PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1405712

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1405712

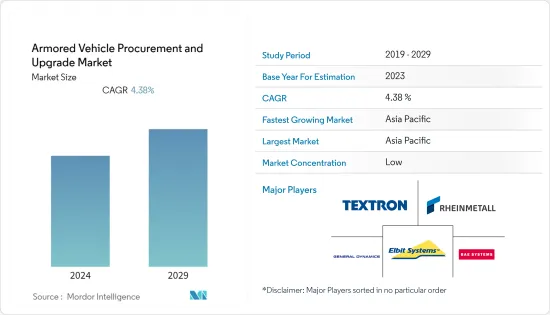

Armored Vehicle Procurement and Upgrade - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029

The Armored Vehicle Procurement and Upgrade Market is valued at USD 6.66 billion in 2024 and is expected to reach USD 8.26 billion by 2029, registering a CAGR of 4.38% during the forecast period.

With the ever-increasing need for national and regional security, countries such as India, the United Kingdom, France, and the United States are anticipated to be the primary centers in the market studied. Growing military expenditure of these countries is expected to help in this regard by giving freedom to the militaries to spend huge amounts for the procurement of these vehicles in order to satisfy the increasing demand.

Countries with vast land-based borders are emerging as lucrative markets for armored vehicles. The procurement of land-based vehicles is increasing, particularly in Asia-Pacific and Europe. It is due to the growing political tensions between the neighboring countries and increasing hostile activities in the regions. In addition, these factors are increasing the need for incorporating the latest technologies into the land vehicles. It, in turn, is a major driver for upgrade and retrofit activities.

The demand for upgrading existing armored vehicles will be triggered by the development of weapon systems, communication, and other new materials related to vehicle protection and armory. It is expected to generate market opportunities in the area of armor upgrades and retrofitting.

Armored Vehicle Procurement & Upgrade Market Trends

The Infantry Fighting Vehicle Segment to Dominate Market Share

The demand for IFVs increased in the recent past from armies worldwide due to the requirement for vehicles with high firepower. IFVs are less expensive and easier to maintain than MBTs. Also, IFVs are designed to include higher mobility than MBTs. In addition, IFCs also provide personnel protection like APCs with greater firing capabilities, and thus, they are used as substitutes for APCs. Driven by their growing popularity, there is an increase in the procurement and upgrades of IFVs in recent times. For instance, the UK Army is in the process of modernizing its armored vehicles with Ajax (Armoured cavalry) and Boxer (mechanized infantry) vehicles. Nasmyth Group Limited won a contract to provide precision machined and fabricated components for the Boxer program. Ajax is a fully digitalized, advanced land vehicle that delivers transformational change in the UK army's future armored fleet. The Ajax vehicle system offers enhanced lethality, mobility, survivability, all-weather intelligence, surveillance, target acquisition, and recognition capabilities. In 2022, Ajax vehicle was tested for noise and vibrations, and the first round of deliveries of vehicles is planned for 2023.

Similarly, in August 2023, the Polish Government announced a partnership between the Polish Armaments Agency (AA) and the Polish Armaments Group (PGZ) to deliver 400 'Polonised' Kia Light Tactical Vehicles (KLTVs). Moreover, the Polish Armaments Group (PGZ) also gave the contract to Huta Stalowa to deliver wheeled infantry fighting vehicles (IFVs) with comprehensive logistics and training packages. Such procurement and upgrade requirements are expected to increase the revenues for the segment in the years to come.

Asia-Pacific is Projected to Dominate the Market During the Forecast Period

In terms of geography, the Asia-Pacific region accounted for the highest market share in 2023. The region is also projected to witness the highest CAGR during the forecast period, driven by the increasing demand from countries like China and India, among others. China's production capacity is advancing in almost every category of ground systems, like armored personnel carriers, assault vehicles, artillery systems and pieces, air defense artillery systems, and main and light battle tanks. China North Industries Corporation (Norinco) is focusing on increasing the production and sales of domestically manufactured armored vehicles for the past few years. These vehicles require an update to extend their lifespan. Hence, the market for retrofit and modernization is expected to witness immense growth in China. In addition, India is also increasing its armored vehicle strength due to its issues with land-border-sharing countries. A significant focus is on the modernization of its aging armored vehicle fleet. For instance, in March 2021, Mahindra Defence Systems (MDS) won a USD 127.4 million contract from the Indian Ministry of Defence (MoD) to deliver 1,300 Armoured Tactical Vehicles (LSV) for the Indian Army. Mahindra's Armoured Tactical Vehicles will be utilized as a medium of carriage for machine guns, automatic grenade launchers, and anti-tank guided missiles.

Similarly, in December 2021, Australia awarded a USD 1 billion contract to Hanwha Defense to deliver 30 self-propelled howitzers and 15 armored ammunition resupply vehicles and military vehicles for the Australian Army. Moreover, in July 2023, the Australian Army awarded a USD 6 billion contract to Hanwha Defense, where it selected Hanwha's "Redback" IFV over Rheinmetall's rival "Lynx" infantry Fighting Vehicle. Such plans are expected to increase the prospects for the market in Asia-Pacific as a whole in the years to come.

Armored Vehicle Procurement & Upgrade Industry Overview

The armored vehicle procurement and upgrade market is fragmented, with many global and local players competing with their manufacturing, MRO, and upgrade capabilities. General Dynamics Corporation, BAE Systems plc, Rheinmetall AG, Textron Inc., and Elbit Systems Ltd. are some of the prominent players in the market. The market saw an increase in the number of local players over the last decade. The aging fleet of armored vehicles in Asia-Pacific, the Middle East, and Africa gave the necessary opportunities for the local players in these regions to develop their capabilities, helping them gain significant shares in the local markets. The countries now can produce their own 3rd and 4th generation MBTs and other armored vehicles locally. In such a competitive environment, the global players are compelled to improve their policies and delivery promises to remain major players outside the United States and European Union, where they enjoy higher revenues. Also, in the coming years, global players may cut down on prices to compete with local manufacturers.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Challenges and Restraints

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Vehicle Type

- 5.1.1 Armored Personnel Carrier (APC)

- 5.1.2 Infantry Fighting Vehicle (IFV)

- 5.1.3 Mine-resistant Ambush Protected (MRAP)

- 5.1.4 Main Battle Tank (MBT)

- 5.1.5 Other Vehicle Types

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.2 Europe

- 5.2.2.1 United Kingdom

- 5.2.2.2 France

- 5.2.2.3 Germany

- 5.2.2.4 Russia

- 5.2.2.5 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 India

- 5.2.3.3 Japan

- 5.2.3.4 South Korea

- 5.2.3.5 Australia

- 5.2.3.6 Rest of Asia-Pacific

- 5.2.4 Latin America

- 5.2.4.1 Brazil

- 5.2.4.2 Mexico

- 5.2.4.3 Rest of Latin America

- 5.2.5 Middle East & Africa

- 5.2.5.1 United Arab Emirates

- 5.2.5.2 Saudi Arabia

- 5.2.5.3 Turkey

- 5.2.5.4 South Africa

- 5.2.5.5 Rest of Middle East and Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 General Dynamics Corporation

- 6.2.2 Rheinmetall AG

- 6.2.3 BAE Systems plc

- 6.2.4 Textron Inc.

- 6.2.5 Elbit Systems Ltd.

- 6.2.6 RUAG International Holding Ltd.

- 6.2.7 KNDS N.V.

- 6.2.8 Oshkosh Corporation

- 6.2.9 THALES

- 6.2.10 The CMI Group, Inc.

- 6.2.11 FNSS Savunma Sistemleri A.S.

- 6.2.12 IVECO S.p.A

- 6.2.13 BMC Otomotiv Sanayi ve Ticaret A.S.

- 6.2.14 Streit Group

7 MARKET OPPORTUNITIES AND FUTURE TRENDS