PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1689706

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1689706

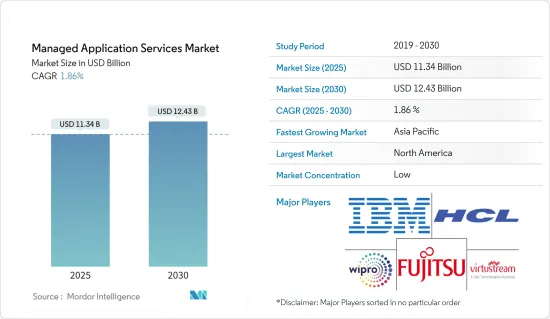

Managed Application Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Managed Application Services Market size is estimated at USD 11.34 billion in 2025, and is expected to reach USD 12.43 billion by 2030, at a CAGR of 1.86% during the forecast period (2025-2030).

Demand for end-to-end application hosting services will increase in the forecast period. The managed application services allow the organization to outsource specific IT requirements to a third-party service provider. The companies can reduce costs, boost productivity, and enhance application performance without spending time on implementation, maintenance, and upgradation of their IT-related application. The increase in the adoption of smartphone devices and the implementation of IoT services in the organization will drive the market in the forecast period. Since the outbreak of COVID-19, the demand for cloud-based solutions has seen significant growth owing to remote working models being adopted by enterprises; however, various industries such as retail, manufacturing, BFSI, and others have seen a significant slump in their revenues in the past years.

Key Highlights

- As customers have moved their workloads to the cloud, there is a growth in the usage of cloud-native architectures, particularly microservices. Microservice-based architectures help improve scalability and velocity, but implementing them can pose challenges. For many Java developers, Spring Boot and Spring Cloud have helped address these challenges, providing a robust platform with well-established patterns for developing and operating microservice applications. In the previous year, to help make it simpler to deploy and manage Spring Cloud applications, together with Pivotal, Microsoft created Azure Spring Cloud.

- Recently, VSHN announced Project Syn, the next generation Open Source managed services framework for DevOps and application operations on any infrastructure based on Kubernetes. Project Syn is a pre-integrated set of tools to provision, update backup, observe, and react or alert production applications on Kubernetes and in the cloud. It supports DevOps through complete self-service and automation with the help of containers, Kubernetes, and GitOps. Project Syn is about to become an Open Source project shortly. It consists of several components that bring the necessary features for running applications in production on Kubernetes, acting as an operations framework.

- During the previous year, AWS launched Amazon Managed Apache Cassandra Service, a scalable, highly available, and managed Apache Cassandra-compatible database service that enables the user to run the Cassandra workloads in the AWS Cloud utilizing the same Cassandra application code, Apache 2.0 licensed drivers, and tools that are used. With Managed Cassandra Service, there is no need to provision, patch, or manage servers and install, maintain, or operate the software. Tables could scale up and down automatically based on request traffic, with virtually unlimited throughput and storage. The user can manage access to the tables using AWS Identity and Access Management (IAM) and keep the applications running smoothly with integrated logging and monitoring.

- Information Technology spending in recent years is likely to fall as organizations trim investments in technology in the wake of the COVID-19 pandemic-led slowdown. However, enterprises and government agencies continue to invest in software and IT services, which is expected to stabilize the market. While short-term projects are getting stopped, the managed application services segment, which fetches significant revenue for service providers, has not been impacted by the outbreak. Recently, XenonStack offered a free 3-month Managed IT Support, Application Management, and Migration to the Cloud as part of their COVID-19 response plan program to anyone directly involved in relief initiatives like Healthcare, NGOs, and government bodies.

Managed Application Services Market Trends

IT and Telecom is Expected to Hold Major Share

- The IT and telecom sector is a significant market for managed application services due to the high rate of various technological adoptions, increased frequency of confirmation of the BYOD policy, and an increased need for high-end security due to the rapidly growing data among organizations. The telecom industry has observed extensive growth during the past few years. Telecommunication companies are constantly pressured to deliver innovative services at lower costs to retain their customers in the competitive market.

- According to the SD-WAN Managed Services recent survey, 64% of the surveyed network and IT managers plan to add an SD-WAN managed service in the upcoming years. This is because the end-users believe it will deliver better security, improved cloud application performance, and flexible management. This demand is encouraging IT and Telcom service providers to purchase hardware, software, and regular administration of their networks from a third party. Many SD-WAN-managed service providers are differentiating themselves with a wide range of security offerings.

- According to Hazlecast Infinity Data report in collaboration with Intel, IT decision-makers identified cloud application performance (40%) as the number one opportunity to unlock profits, with financial services (49%), telecommunications (42%), and e-commerce (40%) ranking it the highest among verticals surveyed. However, security (97%) and performance (90%) were the top challenges when migrating to the cloud.

- In the previous year, Hazelcast announced the availability of Hazelcast Cloud Enterprise on Amazon Web Services (AWS), a low-latency deployment of Hazelcast software as a managed service designed to improve the performance, security, and ease of management of cloud-based applications. Featuring built-in protection and a cloud-agnostic architecture, Hazelcast Cloud Enterprise exceeds the speed, scale, safety, and high availability capabilities of existing commoditized cloud data storage services for large-scale enterprise deployments.

North America is Expected to Hold Major Share

- The North American Managed Application Services market is growing due to the changing IT infrastructure landscape, especially in small and medium enterprises (SMEs), continually focusing on outsourcing cybersecurity solutions. For instance, Kpaul Properties LLC, one of the emerging manufacturers and distributors of IT supplies in the United States, onboarded FUJITSU to replace physical servers with a virtualized environment. This has reduced the company's cost by 15% and delivered 95% uptime. With the speedy acceleration of modern technology and the need for streamlined IT functions, an increasing number of businesses in the region find the best way to keep pace with MSP.

- Besides, Canada is witnessing a high rise in the application of multi-Cloud environments and increased adoption of automation. In the region, Cloud, mobile, and social technologies demand that businesses take a proactive approach toward IT security, thus boosting the demand for deploying robust managed services that would deliver in all security management layers. Unified Communications as a Service and related Contact Center as a Service market represent a business opportunity for managed service providers. This is because emerging players offer innovative cloud-based solutions, which require a minimum investment and are easy to deploy.

- Recently, Rackspace, an American-managed Cloud computing company, announced that it has agreed to acquire Onica, an Amazon Web Services (AWS) Partner Network (APN) Premier Consulting Partner and AWS Managed Service Provider. This acquisition brings Onica's innovative professional services capabilities, including strategic advisory, architecture, engineering, and application development, to the Rackspace portfolio, complementing its existing managed cloud services capabilities. Rackspace's hybrid cloud portfolio enables enterprises to leverage various technical enhancements, from IT security to software development.

- In the previous year, Infosys unveiled the Infosys Live Enterprise Suite in Phoenix, Arizona, a comprehensive set of platforms, solutions, and digital services that helps enterprises to accelerate their digital innovation journey. The user can embrace the best innovations across cloud providers and build a cloud-agnostic application stack through the Infosys Polycloud Platform. The platform provides a backplane that abstracts the public and private clouds, enabling a standard interface and catalog to select, provision, move and manage platform and application services workloads across the enterprise.

Managed Application Services Industry Overview

The competition within the managed application services market is high among the market players without any specific dominating player. The competition results are based on the enterprise's best features of high quality and services at a reasonable price. Some significant players in the market are IBM Corporation, HCL Technologies Limited, WIPRO Limited, Fujitsu Ltd., and others. Some of the recent trends in the market are as follows:

- May 2022 - Microsoft launched a new managed service category known as Microsoft Security Experts. The service provides organizations with assistance from external security experts who can perform threat hunting and managed detection and response tasks. For businesses, the service enables on-site security teams to supplement their capabilities with assistance from off-site Microsoft experts.

- February 2022 - IBM partnered with SAP (NYSE: SAP) to provide technology and consult experts to help clients embrace a hybrid cloud approach and migrate mission-critical workloads from SAP solutions to the cloud in regulated and non-regulated industries. As part of the RISE with an SAP offering, IBM is the first partner to provide cloud infrastructure and technical managed services.

- Moreover, as clients consider hybrid cloud strategies, moving the workloads and applications that are the backbone of their enterprise operations necessitates a highly secure and reliable cloud environment. With the launch of the IBM supplier option for RISE with SAP, clients have the tools to help accelerate the migration of their on-premise SAP software workloads to IBM Cloud, backed by industry-leading security capabilities.

- In addition, IBM is launching a new program called BREAKTHROUGH with IBM for RISE with SAP, which includes a portfolio of solutions and consulting services to help accelerate and amplify the journey to SAP S/4HANA Cloud. The solutions and services, built on a flexible and scalable platform, use intelligent workflows to streamline operations. They offer an engagement model that aids in the planning, execution, and support of holistic business transformation. Clients are also given the option and flexibility to migrate SAP solution workloads to the public cloud with the help of deep industry expertise.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increased demand for end-to-end application hosting

- 4.2.2 The requirement to improve and secure critical business applications

- 4.2.3 Increase in the level of application infrastructure

- 4.3 Market Restraints

- 4.3.1 Security risks associated with application data

- 4.4 Value Chain / Supply Chain Analysis

- 4.5 Porters 5 Force Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 PESTLE Analysis

5 MARKET SEGMENTATION

- 5.1 Organization Size

- 5.1.1 Small & Medium-scale Enterprises

- 5.1.2 Large Enterprises

- 5.2 End-user Verticals

- 5.2.1 BFSI

- 5.2.2 Retail & E-Commerce

- 5.2.3 IT & Telecom

- 5.2.4 Manufacturing

- 5.2.5 Healthcare

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Russia

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia Pacific

- 5.3.3.1 India

- 5.3.3.2 China

- 5.3.3.3 Japan

- 5.3.3.4 Rest of Asia Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.5 Middle East

- 5.3.5.1 United Arab Emirates

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 Rest of Middle East

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Mergers & Acquisitions

- 6.3 Company Profiles

- 6.3.1 Fujitsu Limited

- 6.3.2 IBM Corporation

- 6.3.3 HCL Technologies Limited

- 6.3.4 Wipro Limited

- 6.3.5 VIRTUSTREAM INC.

- 6.3.6 RACKSPACE INC.

- 6.3.7 CenturyLink, Inc.

- 6.3.8 DXC Technology Company

- 6.3.9 BMC Software, INC.

- 6.3.10 Mindtree Limited

- 6.3.11 Unisys Corporation

7 MARKET OPPORTUNITIES AND FUTURE TRENDS