PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1435861

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1435861

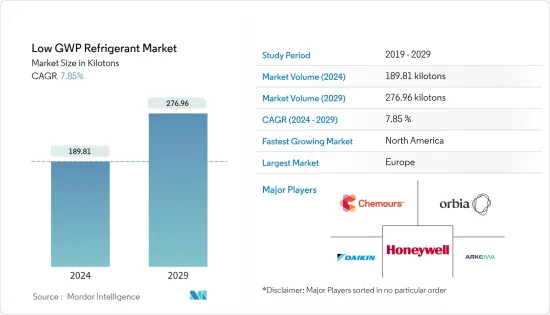

Low GWP Refrigerant - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

The Low GWP Refrigerant Market size is estimated at 189.81 kilotons in 2024, and is expected to reach 276.96 kilotons by 2029, growing at a CAGR of 7.85% during the forecast period (2024-2029).

The low GWP refrigerant market was negatively impacted by the COVID-19 pandemic. However, the market recovered significantly in 2021, owing to rising applications in pharmaceuticals, residential, commercial, and others.

Key Highlights

- The low environmental impact and stringent regulations are likely to be the main driver of the low GWP refrigerant market's growth over the medium term.

- However, the higher flammability and other toxicity characteristics are expected to limit the growth of the low GWP refrigerant market.

- Nevertheless, developments for promoting low GWP refrigerants are likely to create lucrative growth opportunities for the global market soon.

- Europe represents the largest market,with the largest consumption coming from countries such as Germany,United Kingdom, etc.

Low GWP Refrigerant Market Trends

Commercial Refrigeration to Dominate the Market

- Low global warming potential (GWP) refrigerant solutions have been in greater demand for air conditioning and refrigeration applications. These low-GWP refrigerants increase energy consumption, introduces safety risks, and require significant equipment modifications.

- Moreover, these are primarily used to reduce service equipment energy consumption and carbon emissions by 50% compared to HFCs and CFCs.

- Low global warming potential (GWP) refrigerant solutions have been in greater demand for air conditioning and refrigeration applications. These low-GWP refrigerants increase energy consumption, introduces safety risks, and require significant equipment modifications.

- The usage of low GWP refrigerants is increasing, especially in the commercial refrigeration segment that includes varied applications, including food safety in dairy, meat, fisheries, and other food industries that rely on efficient cold chain networks (commercial freezers and refrigerators), cold chain preservation in the pharmaceutical industry, commercial air conditioners.

- Based on data published by the Air Conditioning and Refrigeration Association of Japan in June 2022, the worldwide demand for commercial air conditioners experienced a significant increase in 2021, reaching 14.88 million units. The North America region took the lead with a total of 7.37 million units in the same year, surpassing previous years figures.

- According to The Haier Smart Home, Asia's air-conditioners retail unit volume has reached 132.3 million units in 2022 and is estimated to reach 147.4 million units by 2024.

- Furthermore, according to OEA (India), the wholesale price index of air conditioners reached 119.4 in 2022.

- With the increasing demand for frozen food products and a highly competitive market with low margins, most food processors, distributors, and retailers are shifting from manually operated obsolete facilities to the high bay deep-freeze warehouses, where commercial refrigeration are widely employed.

- Moreover, the expansion of retail food chains by the multinational companies and the growth in international trade (due to trade liberalization) have led to an increase in the demand for the cold chain processes. This, in turn, is augmenting the demand for commercial refrigeration across the world.

Germany to Dominate the Europe Market

- The German economy is the largest in Europe and the fifth-largest in the world. Germany has a strong manufacturing sector, particularly in the areas of machinery and automotive. This has helped the country maintain a competitive edge in international trade and attract foreign investment.

- Based on the data published by the Association of Air Conditioning and Refrigeration Industry in Japan in June 2022, the sales of commercial air conditioning units in Germany experienced a significant increase in 2021, with the demand reaching 50 thousand units. This surge in demand marked a notable rise compared to previous years.

- The German food and beverage industry is the largest industry sector. Food processing is one of the major activities in the domestic food and beverage industry, which creates a significant need for refrigeration. The country's food and beverage export business exceeds more than EUR 72.6 billion (~USD 79.6 billion).

- Some of the major foods processed in the country include meat and sausage products, dairy products, baked goods, and confectionery. Most of these products need cold storage in order to increase their shelf life, further creating a demand for refrigeration.

- According to The Federal Ministry of Food and Agriculture( BMEL), Germany's per capita consumption of meat has reached 77.5 kilograms in 2022.

- Germany is one of the world's largest consumers of soft drinks with more than 120 liters of per-capita consumption. Caffeine-oriented drinks are the most dynamic in the present German market. This has given a boost to the sales of companies, such as Sprite, Fanta, Delta, Mezzo Mix, and Coca-Cola. The need for cold storage of these cold drinks has created a significant demand for refrigeration.

- Furthermore, with the use of better cryogenic equipment and the increased demand for frozen foods, the low GWP refrigeration market is poised to witness an increasing growth rate in the coming years in the country.

- However, there is significant demand from the food processing aftermarket, which is expected to increase the demand for refrigerants from the automotive industry in the coming years.

Low GWP Refrigerant Industry Overview

The low GWP refrigerants market is partially consolidated in nature, with players accounting for a marginal share of the market studied. A few major companies in the market (not in particular order) include Honeywell International Inc., The Chemours Company, Orbia, Arkema, and DAIKIN INDUSTRIES, Ltd., among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Low Environmental Impact

- 4.1.2 Stringent Regulations

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Higher Flammability and Other Toxicity Characteristics

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Type

- 5.1.1 Inorganics

- 5.1.2 Hydrocarbons

- 5.1.3 Fluorocarbons and Fluoro-olefins (HFCs and HFOs)

- 5.2 Application

- 5.2.1 Commercial Refrigeration

- 5.2.2 Industrial Refrigeration

- 5.2.3 Domestic Refrigeration

- 5.2.4 Other Applications

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 A-Gas

- 6.4.2 Arkema

- 6.4.3 DAIKIN INDUSTRIES, LTD.

- 6.4.4 Danfoss

- 6.4.5 engas Australasia

- 6.4.6 GTS SPA

- 6.4.7 HARP International

- 6.4.8 Honeywell International Inc

- 6.4.9 Linde

- 6.4.10 Messer Group

- 6.4.11 Orbia

- 6.4.12 Tazzetti S.p.A

- 6.4.13 The Chemours Company

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Developments for Promoting Low GWP Refrigerants

- 7.2 Other Opportunities