PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1687854

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1687854

Security Orchestration - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

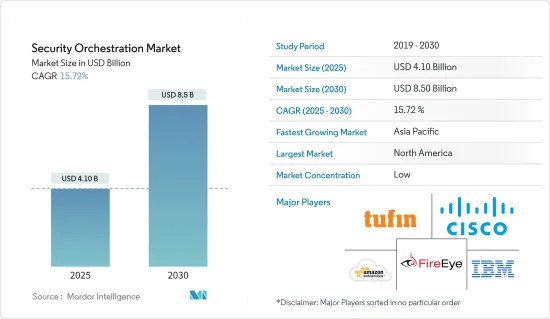

The Security Orchestration Market size is estimated at USD 4.10 billion in 2025, and is expected to reach USD 8.50 billion by 2030, at a CAGR of 15.72% during the forecast period (2025-2030).

The implementation of security orchestration across various organizations can help manage security alerts and prevent severe cyber-attacks. As the sophistication level in cyber-attacks is increasing, security vendors are trying to develop better orchestration platforms to provide proactive and holistic security architecture to handle critical business applications.

Key Highlights

- An increase in the security breaches and occurrences due to dramatic growth in the BYOD trend affecting SMEs, along with the rapid deployment and development of cloud-based solutions, is fueling the application of security orchestration among various organizations.

- A rise in the application of network forensics is expected to drive the market demand, as a growing number of companies are adopting the security orchestration platform to monitor and manage their computer network traffic.

- Growing adoption of various IT enabled services and solutions, due to the growing popularity of connected devices, has further boosted the amount of data generated daily, subsequently resulting in a vast scope for potential vulnerabilities that need effective management and containment.

- Implementation of these solutions has also enabled improved adherence to audit and compliance requirements easily, with proactive policy enforcement and audit and compliance reports, such as ITIL, PCI, Health Insurance Portability and Accountability Act (HIPAA), Sarbanes-Oxley Act (SOX), and Gramm-Leach-Bliley Act. These factors have been aiding the growth of the market.

Security Orchestration Market Trends

IT and Telecommunication Sector is Projected to Record Significant Growth

- The IT and telecommunication industry offers a wide range of global and domestic services for connecting millions of customers. This diverse ecosystem is more prone to frequent cyber attacks, as they are highly dependent on their infrastructure, network, and databases to perform any operation.

- Telecom organizations typically store customers' personal information, such as names, addresses, and financial data. Information-sensitive data is a compelling target for insiders or cyber-criminals to steal money, blackmail customers, or launch further attacks. Therefore, the industry demands a greater focus on updated solutions, the right tools, highly trained personnel, and the ability to respond to threats immediately.

- SOAR tools aid IT teams in defining, standardizing, and automating organizations' incident response activities. Most IT organizations use these tools to automate security operations and processes, respond to incidents, and manage vulnerabilities and threats. Moreover, security orchestration reduces the threat response and resolution time for IT professionals working in enterprise security.

- With the increased data connectivity with the cloud as well as IoT taking center stage in the IT sector, security has been a top priority for the all the organizations in the industry to protect themselves from the data breaches. Further, COVID-19 pandemic has led Information and communication technology organizations to rethink their business processes and improve their network performance to provide their customers with reliable services throughout the pandemic, specially when the demand for telecom networks has doubled. Thus, companies are adopting these security orchestration solutions thereby driving the market growth rate.

North America Accounts for the Largest Market Share

- North America dominates the security orchestration market, owing to many prominent security orchestration vendors across the region, such as IBM Corporation, DXC Technology Company, Cisco System Inc., FireEye Inc., etc. Factors such as the growing end-user industries, government expenditure toward critical infrastructure, well-established R&D centers, and the demand for advanced security technology across the region are expected to drive market growth.

- The growing number of cyber attacks in the region further contributes to the market growth. In 2021, The National Security Agency (NSA), the Cybersecurity and Infrastructure Security Agency (CISA), and the Federal Bureau of Investigation (FBI) reportedly witnessed occurrences involving ransomware against 14 of the 16 critical infrastructure sectors in the United States, including the Defense Industrial Base, Emergency Services, Food and Agriculture, Government Facilities, and Information Technology Sectors.

- Also, various organizations have admitted that network complexity has increased over the past few years and will continue to increase over the next five years. Therefore, there is a high need for network security to stop hacking and cyber-attacks from securing industrial processes, and that is where security orchestration plays its part.

- Further, the region is witnessing an explosion of new cloud tools adopted for hybrid and multicloud environments, while at the same time, established cloud platforms are pivoting to fit into the new hybrid reality.

Security Orchestration Industry Overview

The security orchestration market is highly competitive and consists of several major players. In terms of market share, few major players currently dominate the market. Moreover, due to the emergence of the cloud network segment, most companies are increasing their SOAR market presence, tapping customers across the subsequent markets. Further, the players are opting for various strategies, such as collaborations and solution launches, thereby contributing to the market growth rate. For instance:

- March 2023-IBM and Cohesity have formed a new partnership to meet organizations' essential need for better data security and reliability in hybrid cloud settings. IBM Storage Defender is being developed to use AI and event monitoring across various storage platforms through one single window to assist in safeguarding organizations' data layer from threats, including ransomware, human error, and attack.

- February 2023-Morado Intelligence, a threat intelligence company that assists clients with their needs for cyber threat intelligence and security operations optimisation, and Cyware, a provider of the technology platform to build low-code SOAR and threat intel automation powered Cyber Fusion Centres for businesses and MSSPs/MDRs, as well as threat intelligence sharing solutions for ISACs and ISAOs, have formed a partnership. The partnership's primary objective is to make it easier for Morado's robust client portfolio to use Cyware's advanced TIP & SOAR modules to effectively ingest, enhance, analyze, and respond on threat data.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Impact of COVID-19 on the market

5 Market Dynamics

- 5.1 Market Drivers

- 5.1.1 Rising Trend of Automated Security Operation for Seamless Workflow

- 5.1.2 Need of Disparate Cybersecurity Technologies to Handle Network Complexity

- 5.2 Market Restraints

- 5.2.1 Lack of Awareness among Professionals

- 5.3 Technology Snapshot

6 MARKET SEGMENTATION

- 6.1 Type

- 6.1.1 Software

- 6.1.2 Services

- 6.2 End-user Industry

- 6.2.1 BFSI

- 6.2.2 IT and Telecommunication

- 6.2.3 Government and Defence

- 6.2.4 E-commerce

- 6.2.5 Other End-user Industries

- 6.3 Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 United Kingdom

- 6.3.2.2 France

- 6.3.2.3 Germany

- 6.3.2.4 Rest of Europe

- 6.3.3 Asia-Pacific

- 6.3.3.1 China

- 6.3.3.2 Japan

- 6.3.3.3 Australia

- 6.3.3.4 Rest of Asia-Pacific

- 6.3.4 Rest of the World

- 6.3.4.1 Latin America

- 6.3.4.2 Middle-East & Africa

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 IBM Corporation

- 7.1.2 Tufin Software Technologies Ltd

- 7.1.3 DXC Technology Company

- 7.1.4 Cisco System Inc.

- 7.1.5 Swimlane LLC

- 7.1.6 RSA Security LLC

- 7.1.7 FireEye Inc.

- 7.1.8 DFLabs SpA

- 7.1.9 Palo Alto Networks Inc.

- 7.1.10 Siemplify Ltd

- 7.1.11 Accenture PLC

- 7.1.12 Amazon Web Services Inc.

- 7.1.13 Cyberbit Ltd

- 7.1.14 Forescout Technologies Inc.

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS