

The presence of expatriates significantly influences the Middle East and Africa alcoholic beverages market by shaping consumption patterns and increasing demand across product categories. Coming from regions where alcohol consumption is socially accepted, expatriates introduce new preferences and social drinking practices to urban centers and business hubs in the United Arab Emirates, Saudi Arabia, and parts of Africa. This demographic expansion broadens the consumer base and promotes diverse drinking practices, leading to wider acceptance of various alcoholic beverages. Their refined preferences drive demand for international premium brands, craft beverages, and innovative products that meet global standards. In response, premium whisky and vodka brands have introduced specialized products targeting this consumer segment. For instance, in October 2024, South Africa witnessed the launch of two premium whiskies: the Jameson Triple Triple Chestnut Edition and the Glenfiddich Grand Chateau 31-Year-Old Limited Release. These launches demonstrate product innovation aimed at expatriate consumers seeking exclusive, well-crafted beverages with distinct flavor profiles.

Tourism growth in key hubs

Tourism growth in key destinations across the Middle East and Africa drives the alcoholic beverages market by expanding consumer demand and consumption occasions. Tourist arrivals bring international visitors who seek premium and diverse beverage experiences during their stay. Major destinations such as Dubai, Cape Town, Marrakech, and Istanbul have experienced increasing visitor numbers, driving both on-trade consumption in bars, hotels, and restaurants and market value through demand for premium alcoholic products. The hospitality and entertainment sectors in these locations enhance their beverage offerings to capture tourist spending, contributing to market growth. Dubai demonstrates this impact through its visitor statistics. For instance, according to the Department of Economy and Tourism, Dubai received 11.17 million overnight visitors between January and July 2025, showing a 5% increase compared to the same period in 2024 . This tourism growth attracts diverse consumers with varied preferences, increasing demand for premium wines, spirits, and beers.

Stringent regulatory environment

The regulatory framework across the Middle East and Africa imposes substantial limitations on the alcoholic beverages market expansion. The region's intricate legal structures present considerable operational impediments and market entry barriers for manufacturers and distributors. In Algeria, the prohibition of alcohol consumption in public spaces, coupled with Libya's stringent alcohol regulations, effectively eliminates substantial commercial opportunities. The Nigerian market demonstrates additional complexity through its diverse state-level regulatory requirements governing alcohol production, distribution, and retail operations. This regulatory fragmentation necessitates the implementation of jurisdiction-specific compliance and distribution protocols, resulting in elevated operational expenditures and logistical challenges. These regulatory constraints subsequently restrict product accessibility and market penetration while impeding new market participants and product innovation, thereby limiting comprehensive market development.

Other drivers and restraints analyzed in the detailed report include:

- Convenient ready-to-drink offerings

- Product innovation and flavor variety

- Supply chain and distribution challenges

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The beer segment holds a dominant position in the Middle East and Africa alcoholic beverages market, commanding a 53.62% share in 2025, making it the largest product category in the region. This dominance stems from evolving consumer preferences, a large young population base, and increasing urbanization that drives social consumption. Beer's moderate alcohol content compared to spirits appeals to a broad consumer base, including younger adults and those preferring lighter alcoholic options. The growth of craft beer culture and premium offerings has driven market growth, as consumers seek unique flavors and artisanal brews. Cultural acceptance, competitive pricing, and established domestic brewing industries support the segment's growth.

The wine segment in the Middle East and Africa alcoholic beverages market is expected to grow at a CAGR of 9.12% through 2031. This growth is attributed to increasing consumer sophistication, rising demand for premium and sparkling wines, and growing wine appreciation across the region's markets. Affluent consumers view wine as a status symbol, driving demand in this segment. The segment benefits from lifestyle trends favoring moderate alcohol consumption and wine-food pairing, particularly in urban areas with developing dining and hospitality sectors. Market expansion is supported by diverse wine varieties, international brands, and emerging local viniculture. For example, in May 2025, Penfolds and La Chapelle launched a collectors' wine in the United Arab Emirates.

The male dominance at 70.25% share in the Middle East and Africa alcoholic beverages market in 2025 reflects deep-rooted cultural, social, and behavioral patterns. Traditional societal norms in the region permit male alcohol consumption while imposing restrictions and social stigmas on female consumption. Men frequently participate in social gatherings, celebrations, and business events where alcohol consumption is common, contributing to higher consumption rates. The beverage industry's marketing strategies primarily target male consumers through associations with sports, nightlife, and leisure activities. The higher male labor force participation rate in the region, such as South Africa's 64.5% in 2024, according to the World Bank, provides men with greater discretionary income and financial independence to purchase alcoholic beverages .

The female consumer segment in the Middle East and Africa alcoholic beverages market is experiencing a robust CAGR of 8.05%. This significant growth is primarily driven by increasing economic empowerment and financial independence among women in the region, enabling them to make autonomous purchasing decisions. Evolving sociocultural dynamics have also encouraged greater female participation in social settings where alcohol consumption is common. Furthermore, global consumption trends have influenced female consumers to explore a broader range of alcoholic beverages, including low-alcohol options, flavored products, and premium wines. The rapid expansion of digital marketing channels, particularly through social media and influencer collaborations, has further accelerated the normalization of alcohol consumption among women, especially in urban areas, highlighting a shift in consumer behavior and preferences.

The Middle East and Africa Alcoholic Beverages Market is Segmented by Product Type (Beer, Wine, Spirits, and Others), End-User (Male and Female), Packaging Type (Bottles, Cans, and Others), Distribution Channel (On-Trade, Off-Trade), and Geography (South Africa, Saudi Arabia, United Arab Emirates, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Liters).

List of Companies Covered in this Report:

- Anheuser-Busch InBev SA/NV

- Heineken Holdings N.V.

- Diageo plc

- Pernod Ricard SA

- Molson Coors Beverage Company

- Edward Snell & Co Pty Ltd

- Suntory Holdings Limited

- Brown-Forman Corporation

- Bacardi Limited

- KWV Wines & Spirits

- Refriango LDA

- Oude Molen Distillery (Pty) Ltd

- DGB (Pty) Ltd.

- Halewood Artisanal Spirits PLC

- Tokara Wine Estate

- Castel Group

- Midtown Factory LLC

- Van Ryn's Distillery

- United Dutch Breweries

- Intercontinental Distillers Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cultural influence of expatriates

- 4.2.2 Tourism growth in key hubs

- 4.2.3 Convenient ready-to-drink (RTD) offerings

- 4.2.4 Product innovation and flavor variety

- 4.2.5 Celebrity and influencer endorsements

- 4.2.6 Rise of sustainable and ethical consumption

- 4.3 Market Restraints

- 4.3.1 Stringent regulatory environment

- 4.3.2 Supply chain and distribution challenges

- 4.3.3 High taxation and import duties

- 4.3.4 Legal age and licensing controls

- 4.4 Consumer Behaviour Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 By Product Type

- 5.1.1 Beer

- 5.1.1.1 Ale Beer

- 5.1.1.2 Lager

- 5.1.1.3 Low-Alcohol Beer

- 5.1.1.4 Other Beer Types

- 5.1.2 Wine

- 5.1.2.1 Fortified Wine

- 5.1.2.2 Stilll Wine

- 5.1.2.3 Sparkling Wine

- 5.1.2.4 Other Wines Types

- 5.1.3 Spirits

- 5.1.3.1 Brandy and Cognac

- 5.1.3.2 Liquer

- 5.1.3.3 Tequilla and Mezcel

- 5.1.3.4 Rum

- 5.1.3.5 Whisky

- 5.1.3.6 Other Spirit Types

- 5.1.4 Others

- 5.1.1 Beer

- 5.2 By End User

- 5.2.1 Male

- 5.2.2 Female

- 5.3 By Packaging Type

- 5.3.1 Bottles

- 5.3.2 Cans

- 5.3.3 Others

- 5.4 By Distribution Channel

- 5.4.1 On-trade

- 5.4.2 Off-trade

- 5.5 By Geography

- 5.5.1 South Africa

- 5.5.2 Saudi Arabia

- 5.5.3 United Arab Emirates

- 5.5.4 Nigeria

- 5.5.5 Egypt

- 5.5.6 Morocco

- 5.5.7 Turkey

- 5.5.8 Rest of Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Anheuser-Busch InBev SA/NV

- 6.4.2 Heineken Holdings N.V.

- 6.4.3 Diageo plc

- 6.4.4 Pernod Ricard SA

- 6.4.5 Molson Coors Beverage Company

- 6.4.6 Edward Snell & Co Pty Ltd

- 6.4.7 Suntory Holdings Limited

- 6.4.8 Brown-Forman Corporation

- 6.4.9 Bacardi Limited

- 6.4.10 KWV Wines & Spirits

- 6.4.11 Refriango LDA

- 6.4.12 Oude Molen Distillery (Pty) Ltd

- 6.4.13 DGB (Pty) Ltd.

- 6.4.14 Halewood Artisanal Spirits PLC

- 6.4.15 Tokara Wine Estate

- 6.4.16 Castel Group

- 6.4.17 Midtown Factory LLC

- 6.4.18 Van Ryn's Distillery

- 6.4.19 United Dutch Breweries

- 6.4.20 Intercontinental Distillers Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK