PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1687832

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1687832

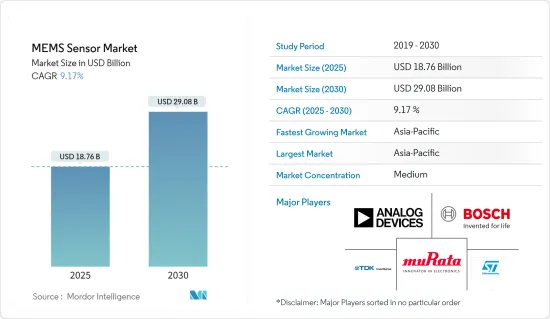

MEMS Sensor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The MEMS Sensor Market size is estimated at USD 18.76 billion in 2025, and is expected to reach USD 29.08 billion by 2030, at a CAGR of 9.17% during the forecast period (2025-2030).

The rising popularity of IoT in semiconductors, the growing need for smart consumer electronics and wearable devices, and the enhanced adoption of automation in industries and residences are some significant factors influencing the growth of the studied market.

Key Highlights

- MEMS sensors deliver multiple advantages, such as accuracy, reliability, and the prospect of making smaller electronic devices. As a result, they have gained considerable traction in the past few years. Miniaturized consumer devices, such as IoT-connected devices and wearables, are emerging applications of MEMS sensors in the market.

- According to the IFR forecasts, global adoption is expected to increase significantly to 518,000 industrial robots operational across factories all around the globe in the next few years. The positive growth trajectory of the industrial robots market is expected to drive the demand for MEMS sensors during the same period.

- Moreover, the demand for smartphones has been witnessing an upsurge owing to several factors increasing disposable income, the advent of 5G, and the development of telecom infrastructure. For instance, according to Ericsson, worldwide smartphone subscriptions are expected to reach 7,690 million in the next few years.

- Furthermore, pressure sensors are anticipated to witness the fastest growth rate as they are used in numerous application areas, such as biomedicine, automotive electronics, small home appliances, and wearable and fitness electronics. Other MEMS sensors, such as microphones and ultrasonic MEMS sensors, environmental sensors, and microbolometers, are expected to hold a significant share of the market studied.

- The US-based Boston Semi Equipment (BSE), a semiconductor test handler company, recently received repeat orders from automotive customers for multiple Zeus gravity test handlers configured for MEMS high-power and pressure IC testing applications. Zeus handlers have a flexible range for MEMS pressure sensing test cells and offer high voltage levels in a production handler for testing IGBT, MOSFET, gate drivers, GaN, and SiC power semiconductors.

- In addition, the factors challenging the market's growth include the increase in the cost of MEMS sensors implementation due to interface design considerations and the lack of a standardized fabrication process of MEMS. The standardization in MEMS is undoubtedly less advanced than it is for conventional semiconductor processes and model environments. However, the standard procedure is bound to happen in the next few years, making the impact of the challenge gradually low in the next few years.

- Due to the COVID-19 pandemic, certain types of MEMS sensors significantly spiked in demand. For instance, the demand for thermopiles and microbolometers used in temperature guns and thermal cameras increased because of the need for contactless monitoring of people's temperatures. Moreover, real-time polymerase chain reaction (PCR) diagnostic tests for detecting COVID-19 and microfluidics for DNA sequencing gained substantial market relevance.

- Furthermore, pressure and flowmeters in ventilators grew because of hospital intensive care units (ICUs). Therefore, the pandemic highlighted the criticality of having a robust healthcare infrastructure, and the industry's subsequent developments are expected to propel market demand over the forecast period.

MEMS Sensor Market Trends

Automotive Sector Expected to Drive the Market Growth

- MEMS sensors are used in the automobile industry and intelligent automobiles. MEMS sensor development is expected to focus on the automotive industry. It is widely used in engine e(ABS), electronic stability program (ESP), electronic control suspension (ECS), electric hand brake (EPB), slope starter auxiliary (HAS), tire pressure monitoring (EPMS), car engine stabilization, angle measure, and heartbeat detection, as well as adaptive navigation systems.

- The increasing demand for safety and security in automobiles is one of the main factors that play a vital role in the market's growth. According to the WHO, more than 1.35 million people yearly are killed in road accidents. MEMS sensors play a critical role in improving the safety features of vehicles and act as a catalyst for the market's growth.

- OMRON has newly released the FH-SMD Vision Sensor series for robot arms, which can be used for fast detection for humans and flexibility for auto-selection of the compartment. These can be mounted on a robot to recognize random (bulk) automotive parts in three sizes that are hard to use with conventional robots and improve productivity, thereby saving space, inspection, and pick and place.

- For instance, in April 2022, Tata Motors announced projects to finance INR 24,000 crores (USD 3.08 billion) in its passenger motorcar business over the next five years. Furthermore, in March 2022, MG Motors, owned by China's SAIC Motor Corp., declared plans to expand USD 350-500 million in confidential equity in India to fund its future requirements, including EV expansion. Such developments in automobiles will further drive the studied market growth.

- Furthermore, with the development of new intelligent vehicles, such as new energy vehicles and driverless vehicles, MEMS sensors may occupy a more significant share of the automotive sensor market in the future. Recently, InvenSense presented its vast portfolio of innovative MEMS sensor technologies at CES. For instance, it released the IMU IAM-20685 high-performance automotive 6-Axis MotionTracking sensor platform for ADAS and autonomous systems and TCE-11101, a miniaturized ultra-low-power MEMS platform for direct and accurate detection of CO2 in home, industrial, automotive, healthcare, and other applications.

Asia-Pacific Expected to Hold Significant Market Share

- Asia-Pacific is anticipated to be the most extensive market for MEMS sensors due to economies, such as India, Japan, and China, along with the increasing growth of the consumer electronics and automobile segments. According to Cisco, this year, around 311 million and 439 million wearable device units are expected to be sold in Asia-Pacific and North America, respectively. This is further driving the demand for MEMS sensors in the region.

- China has witnessed a significant increase in the usage of MEMS sensors in the past couple of years due to the rise in its automotive and consumer markets and the export of smartphones, tablets, drones, and other microsystem and semiconductor-enabled products. Multiple MEMS sensors, such as accelerometers, gyroscopes, pressure sensors, and radio frequency (RF) filters, have been imported into China for product assembly.

- Moreover, the Chinese administration also views its automotive industry, including the auto parts sector, as one of the major industries. The Central Government expects China's automobile output to reach 35 million units in the next few years. This is posed to make the automotive sector one of the prominent uses of MEMS sensors in China.

- According to the India Brand Equity Foundation (IBEF), the Indian appliances and consumer electronics (ACE) market has registered a CAGR of 9% to achieve INR 3.15 trillion (USD 48.37 billion) this year. The government has taken several initiatives to propel this product, including the National Policy on Electronics 2019, which aims to promote domestic electronic manufacturing and export a complete value chain to achieve a turnover of approximately USD 400 billion in the next few years. Such regional government initiatives are estimated to bolster the studied market.

- The Indian automotive industry is well-positioned for growth economically and demographically, serving domestic interest and export possibilities, which will rise shortly. As a part of the Make in India scheme, the Government of India aims to make automobile fabricating the main driver for the initiative. The system is poised to make the passenger vehicles market rise to 9.4 million units in the next few years, as underlined in the 2016-26 Auto Mission Plan (AMP). This factor is expected to raise the adoption of MEMS sensors in the region's automotive sector.

- Furthermore, Minbea Mitsumi Inc., based in Japan, recently announced that Mitsumi Electric Co. Ltd, a company subsidiary, has reached an agreement with Omron Corporation to acquire the semiconductor and MEMS Manufacturing plant as the MEMS product development function at OMRON's Yasu facility through MITSUMI. Acquiring the MEMS sensor business will strengthen Mitsumi's sensor business, which is one of its most important.

MEMS Sensor Industry Overview

The MEMS sensors market is relatively competitive and consists of numerous significant players. In terms of market share, a few crucial players, such as STMicroelectronics NV, Invensense Inc. (TDK Corp), Bosch Sensortec GmbH (Robert Bosch GmbH), Analog Devices Inc., and Murata Manufacturing Co. Ltd, currently hold a significant market share. Additionally, these companies continuously innovate their products to increase their market share and profitability.

- April 2022: Bosch Sensortec released its first capacitive barometric pressure sensor, the BMP581. The energy-efficient barometric is a highly accurate altitude-tracking IC that can provide precise location information for indoor localization, floor detection, and navigation applications. The sensor supports multiple communication interfaces, including I2C, I3C, and SPI digital serial interfaces. Its small size and low power consumption create it ideal for smart wearables, hearables, and IoT applications.

- January 2022: TDK introduced the most recent MEMS microphone with SoundWire functionality. The new T5828 MEMS (micro-electromechanical system) microphone complies with the MIPI SoundWire protocol. It includes 68dBA SNR (signal-to-noise ratio) and acoustic activity detect elements with always-on ultra-low power mode.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Safety Concerns in the Automotive Industry

- 5.1.2 Emergence of Automation and Industry 4.0

- 5.2 Market Challenges

- 5.2.1 Increase in Overall Cost of MEMS Sensors due to Multiple Interface Design Complexity

- 5.2.2 Lack of Standardized Fabrication Process for MEMS

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Pressure Sensors

- 6.1.2 Inertial Sensors

- 6.1.3 Other Types

- 6.2 By End-user Industry

- 6.2.1 Automotive

- 6.2.2 Healthcare

- 6.2.3 Consumer Electronics

- 6.2.4 Industrial

- 6.2.5 Aerospace and Defense

- 6.3 By Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 Germany

- 6.3.2.2 United Kingdom

- 6.3.2.3 France

- 6.3.2.4 Italy

- 6.3.2.5 Rest of Europe

- 6.3.3 Asia-Pacific

- 6.3.3.1 China

- 6.3.3.2 Japan

- 6.3.3.3 India

- 6.3.3.4 South Korea

- 6.3.3.5 Rest of the Asia-Pacific

- 6.3.4 Rest of the World

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 STMicroelectronics NV

- 7.1.2 InvenSense Inc. (TDK Corp.)

- 7.1.3 Bosch Sensortec GmbH (Robert Bosch GmbH)

- 7.1.4 Analog Devices Inc.

- 7.1.5 Murata Manufacturing Co. Ltd

- 7.1.6 Kionix Inc. (ROHM Co Ltd)

- 7.1.7 Infineon Technologies AG

- 7.1.8 Freescale Semiconductors Ltd (NXP Semiconductors NV)

- 7.1.9 Panasonic Corporation

- 7.1.10 Omron Corporation

- 7.1.11 First Sensor AG (TE Connectivity)

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET