PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1536883

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1536883

Automotive Gears - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

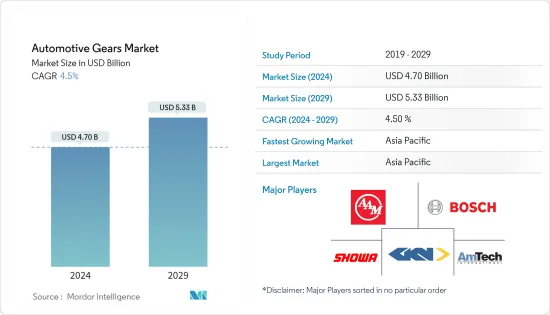

The Automotive Gears Market size is estimated at USD 4.70 billion in 2024, and is expected to reach USD 5.33 billion by 2029, growing at a CAGR of 4.5% during the forecast period (2024-2029).

The automotive gears market was valued at USD 4.67 billion in 2022 and is expected to reach USD 5.38 billion by 2027. The automotive gears market is anticipated to register a CAGR of over 5.5% during the forecast period (2023-2028).

The COVID-19 pandemic disrupted market growth. With lockdowns and travel restrictions, the demand for vehicles had declined. As a result, the growth of automotive parts in the automotive industry also fell in the past two years. This trend was seen in all segments related to the automotive industry.

Over the long term, vehicle production has increased yearly in developed and developing countries. This will lead to growth in the automotive gear market. In the automotive market, a shift toward a more enhanced driving experience in terms of smooth gear shifting & improved acceleration has been increased.

However, various factors are restraining the growth of the gear market, such as the growing demand for electric vehicles due to rising emission regulations. Electric vehicles use minimal gear. The overall number of gears is significantly less due to fewer transmission systems, lesser use of differentials, and near elimination of gearboxes.

Asia-Pacific is likely to lead the automotive gears market, as the region is a significant vehicle producer, followed by Europe and North America. The market growth across these regions will likely be supported by demand for passenger cars and light commercial vehicles and continuous investments by established gear manufacturers in research and development to achieve improved vehicle efficiency and reduced carbon footprint in the coming years.

Automotive Gear Market Trends

Parallel Gear Shaft is Expected to Dominate the Market during Forecast Period

Parallel shaft gear motors, also called parallel shaft gearboxes, feature a design in which the input and output shafts are parallel but offset.

This design allows for higher torque capacity and a more comprehensive range of gear ratios than concentric gearboxes, making them suitable for applications that require higher torque and speed capabilities.

A parallel shaft gear motor refers to the position where the gearbox reducer's output shaft sits. If the motor shaft and the speed reducer output shaft are on parallel planes, it is considered a "parallel shaft." This position, coupled with the inline positioning, enables the gear motor to succeed in limited-space areas. Compact size leads to less weight, less sound, less vibration, and a happy customer experience.

In many engine systems, parallel shafts are used for power transmission between components. For example, in an internal combustion engine, one shaft may be connected to the crankshaft to transmit power from the pistons. In contrast, the other shaft may be connected to the camshaft to control valve timing and operation.

Parallel shafts can be utilized for balancing purposes in engines. By rotating two counter-rotating masses on parallel shafts, the engine can achieve dynamic balance, reducing vibrations and improving the overall smoothness of operation. This is commonly employed in specific engine configurations, such as boxer engines.

Asia-Pacific is Expected to Dominate the Market During the Forecast Period

Asia-Pacific is likely to dominate the automotive gears market, with China being a key contributor to the market's growth. Asia-Pacific is the leading market for automotive gear. With the increasing vehicle production in countries such as India and China and the manufacturers' focus on increasing production capacity, the demand for automotive gear is anticipated to grow significantly. For instance, according to several reports, China is expected to sell 80 million internal combustion engines annually in the coming years as these IC vehicles are still occupying the dominant share.

Additionally, the increasing need for fuel-efficient vehicles and lightweight automotive parts drive the market's growth. In addition, lightweight and highly durable aluminum and composite gears are estimated to gain higher popularity during the forecast period. For instance, NORD launched the SK 920072.1 two-stage helical bevel gear motor (mounted with a NORD motor), a drive solution for a wide range of light-duty conveying, processing, and manufacturing applications. It is identified by its high-strength and lightweight design.

The factors above and developments across various countries in Asia-Pacific are expected to enhance the market's growth during the forecast period.

Automotive Gears Industry Overview

Some of the major manufacturers in the automotive gear market include American Axle & Manufacturing Holdings Inc., AmTech International, Bharat Gears Ltd, GKN PLC, Robert Bosch GmbH, Gleason Plastic Gears, Showa Corporation, and Universal Auto Gears LLP.

- In June 2021, JATCO developed a new continuously variable transmission, "CVT-X," for medium and large FWD vehicles with improved environmental performance and drivability. It is said to have achieved more than 90% transmission efficiency, which was considered difficult for a CVT.

- ZF announced investing USD 200 million in commercial vehicle transmission manufacturing in North America. In 2023, ZF planned to produce the ZF Powerline 8-speed automatic transmission at the company's state-of-the-art manufacturing facility in Gray Court, SC. In July 2021, ZF secured a nearly USD 6 billion axle contract for the Marysville, Michigan, facility to deliver beam axles and axle drives for pick-up trucks until 2027.

- In March 2019, Dana Incorporated announced that it completed the acquisition of the Drive Systems segment of the Oerlikon Group. This acquisition has expanded Dana's technology portfolio, especially in high-precision helical gears for the light- and commercial-vehicle markets.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.2 Market Restraints

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD billion)

- 5.1 By Position

- 5.1.1 Skew Shaft Gears

- 5.1.1.1 Hypoid Gears

- 5.1.1.2 Worm Gears

- 5.1.2 Intersecting Shaft Gears

- 5.1.2.1 Straight Bevel Gears

- 5.1.2.2 Spiral Bevel Gears

- 5.1.3 Parallel Shaft Gears

- 5.1.3.1 Spur Gears

- 5.1.3.2 Rack and Pinion Gears

- 5.1.3.3 Herringbone Gears

- 5.1.3.4 Helical Gears

- 5.1.1 Skew Shaft Gears

- 5.2 By Material

- 5.2.1 Ferrous Metals

- 5.2.2 Non-ferrous Metals

- 5.2.3 Other Materials (Composites and Plastics)

- 5.3 By Application

- 5.3.1 Steering Systems

- 5.3.2 Differential Systems

- 5.3.3 Transmission Systems

- 5.3.3.1 Manual

- 5.3.3.2 Automatic

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 Latin America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Mexico

- 5.4.4.4 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 American Axle & Manufacturing Holdings Inc.

- 6.2.2 AmTech International

- 6.2.3 Bharat Gears Ltd

- 6.2.4 Cone Drive

- 6.2.5 Dynamatic Technologies Limited

- 6.2.6 Franz Morat Group

- 6.2.7 GKN PLC

- 6.2.8 Gleason Plastic Gears

- 6.2.9 IMS Gear SE & Co. KGaA

- 6.2.10 Robert Bosch GmbH

- 6.2.11 RSB Global

- 6.2.12 Showa Corporation

- 6.2.13 Taiwan United Gear Co. Ltd

- 6.2.14 Universal Auto Gears LLP

- 6.2.15 ZF Friedrichshafen AG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS