PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1334424

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1334424

United Kingdom White Cement Market Size & Share Analysis - Growth Trends & Forecasts (2023 - 2028)

The UK White Cement Market size is expected to grow from 798.55 kilotons in 2023 to 990.86 kilotons by 2028, at a CAGR of 4.41% during the forecast period (2023-2028).

The COVID-19 pandemic caused lockdowns nationwide, messed up manufacturing and supply chains, and stopped all construction there. This had a big effect on the market in 2020. But in 2021, things started to improve, and the market continued to grow for the rest of the projection period.

Key Highlights

- The rising construction sector in the United Kingdom and the substitution of grey cement due to white cement's superior properties will drive the market in the long run.

- However, the high production cost will likely restrain the market over the forecast period.

- An increased emphasis on innovation and artistic and aesthetic senses in the building is expected to certainly present an opportunity during the forecast period.

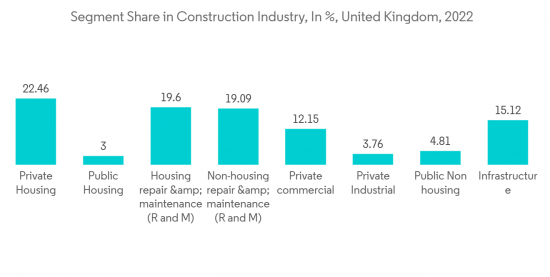

- Due to increased demand for white cement from commercial, industrial, and infrastructure applications, the non-residential segment accounts for the major share by application.

UK White Cement Market Trends

Type I Cement to Dominate

- Portland Cement Type I can be used for all architectural or structural concrete construction types where a whiter or brighter color may be needed. It is a general-purpose white cement where the special properties of other types are not required.

- Type I white Portland cement is used as a base to produce vibrant and true colors prized in almost any architectural concrete application. This product type may also be used to satisfy low alkali requirements.

- There is a sub-product type in type I cement, which includes water repellant. It is a specialty product that finds its usage in plastering applications, masonry mortar, tile grout, and as a component in cementitious coatings and water-repellent products.

- According to the Office for National Statistics (UK), GDP from the construction sector in the United Kingdom fell to GBP 32,120 million (USD 35.80 billion) in the third quarter of 2022, down from GBP 32,188 million (USD 39.15 billion) in the second quarter. Further, the GDP from construction in the United Kingdom is expected to be around GBP 30,940 million (USD 37.60 billion) in 2023 and GBP 31,064.00 million (USD 37.80 billion) in 2024.

- Further, a GBP 11.5 billion (USD 14.8 billion) budget was confirmed for allocation in the country's Affordable Homes Program by the Government, which targets to deliver around 180,000 new homes over five years between 2021 and 2026. The program is also due to unlock an added budget of GBP 38 billion (USD 49 billion) for public and private investment in affordable housing.

- The National House Building Council (NHBC) revealed data showing a high increase of 25% in the number of new homes registered to be built in the United Kingdom in Q1 2022 compared to the same period in 2021. The total number of units registered increased from 36,665 in Q1 2021 to 45,991 in Q1 2022.

- The United Kingdom is engaged in several construction projects, predicted to increase demand for white cement in the next years. For instance, a 40-story residential tower and a 14-story office building are being built at Albion Street in Central Manchester with a USD 333 million investment, whose construction is expected to be finished by 2024.

- Moreover, the factors mentioned above and a growing focus on using white cement for better aesthetic and artistic senses provide opportunities for white cement to be used in the construction sector at a healthy rate during the forecast period.

Non-Residential Application to Dominate the Market

- The non-residential sector is one of the significant demanding markets for white cement globally. Increasing construction of new institutional buildings, office spaces, and other industrial constructions has majorly contributed to the rise in the demand for white cement in the United Kingdom.

- White cement is used in the industrial and institutional sectors for tile and paver-related repairs and construction projects. In the segment, white cement is used to build and restore new hospitals and educational facilities to enhance the exterior facades of those facilities.

- In its statistical presentation, the Office for National Statistics (United Kingdom) stated that the monthly construction output increased by 0.4% in volume terms in August 2022, following an upwardly revised 0.1% increase in July 2022. The main contributors to the rise seen in August 2022 were infrastructure, private industry, and private housing new work.

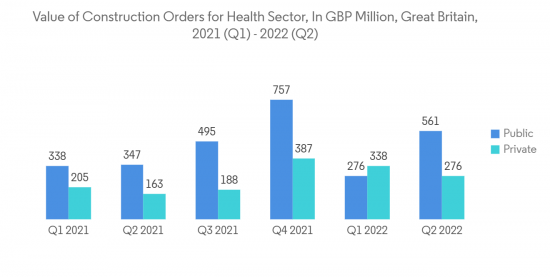

- According to the Office for National Statistics (United Kingdom), the value of construction orders for the health sector in Great Britain in the second quarter of 2022 was estimated to be around GBP 837 million (USD 1.01 billion). The public health construction segment accounting accounted for about two-thirds of the total value.

- The growing construction sector in the country is being pushed further ahead by various non-residential ongoing projects or projects that are due to start in 2023. For instance, the football club of Manchester City, in April 2023, had put forward its plans to invest GBP 300 million (USD 370 million) to increase the current capacity of 53,400 to 60,000 people by expanding the North Stand.

- Furthermore, the plans to revamp London's Liverpool Street station, estimated to be GBP 1.5 billion (USD 1.8 billion), are due to be unveiled in 2023 by Sellar, the developer behind The Shard. Sellar partnered with the Hong Kong-based Mass Transit Corporation and appointed Mace and Gardiner & Theobald consultants.

- All the factors above augment the growth of construction activities in the non-residential segment, thus, driving the demand for white cement in the country.

UK White Cement Industry Overview

The white cement market in the United Kingdom is consolidated, with the top five players accounting for a major share of the market. The key players in the market include Aggregate Industries, Cemex, S.A.B. de C.V., Hanson (HeidelbergCement AG), Breedon Group plc, and Cementir Holding N.V.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Demand from the Construction Industry

- 4.1.2 Substitution of Grey Cement due to White Cement's Superior Properties

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 High Production Cost

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Type

- 5.1.1 Type I

- 5.1.2 Type III

- 5.1.3 Other Types

- 5.2 Application

- 5.2.1 Residential

- 5.2.2 Non-residential

- 5.2.2.1 Commercial

- 5.2.2.2 Infrastructure

- 5.2.2.3 Industrial/Institutional

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Aggregate Industries (Holcim Group)

- 6.4.2 Breedon Group plc

- 6.4.3 Cementir Holding N.V.

- 6.4.4 Cemex S.A.B. de C.V.

- 6.4.5 CRH

- 6.4.6 Dragon Alpha Cement Ltd

- 6.4.7 Hanson (HeidelbergCement AG)

- 6.4.8 Southern Cement Limited (CRH Company)

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increased Emphasis on Innovation, Artistic and Aesthetic Senses in Building

- 7.2 Other Opportunities