PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1433779

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1433779

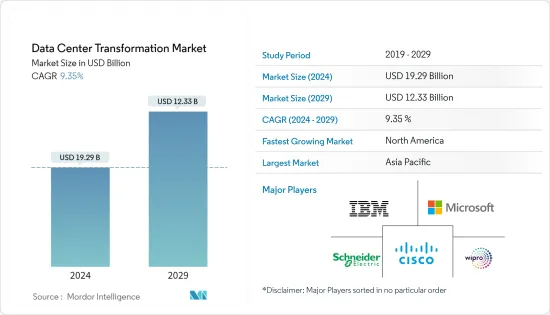

Data Center Transformation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

The Data Center Transformation Market size is estimated at USD 19.29 billion in 2024, and is expected to reach USD 12.33 billion by 2029, growing at a CAGR of 9.35% during the forecast period (2024-2029).

Data center providers across the globe are gradually moving towards data center transformation in order to increase overall efficiency whilst reducing operational costs. Owing to the rapidly rising adoption of cloud, Ineternet of Things (IoT), and big data analytics across various enterprises as a part of their digital transformation strategy, the burden on the data centers is also increasing, leading to the growth in the data centers globally.

Key Highlights

- Moreover, data center traffic across the world is also increasing, considering the number of increasing communicating devices and more enterprises switching to software-as-a-service (SaaS)-based applications, as forecasted by Cisco, which will also drive the market.

- With the increasing reliability and the increase in the number of data centers around the world, data center providers are finding it difficult to maintain consistency and operational efficiency

- Demand for data center services increased in many sectors which are dependent on digital infrastructures and this has resulted in an increase in the demand for Data Center Network Services. The need for data centres is increasing as a result of the rising number of enterprises and education institutions around the world who are Internet based, which means that they have to provide required program availability and data security.

- Energy efficiency considerations are also gaining importance among data centers since energy accounts for almost 40% of total costs (according to network strategy and technology company Ciena). Infrastructure management, as a part of the data center transformation, is expected to gain traction over the years, considering the attempt to increase energy efficiency as a cost-saving measure.

- The market for data center transformation was positively affected by the COVID 19 pandemic. Increasing awareness of the advantages provided by cloud computing to deliver a high security, reliable IT infrastructure and growing demand for building local data centres has also helped drive Data Centres growth.

Data Center Transformation Market Trends

Increasing Significance of E-commerce Databases are Expected to Grow at a Significant Rate

- For e commerce companies, data centres offer a number of significant advantages. In addition, they need to take advantage of the data that they collect and use it for extremely useful customer insights and business process optimisation.

- The growing importance of e commerce databases is the key driver for expanding data centres around the world. In order to store and transfer these data sets for a variety of organizational tasks, e.g. branding, promotion or anything like that, Data Centres are being used by businesses selling on the Internet.

- Through the acquisition of e-commerce data, online retailers monitor all the many components of their e-commerce, such as analytics or customer information. It is also expected that rising digital transformation in emerging nations fuels data centre market growth.

- Consequently, the market for data centres has been significantly stimulated by developing economies like China and India. At this phase of digital transformation, efficient data centers and related solutions are being developed due to the evolution of technology.

North America Occupies the Largest Market Share

- The North American region holds the largest market share of the global cloud and internet data centers, according to China Internet Network Information Center (CNNIC). This high share can also be because many major players are headquartered in this region.

- North America also contributes substantially to the global data center demand from various end-user industries such as IT, BFSI, retail, and healthcare.

- The Federal government's Data Center Optimization Initiative (DCOI) primarily aims to encourage data center players to consolidate the inefficient infrastructure, optimize existing facilities, achieve cost savings, and transition to a more efficient infrastructure.

- Due to the increased focus on dependability and sustainability, data center owners and operators must investigate cutting-edge technologies like fuel-cell energy storage. Older assets that might be deemed unsuitable for modern colocation are receiving new opportunities thanks to cryptocurrency mining, a comparatively recent source of demand.

- To generalize the statement, through this initiative, the government intends to reduce the costs of physical data centers by a minimum of 25% by the end of the fiscal year. The dominance of this region in the market, combined with the increasing need to reduce operational costs, provides scope for adopting data center transformation solutions, hence driving the market.

Data Center Transformation Industry Overview

The data center transformation market is semi-conslidated owing to the presence of many players in the market operating in the domestic as well as the international market. The market is moderately concentrated, with key players adopting product and design innovation strategies. Some of the major players in the market are IBM Corporation, Cisco Systems, Inc., and Wipro, among others.

In September 2023 - Schneider Electric SE announced at its Collobration with investors a USD 3 billion multi-year agreement with Compass Datacenters. The agreement extends the companies' existing relationship that integrates their respective supply chains to manufacture and deliver prefabricated modular data center solutions.

In October 2022, Kyndryl announced a comprehensive hybrid cloud solution in collaboration with Dell Technologies and Microsoft Corporation. This solution empowers clients in data center, remote, and mainframe environments to expedite their cloud transformation journey by leveraging the infrastructure offered by Dell, Kyndryl's managed services, and Microsoft Azure.

In January 2022, IBM launched the IBM Z and Cloud Modernization Center to facilitate the adoption of hybrid clouds. The center serves as a digital gateway to a wide range of tools, resources, training, and ecosystem partners, assisting IBM Z clients in accelerating the digitization of their applications, processes, and data in a hybrid cloud environment.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Need to Reduce Costs and Increase Efficiency of Data Centers

- 5.1.2 Adoption of Cloud-based Services

- 5.1.3 Increasing Significance of E-commerce Databases are Expected to Grow at a Significant Rate

- 5.2 Market Restraints

- 5.2.1 ROI Concerns Over the Investment across Low Load Data Centers

6 MARKET SEGMENTATION

- 6.1 By Services

- 6.1.1 Consolidation Services

- 6.1.2 Optimization Services

- 6.1.3 Automation Services

- 6.1.4 Infrastructure Management

- 6.2 By Level of Data Center

- 6.2.1 Tier 1

- 6.2.2 Tier 2

- 6.2.3 Tier 3

- 6.2.4 Tier 4

- 6.3 By End User

- 6.3.1 Data Center Providers

- 6.3.2 Enterprises

- 6.3.2.1 IT and Telecom

- 6.3.2.2 BFSI

- 6.3.2.3 Healthcare

- 6.3.2.4 Retail

- 6.3.2.5 Manufacturing

- 6.3.2.6 Aerospace, Defense, and Intelligence

- 6.3.2.7 Other End Users

- 6.4 By Geography

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia Pacific

- 6.4.4 Latin America

- 6.4.5 Middle East & Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 IBM Corporation

- 7.1.2 Cisco Systems, Inc.

- 7.1.3 NetApp, Inc.

- 7.1.4 NTT Communications

- 7.1.5 Dell EMC (Dell Inc.)

- 7.1.6 Microsoft Corporation

- 7.1.7 Schneider Electric SE

- 7.1.8 HCL Technologies Limited

- 7.1.9 Accenture plc

- 7.1.10 Wipro Technologies

- 7.1.11 Hitachi Vantara Federal, Corporation

- 7.1.12 Emerson Network Power, Inc

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS