PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044180

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044180

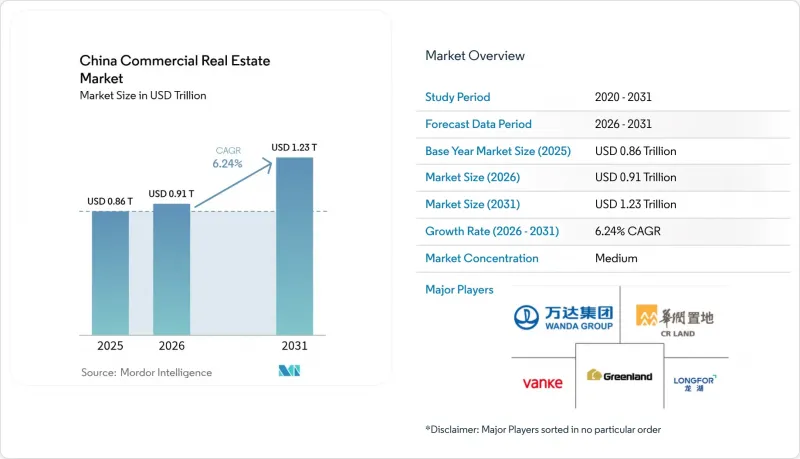

China Commercial Real Estate - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The China commercial real estate market size expanded from USD 855.26 billion in 2025 to USD 909.22 billion in 2026 and is projected to reach USD 1,234.6 billion by 2031, advancing at a 6.31% CAGR between 2026 and 2031.

This growth arc stems from a decisive turn toward income-generating assets and high-throughput logistics facilities as developers confront elevated refinancing costs and soft office absorption. Omnichannel retail platforms, mandatory on-site renewable-energy rules, and an enlarged C-REIT pipeline are together redefining capital deployment priorities. While offices still commanded 34% of value in 2025, distribution centers are capturing the incremental square footage, aided by 24-hour e-commerce fulfillment timelines. Rental operations, although just 38% of the 2025 deal value, are gaining favor as institutional capital prizes predictable yields over volatile pre-sales inflows.

China Commercial Real Estate Market Trends and Insights

Resilient Logistics Demand From Omni-Channel Retail & On-Shoring

E-commerce platforms shortening delivery windows are driving robust warehouse leasing, even as traditional mall footfall plateaus. GLP signed 7.8 million m2 of leases in Q2 2025, a 16% uptick, while keeping portfolio occupancy at 87%. Multinationals' reshoring distribution nodes to hedge geopolitical risk have amplified absorption around port-adjacent and inland rail hubs. Developers respond by pairing automated sortation belts with cold-chain bays, an amenity mix that earns 15-20% rent premiums. Cross-border parcel volumes in lower-tier cities further reinforce demand for regional fulfillment hubs. Together, these themes sustain a logistics pipeline that outpaces all other asset classes.

Expanded C-REIT Pipeline Widening Exit Options For Developers

The December 2025 decision to let Grade-A offices, malls, and four-star hotels enter the C-REIT universe unlocked CNY 207 billion (USD 29.6 billion) of fresh equity across 77 trusts. Seasoned sponsors now enjoy a liquid path out of construction risk, reducing dependence on offshore bonds capped by higher spreads. GLP disbursed USD 171 million in 2024 dividends from its listed vehicles, underscoring the attractiveness of near-100% payout ratios. Eligibility hurdles, three-year operating record, 90% occupancy, and investment-grade leverage concentrate benefits on large players, accelerating industry consolidation. Private-placement REITs pricing at 5-6% yields, versus 3-4% for public peers, reveal a two-tier appetite that mirrors sponsor credit profiles.

Structural Oversupply Of Legacy Office Stock Post-Hybrid Shift

Shenzhen's vacancy touched 29% in Q3 2025 as work-from-anywhere policies compressed per-capita footprints and prompted lease non-renewals. Shanghai posted 23.6%, while Beijing steadied near 16.9%. Incentives such as 6-12 months rent-free and turnkey fit-outs protect occupancy but erode landlord margins. Roughly 72 million m2 of CBD stock, much of it built before 2015, lacks the smart-building functions tenants now treat as a baseline. Owners unable to fund upgrades experience value write-downs, pushing distress-sale inventory into the pipeline and dragging overall pricing.

Other drivers and restraints analyzed in the detailed report include:

- State-Backed Urban-Renewal Grants For Grade-A Office Retrofits

- Data-Center & AI Edge-Node Land-Banking In Tier-1 And 1.5 Cities

- Elevated Borrowing Costs & Offshore Refinancing Hurdles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Logistics captured 7.8 million m2 of fresh leases in 2025 and is forecast at a 7.72% CAGR to 2031, the fastest among property categories. Offices, though still holding a 34% China commercial real estate market share in 2025, wrestle with hybrid-driven downsizing and persistent vacancy above 25% in Shenzhen and Shanghai. Retail vacancy plateaued near 10% across prime centers, but secondary malls lag, reinforcing a bifurcated outlook. Other segments, data centers, life-science labs, and mixed-use campuses- remain small yet draw outsized capital due to sticky leases and inflation-linked rent ladders.

Build-to-suit contracts limit speculative risk for warehouses: GLP posted 87% occupancy across 29 million m2 in 2024, highlighting robust demand. Office landlords accelerate wellness retrofits and flexible space tie-ups, yet 9.9% rent erosion in 2025 underlines oversupply pressure. Retail owners embrace omnichannel nodes and themed experiences; Bain estimates O2O penetration hit 50% in 2024. Data-center operators such as GDS and Keppel bundle renewable power and edge racks, narrowing the divide between property and digital infrastructure.

The China Commercial Real Estate Market Report is Segmented by Property Type (Offices, Retail, Logistics, Others), by Business Model (Sales, Rental), by End-User (Individuals/Households, Corporates & SMEs, Institutions/Government/NGOs), and by Geography (Shanghai, Beijing, Shenzhen, Guangzhou, Chengdu, Rest of China). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Wanda Group

- China Resources Land

- Greenland Group

- Longfor Group

- China Vanke

- Seazen Holdings

- China Overseas Land & Investment

- CapitaLand China

- Sino-Ocean Group

- Sun Hung Kai Properties

- Henderson Land Development

- Wharf REIC

- Prologis China

- GLP China

- Goodman China

- JD Property

- Cainiao Smart Logistics

- GDS Holdings

- Keppel Land China

- Brookfield China Logistics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Commercial-Real-Estate Buying Trends - Socio-economic & Demographic Insights

- 4.3 Rental-Yield Analysis

- 4.4 Capital-Market Penetration & REIT Presence

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Insights into Real-Estate Tech & Start-ups

- 4.8 Insights into Existing & Upcoming Projects

- 4.9 Market Drivers

- 4.9.1 Resilient logistics demand from omni-channel retail & on-shoring (mainstream)

- 4.9.2 Expanded C-REIT pipeline widening exit options for developers (mainstream)

- 4.9.3 State-backed urban-renewal grants for Grade-A office retrofits (mainstream)

- 4.9.4 Mandatory on-site PV & storage for >=20 000 m2 assets lowering opex (under-radar)

- 4.9.5 Data-centre & AI edge-node land-banking in Tier-1/1.5 cities (under-radar)

- 4.9.6 Tokenised fractional ownership platforms unlocking retail capital (under-radar)

- 4.10 Market Restraints

- 4.10.1 Structural oversupply of legacy office stock post-hybrid shift (mainstream)

- 4.10.2 Elevated borrowing costs & offshore refinancing hurdles (mainstream)

- 4.10.3 Vacancy pressure in lower-tier malls amid consumption polarisation (mainstream)

- 4.10.4 Grid-capacity caps delaying power-intensive redevelopments (under-radar)

- 4.11 Value / Supply-Chain Analysis

- 4.11.1 Overview

- 4.11.2 Developers & Contractors - Key Quantitative & Qualitative Insights

- 4.11.3 Brokers & Agents - Key Quantitative & Qualitative Insights

- 4.11.4 Property-Management Firms - Key Quantitative & Qualitative Insights

- 4.11.5 Valuation Advisory & Other Services

- 4.11.6 Building-Materials Ecosystem & Developer Partnerships

- 4.11.7 Strategic Real-Estate Investors / Buyers

- 4.12 Porter's Five Forces

- 4.12.1 Bargaining Power of Suppliers

- 4.12.2 Bargaining Power of Buyers

- 4.12.3 Threat of New Entrants

- 4.12.4 Threat of Substitutes

- 4.12.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Property Type

- 5.1.1 Offices

- 5.1.2 Retail

- 5.1.3 Logistics

- 5.1.4 Others

- 5.2 By Business Model

- 5.2.1 Sales

- 5.2.2 Rental

- 5.3 By End-user

- 5.3.1 Individuals / Households

- 5.3.2 Corporates & SMEs

- 5.3.3 Others (institutions, governments, NGOs)

- 5.4 By Cities

- 5.4.1 Shanghai

- 5.4.2 Beijing

- 5.4.3 Shenzhen

- 5.4.4 Guangzhou

- 5.4.5 Chengdu

- 5.4.6 Rest of China

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Company Profiles {(includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, Recent Developments)}

- 6.3.1 Wanda Group

- 6.3.2 China Resources Land

- 6.3.3 Greenland Group

- 6.3.4 Longfor Group

- 6.3.5 China Vanke

- 6.3.6 Seazen Holdings

- 6.3.7 China Overseas Land & Investment

- 6.3.8 CapitaLand China

- 6.3.9 Sino-Ocean Group

- 6.3.10 Sun Hung Kai Properties

- 6.3.11 Henderson Land Development

- 6.3.12 Wharf REIC

- 6.3.13 Prologis China

- 6.3.14 GLP China

- 6.3.15 Goodman China

- 6.3.16 JD Property

- 6.3.17 Cainiao Smart Logistics

- 6.3.18 GDS Holdings

- 6.3.19 Keppel Land China

- 6.3.20 Brookfield China Logistics

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment