PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1687796

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1687796

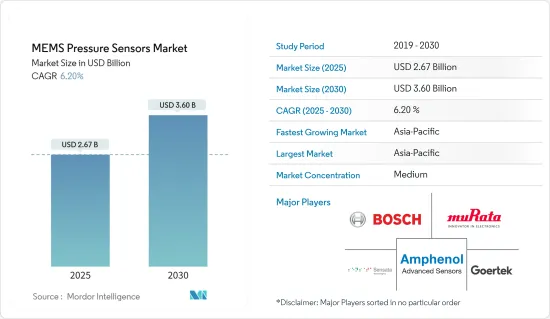

MEMS Pressure Sensors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The MEMS Pressure Sensors Market size is estimated at USD 2.67 billion in 2025, and is expected to reach USD 3.60 billion by 2030, at a CAGR of 6.2% during the forecast period (2025-2030).

Industrial automation and demand for miniaturized consumer devices across regions, such as wearables and IoT-connected devices, are among the significant factors driving the MEMS pressure sensors market.

Key Highlights

- MEMS sensors are gaining popularity across sectors, due to their advantages, such as accuracy and reliability, in addition to the scope for making smaller electronic devices, which have gained significant traction in the past few years. Industrial automation and demand for miniaturized consumer devices across regions, such as wearables and IoT-connected devices, are among the crucial factors driving the MEMS pressure sensors market.

- Also, The automotive industry, which is presently undergoing a technology transition with a significant focus on increasing safety, comfort, and entertainment, provides ample opportunities for MEMS pressure sensors. Emerging sensor-rich applications, such as autonomous vehicles, drones, and AR/VR equipment, further accelerate the need for MEMS pressure sensors.

- In addition, MEMS technologies have enabled miniaturized, cost-effective, and reliable sensors, some of which can withstand high temperatures and harsh environments, expanding the scope of semiconductor devices. Such diversity in MEMS devices and the different technologies involved in their manufacture have led to a complex but sustainable supply chain, from design to testing.

- The interfaces are a source of some of the most severe issues in the design of sensor-based systems. The multiple obstacles connected with sensor interfaces are enough to make design and manufacture complicated. While invaluable for decoupling parts and allowing reuse across different implementations, they are enough to make design and manufacturing difficult. Indeed, more than a third of respondents in a recent Fierce Electronics study on sensor design said that incorporating sensors into a plan is their most demanding issue. This is expected to challenge the market's growth.

- Moreover, the COVID-19 pandemic hurt the MEMS pressure sensors market in 2020 and 2021, which resulted in a slight drop in the MEMS pressure sensors. However, the market studied is likely to grow after the COVID-19 pandemic; the ease of restrictions attracted consumers to make spending decisions on IoT-enabled devices, which mostly come with MEMS pressure sensors.

MEMS Pressure Sensors Market Trends

Emergence of Automation and Industry 4.0 to Drive the Market

- MEMS's key features to support the smart industry are accuracy, reliability, and longevity. For Industry 4.0, MEMS sensors can be applied in early-failure-detection and predictive-maintenance systems where vibration, temperature, pressure, sound, and acoustics analyses are needed, thus, driving its usage in automation and Industry 4.0 applications.

- Massive changes in the manufacturing industry brought by Industry 4.0 and the adoption of IoT demand that businesses adopt flexible and creative strategies to advance production with technologies that complement and augment human labor with automation and lower industrial accidents brought on by process failure. There has been an increase in the number of data points generated in the manufacturing sector as a result of the widespread adoption of connected devices and sensors and the facilitation of M2M communication.

- In addition, the increased adoption of automation across a variety of industries has significantly increased interest in industrial robotics. The International Federation of Robotics (IFR) estimates that industrial robot shipments worldwide reached about 384,000 in 2020, only slightly up from 2019. Industrial robot shipments are anticipated to rise sharply in the years to come, possibly even exceeding the peak year of 2018, when about 422,000 industrial robots were shipped globally. Global shipments of industrial robots are predicted to reach 518,000 units in 2024.

- Industrial robots can be used in a growing number of industries for a variety of tasks. The electrical and electronic industries installed the most industrial robots in 2020, despite the highly automated auto industry continuing to be one of the largest markets for electro-mechanical machines. Such a rise in industrial robots would also boost the demand for MEMS pressure sensors globally.

- Additionally, According to Cisco, by 2022, machine-to-machine (M2M) connections that support IoT applications are expected to account for over half of the world's 28.5 billion connected devices. Manufacturers worldwide also understand that the next generation of robotics and automation technologies is a revolutionary opportunity to upgrade manufacturing in terms of productivity, quality, safety, and cost metrics. Also, increased year-on-year robotic automation expenditure mainly expands the scope of the studied market.

Asia Pacific to Hold Major Market Share

- Asia-Pacific is a well-known manufacturing hub and rapidly growing. There is a need for more safety regulations in the automotive industry. Due to the widespread use of MEMS pressure sensors in smartphones, smart devices, and home electronics, the consumer electronics segment is predicted to dominate the regional MEMS pressure sensor market.

- Additionally, Asia pacific automotive industry is among the largest worldwide, growing from a small government-controlled sector to one controlled by large multinational enterprises over the past few decades. South Korea is home to major players like Kia, Hyundai, and Renault, and it is expected to witness steady growth in the demand for automobiles. Such growth in automobiles will increase demand for MEMS pressure sensors in the region.

- MEMS pressure sensors have a variety of applications in the automotive industry, which is currently undergoing a technological transformation with the primary goal of enhancing safety, comfort, and entertainment. These sensors, like MEMS, are in high demand in the automotive industry due to their small size, which is a key driver of their widespread adoption.

- Since the automotive sector accounts for a sizable portion of the pressure sensor market, the region presents an excellent opportunity over the coming years. The adoption of MEMS pressure sensors is also anticipated to be influenced by the expanding idea of connected cars and Chinese regulations regarding automotive safety.

- In the upcoming years, expanding technological development, IoT adoption on a large scale, pro-product government regulations, and more will all contribute to the growth of the pressure sensors market. However, the market for pressure sensors may face additional challenges due to high regulatory barriers.

MEMS Pressure Sensors Industry Overview

The MEMS pressure sensor market comprises many large-scale vendors capable of both backward and forward integration and commands significant revenue generation capabilities. The market is relatively consolidated, and vendors are increasingly spending on R&D to gain technological capabilities and a competitive edge over other companies. The vendors in the market are competing on technology and quality but not on price. The intensity of competitive rivalry in the market is moderately high and is expected to increase over the coming years.

- July 2022 - Bosch Sensortec announced that Edge Impulse's machine-learning platform supports its sensors on the Arduino NiclaSense ME microcontroller. According to the company's announcement, the first Arduino Pro product was created in association with Bosch Sensortec, in which sensors offered by Bosch Sensortec offer numerous high-accuracy data collection and analysis methods by utilizing the pressure sensor BMP390.

- February 2022 - STMicroelectronics manufacturer of micro-electro-mechanical systems (MEMS), is releasing its third generation of MEMS sensors. The new sensors offer the next jump in performance and features for consumer mobile devices, intelligent industries, healthcare, and retail. Distributors will soon be able to purchase the LPS28DFW pressure sensor in a 2.8mm x 2.8mm x 1.95mm 7-lead LGA and the LPS22DF pressure sensor in a 2.0mm x 2.0mm x 0.73mm 10-lead LGA package.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Technology Snapshot

- 4.5 Assessment of Impact of COVID-19 on the Market

- 4.6 Overview of the Use of Parylene in the MEMS Pressure Sensors

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Emergence of Automation and Industry 4.0

- 5.1.2 Increasing Demand for Sensor-rich Applications

- 5.2 Market Restraints

- 5.2.1 Complexity Regarding Multiple Interface

6 MARKET SEGMENTATION

- 6.1 By Application

- 6.1.1 Medical

- 6.1.2 Automotive

- 6.1.3 Industrial

- 6.1.4 Aerospace and Defense

- 6.1.5 Consumer Electronics

- 6.2 By Type

- 6.2.1 Silicon Piezoresistive

- 6.2.2 Silicon Capacitive

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia Pacific

- 6.3.4 Latin America

- 6.3.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Bosch Sensortec GmbH

- 7.1.2 Murata Manufacturing Co. Ltd

- 7.1.3 Amphenol Advanced Sensors (Amphenol Corporation)

- 7.1.4 Sensata Technologies Inc.

- 7.1.5 Goertek INC.

- 7.1.6 STMicroelectronics NV

- 7.1.7 Omron Corporation

- 7.1.8 Alps Alpine Co. Ltd

- 7.1.9 Infineon Technologies AG

- 7.1.10 TE Connectivity Ltd

- 7.1.11 NXP Semiconductors NV (Freescale)

- 7.1.12 InvenSense Inc. (TDK Corporation)

- 7.1.13 ROHM Co. Ltd

- 7.1.14 Honeywell International Inc.

- 7.1.15 Melexis

- 7.2 Vendor Ranking for the Top 5 Vendors Across the End-user Verticals

- 7.3 Vendor Market Share for the Top 15 Vendors in 2021

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET