PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1939616

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1939616

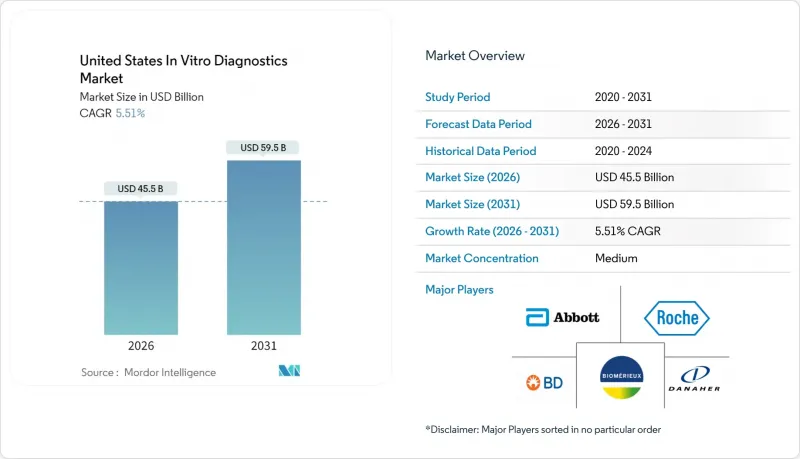

United States In Vitro Diagnostics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

USA in vitro diagnostics market size in 2026 is estimated at USD 45.5 billion, growing from 2025 value of USD 43.13 billion with 2031 projections showing USD 59.5 billion, growing at 5.51% CAGR over 2026-2031.

A balanced mix of demographic aging, wider chronic-disease burden, and permanent adoption of point-of-care (POC) technologies supports this steady climb. Hospitals, clinics, and a fast-growing home-testing channel now embed molecular and immuno-based assays into routine care, while new FDA regulations around laboratory-developed tests (LDTs) shape future competitive entry and compliance spending. Artificial intelligence (AI) models that interpret assay data in real time, cloud-native laboratory information systems, and multiplex panels that shorten turnaround times all help laboratories manage rising test volumes despite workforce shortages. Together, they reinforce the USA in vitro diagnostics market as a critical foundation for precision medicine, infection surveillance, and decentralized care delivery.

United States In Vitro Diagnostics Market Trends and Insights

Rising Prevalence Of Chronic Diseases & Aging Population

Diabetes now affects 15.8% of US adults, while projections indicate that cardiovascular disease could impact 184 million people by 2050. As multiple chronic conditions already touch 76.4% of adults, demand for integrated panels that monitor overlapping metabolic, cardiac, and inflammatory biomarkers continues to rise. The edge that molecular and immuno-assays provide in early detection translates into faster intervention, longer healthy life expectancy, and lower hospital readmission rates. With baby-boomers entering ages of higher disease incidence, laboratories expand capacity for high-throughput chemistry, hemoglobin A1c, and troponin testing, reinforcing the USA in vitro diagnostics market as an essential pillar of preventive medicine.

Rapid Adoption Of Point-Of-Care (POC) Testing

The pandemic underscored how bedside diagnostics can shorten triage times from hours to minutes. FDA's 2024 authorization of home STI panels and combination flu/COVID-19 kits validated distributed testing models. Large urban networks report emergency-department decision time savings of 35-45 minutes when POC troponin, D-dimer, and CRP tests replace central-lab workflows. AI-enabled readers that sync to electronic health records further compress cycle times and support antimicrobial stewardship by matching real-time pathogen identification with guideline-based therapy recommendations. As reimbursement codes catch up, the USA in vitro diagnostics market embeds POC testing into chronic-care pathways for diabetes, heart failure, and kidney disease.

Stringent FDA Regulation of LDTs & Novel Assays

The April 2024 final rule phases out general enforcement discretion, requiring LDT makers to file pre-market submissions, maintain quality systems, and report adverse events. Compliance costs could reach USD 3.56 billion annually, hitting small specialty labs hardest. Stage 1 rules that take effect in May 2025 already force labs to formalize complaint files and device reports. Legal challenges by trade groups inject uncertainty, delaying investment decisions and slowing the roll-out of niche genetic panels that normally refresh market innovation cycles. Over the near term, registration bottlenecks trim the USA in vitro diagnostics market CAGR.

Other drivers and restraints analyzed in the detailed report include:

- Government Preventive-Screening Programs

- Rising Investment in R&D

- High Cost of Advanced Diagnostic Instruments

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Molecular diagnostics delivered 31.62% of USA in vitro diagnostics market share in 2025, underscoring its centrality to COVID-19 surveillance, oncology profiling, and antimicrobial resistance tracking. Immuno-diagnostics follows with an 8.32% forecast CAGR as auto-immune disorders, neuro-degenerative conditions, and companion therapeutic monitoring expand antibody-based testing portfolios. Clinical chemistry anchors basic metabolic panels, while hematology gains from automated coagulation and cell-imaging modules. Microbiology retains relevance through rapid pathogen identification that feeds infection-control decisions.

Continual next-generation sequencing cost compression, droplet digital PCR accuracy gains, and AI-powered variant interpretation keep molecular platforms on a rapid innovation cadence. Breakthroughs such as liquid biopsy panels that detect cell-free DNA fragments at very low allele frequencies reduce reliance on invasive tissue biopsies. This momentum positions the USA in vitro diagnostics market as a global benchmark for precision diagnostics, while immuno-diagnostics leverages multiplexed bead arrays and chemiluminescent assays for expanded biomarker detection, sustaining double-digit growth across autoimmune and neuro-logical applications.

Reagents and kits provided 61.78% of the USA in vitro diagnostics market size in 2025, generating predictable replenishment revenue for manufacturers as test volumes climb. Instruments represent the second-largest contribution, driven by laboratory automation cycles. Software & services, however, register a market-leading 9.41% CAGR because laboratories now tap cloud analytics, remote calibration, and AI-guided quality-control dashboards to address throughput and staffing constraints.

Standalone middleware morphs into integrated laboratory information management systems (LIMS) that orchestrate sample accessioning, track reagent lots, and push results to electronic health records in real time. Vendors bundle subscription-priced decision-support algorithms that flag critical values, compare trends, and suggest reflex testing pathways. This digital layer differentiates suppliers and deepens switching costs, embedding long-term loyalty within the USA in vitro diagnostics market.

The United States in Vitro Diagnostics Market Report is Segmented by Test Type (Clinical Chemistry, Molecular Diagnostics, Hematology, and More), Product (Instruments, Reagents & Kits, and More), Usability (Disposable IVD and Reusable IVD), Application (Infectious Diseases, Diabetes, Oncology, and More), and End User (Diagnostic Laboratories, Hospitals & Clinics, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Abbott Laboratories

- Roche

- Danaher Corp (Beckman Coulter)

- Thermo Fisher Scientific

- Siemens Healthineers

- bioMerieux

- Bio-Rad Laboratories

- QIAGEN

- Beckton Dickinson

- Sysmex Corp.

- Illumina

- Hologic

- Ortho Clinical Diagnostics

- GenMark Diagnostics

- QuidelOrtho

- Exact Sciences Corp.

- DiaSorin (Luminex Corp.)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prevalence Of Chronic Diseases & Aging Population

- 4.2.2 Rapid Adoption Of Point-Of-Care (POC) Testing

- 4.2.3 Government Preventive-Screening Programs

- 4.2.4 Rising Investment in R&D

- 4.2.5 Increasing Adoption of Personalized Medicine

- 4.2.6 Growing Awareness and Health Screenings

- 4.3 Market Restraints

- 4.3.1 Stringent FDA Regulation of LDTs & Novel Assays

- 4.3.2 High Cost of Advanced Diagnostic Instruments

- 4.3.3 Concerns over Data Privacy and Security

- 4.3.4 Limited Skilled Workforce

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Test Type

- 5.1.1 Clinical Chemistry

- 5.1.2 Molecular Diagnostics

- 5.1.3 Immuno-Diagnostics

- 5.1.4 Hematology

- 5.1.5 Microbiology

- 5.1.6 Other Test Types

- 5.2 By Product

- 5.2.1 Instruments

- 5.2.2 Reagents & Kits

- 5.2.3 Software & Services

- 5.3 By Usability

- 5.3.1 Disposable IVD

- 5.3.2 Re-usable IVD

- 5.4 By Application

- 5.4.1 Infectious Diseases

- 5.4.2 Diabetes

- 5.4.3 Oncology

- 5.4.4 Cardiology

- 5.4.5 Autoimmune Disorders

- 5.4.6 Nephrology

- 5.4.7 Other Applications

- 5.5 By End-User

- 5.5.1 Diagnostic Laboratories

- 5.5.2 Hospitals & Clinics

- 5.5.3 Physician Office Labs

- 5.5.4 Home-Care & Self-Testing

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Abbott Laboratories

- 6.3.2 F. Hoffmann-La Roche AG

- 6.3.3 Danaher Corp (Beckman Coulter)

- 6.3.4 Thermo Fisher Scientific Inc.

- 6.3.5 Siemens Healthineers AG

- 6.3.6 bioMerieux SA

- 6.3.7 Bio-Rad Laboratories Inc.

- 6.3.8 Qiagen N.V.

- 6.3.9 Becton, Dickinson & Co.

- 6.3.10 Sysmex Corp.

- 6.3.11 Illumina Inc.

- 6.3.12 Hologic Inc.

- 6.3.13 Ortho Clinical Diagnostics

- 6.3.14 GenMark Diagnostics

- 6.3.15 QuidelOrtho

- 6.3.16 Exact Sciences Corp.

- 6.3.17 DiaSorin (Luminex Corp.)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment