PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1641902

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1641902

Composite Insulated Panels - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

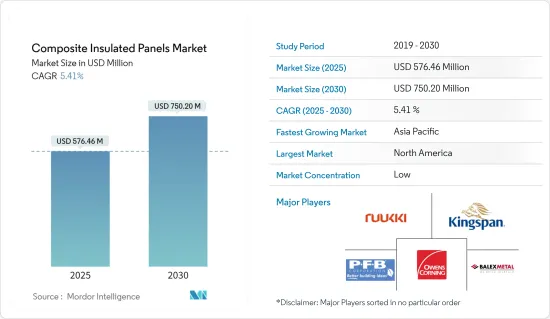

The Composite Insulated Panels Market size is estimated at USD 576.46 million in 2025, and is expected to reach USD 750.20 million by 2030, at a CAGR of 5.41% during the forecast period (2025-2030).

The COVID-19 pandemic negatively impacted the market. This was because of the shutdown of the manufacturing facilities and plants due to the lockdown and restrictions. Supply chain and transportation disruptions further created hindrances for the market. However, the industry witnessed a recovery in 2021, thus rebounding the demand for the market studied.

Key Highlights

- Over the short term, increasing demand from the construction sector and increasing cold storage applications are some of the factors driving the growth of the market studied.

- On the flip side, advancements in building technologies such as modular construction techniques are likely to hinder the growth of the market.

- However, growing smart city constructions are anticipated to provide numerous opportunities over the forecast period.

- North America dominated the market in terms of consumption, however, Asia-Pacific is expected to have the highest CAGR during the forecast period.

Composite Insulated Panels Market Trends

Increasing Demand from the Building Wall

- The outer walls are the major part of a building. Additionally, the external walls play a very important role in energy-saving buildings. Therefore, the wall's energy-saving technology is of much significance.

- Composite panels can be better applied to the engineering practice, in order to meet the development requirements of energy-saving buildings and housing industrialization. The energy-saving technologies are applied on mainly four kinds of walls, namely, traditional single wall, internal thermal insulation composition wall, external thermal insulation composite wall, and sandwich insulation panel wall.

- The increasing demand from the construction industry is one of the key factors driving the market for composite insulated panels market. Some of the large ongoing building construction projects across the world include the Magnolia Mixed-Use Complex project worth USD 1 billion in Texas, which is expected to be completed in Q1 2025. The Minamikoiwa 6-Chome District Type One Urban Redevelopment project in Tokyo, Japan is another such project, which is expected to complete in 2026. Thus, such construction projects are estimated to use composite insulated panels for walls of the building.

- Moreover, Asia-Pacific composite insulated panels market is anticipated to grow significantly during the forecast period with China leading the market owing to expanding construction and rapid industrial development. The growing building construction and renovation activities in the region are expected to surge the consumption of composite insulated panels. For instance, some of the ongoing building construction projects in the Asia-Pacific include the Hamamatsucho Shibaura 1 Chome Redevelopment project worth USD 3.17 billion, which is expected to be completed in 2030, in Tokyo, Japan. Another such project is the Wuhan Fosun Bund Center T1 project, which involves the construction of the Fosun Bund Center T1 in Wuhan, China. Therefore, increasing building construction projects are expected to drive the growth of composite insulated panels market in the region.

- Furthermore, the residential sector in India is on an increasing trend, with government support and initiatives further boosting the demand. According to the India Brand Equity Foundation (IBEF), the Ministry of Housing and Urban Development (MoHUA) allocated USD 9.85 billion in the 2022-2023 budget to construct houses and create funds to complete the halted projects. Therefore, increasing in the number of house constructions in the country is expected to create an upside demand for building walls, further boosting the demand for composite insulated panels market.

- All the aforementioned factors are expected to drive the demand of composite insulated panels from building walls application.

North-America to Dominate the Market

- The construction industry in North America is growing steadily, due to the improving commercial real estate sector and increased federal and state investment in public construction and institutional buildings. Some of North America's major building construction projects include the East River Mixed-Use Development project worth USD 2.5 billion. The project aims to provide better residential and office facilities in Texas, which is expected to be completed in 2040. Therefore, increasing investments from the building and construction industry is expected to create an upside for composite insulated panels.

- The United States dominated the North American composite insulated panels market, owing to the increasing construction activities in the country.

- According to the US Census Bureau, the value of private construction in the United States in 2022 was USD 1.43 trillion, which shows an increase of 10.47% compared to 2021, which amounted to USD 1.28 trillion. Residential construction spending in 2022 amounted to USD 899.1 billion, which showed an increase of 13.3% compared to 2021, while non-residential construction spending amounted to USD 530.1 billion, which showed a decrease of 9.1% compared to 2021. Therefore, increasing private construction in the United States is expected to create an upside demand for composite insulated panels market from the country's construction industry.

- Additionally, in May 2022, the the United States government announced to the allocation of over USD 110 billion for carrying out 4.3 thousand specific projects for modernizing airports and ports and rebuilding roads and bridges. These projects are expected to benefit around 3.2 thousand communities across the 50 states. Therefore, the expansion of constructing industry in the country is expected to create an upside demand composite insulated panels market from the building walls segment.

- Moreover, according to the US Census Bureau, the total new construction put in place was valued at about USD 1.79 trillion during year 2022, registering a growth rate of 10.20% compared to the USD 1.63 trillion in 2021 and is expected to rise through the years to come, which will further enhance the consumption of composite insulated panels from various building and construction applications.

- Furthermore, the Canadian construction industry is the second-largest in North America; it is expected to improve and grow at a decent pace, till 2024. For instance, according to Canada Mortgage and Housing Corporation, the number of dwelling units that were under construction in Canada in December of 2022 was approximately 334.1 thousand units, which showed an increase of 12.8% compared to 2021. Therefore, increasing construction activities in the country is expected to create an upside demand for composite insulated panels market.

- With the construction industry's growth, the demand for market studied is expected to increase significantly.

Composite Insulated Panels Industry Overview

The Composite Insulated Panels Market is fragmented in nature. The major players in this market (not in a particular order) include Kingspan Group, Rautaruukki Corporation, Balex-Metal, PFB Corporation, and Owens Corning, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand from the Construction Sector

- 4.1.2 Increasing Cold Storage Applications

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Advancements in Building Technologies, such as Modular Construction Techniques

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Product

- 5.1.1 Expanded Polystyrene (EPS) Panel

- 5.1.2 Rigid Polyurethane (PUR) and Rigid Polyisocyanurate (PIR) Panel

- 5.1.3 Glass Wool Panel

- 5.1.4 Other Products (Extruded Polystyrene Foam)

- 5.2 Application

- 5.2.1 Building Wall

- 5.2.2 Building Roof

- 5.2.3 Cold Storage

- 5.3 Skin Material

- 5.3.1 Continuous Fiber Reinforced Thermoplastics (CFRT)

- 5.3.2 Fiberglass Reinforced Panel (FRP)

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Alubel

- 6.4.2 ArcelorMittal

- 6.4.3 Balex-Metal

- 6.4.4 DANA Group of Companies

- 6.4.5 ITALPANNELLI SRL

- 6.4.6 Jiangsu Jingxue Insulation Technology Co. Ltd

- 6.4.7 Kingspan Group

- 6.4.8 Metecno

- 6.4.9 Owens Corning

- 6.4.10 PFB Corporation

- 6.4.11 Rautaruukki Corporation

- 6.4.12 Tata Steel

- 6.4.13 Zamil Steel Pre-Engineered Buildings Company Limited

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

8 Growing Smart City Construction

9 Other Opportunities