Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1690091

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1690091

North America Small Satellite - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 160 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

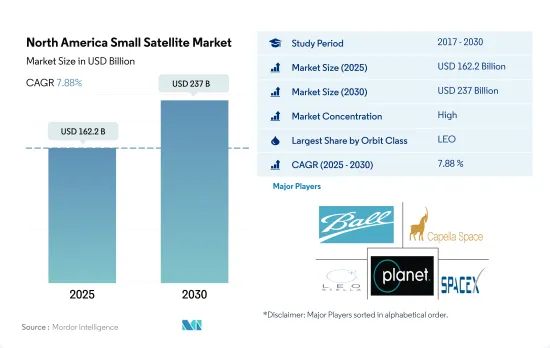

The North America Small Satellite Market size is estimated at 162.2 billion USD in 2025, and is expected to reach 237 billion USD by 2030, growing at a CAGR of 7.88% during the forecast period (2025-2030).

LEO satellites are driving the demand for small satellites

- During launch, a satellite or spacecraft is usually placed into one of many special orbits around the Earth, or it can be launched into an interplanetary journey. There are three types of Earth orbits, namely, geostationary orbit (GEO), medium Earth orbit, and low Earth orbit. Many weather and communication satellites tend to have high Earth orbits farthest from the surface. Satellites in medium Earth orbit include navigational and specialized satellites designed to monitor a specific area. Most science satellites, including NASA's Earth Observation System, are in low Earth orbit.

- The small satellite market is experiencing strong growth, driven by the increasing demand for LEO satellites, which are used for communication, navigation, Earth observation, military reconnaissance, and scientific missions. Between 2017 and 2022, around 2,900 small LEO satellites were manufactured and launched in North America alone, primarily for communication purposes. This has led companies such as SpaceX, OneWeb, and Amazon to plan the launch of thousands of satellites into LEO. With the rising demand for low Earth orbit from various sectors like Earth observation, navigation, meteorology, and military communications, the region has witnessed an increase in the number of LEO satellite launches.

- The military's use of MEO and GEO satellites has grown in recent years due to their advantages, including increased signal strength, improved communications and data transfer capabilities, and greater coverage area. For instance, Raytheon Technologies' and Boeing's Millennium Space Systems are developing the first prototype Missile Track Custody (MTC) MEO OPIR payloads to detect and track hypersonic missiles for the US Space Force.

North America Small Satellite Market Trends

A trend of using better fuel and operational efficiency has been witnessed

- Satellites are getting smaller nowadays. A small satellite can do almost everything as a conventional satellite at a fraction of the cost, thus making the building, launching, and operation of the small satellite constellations increasingly viable. The reliance on small satellites has also been growing exponentially. Small satellites typically have shorter development cycles, smaller development teams, and cost much lesser for launch. Revolutionary technological advancements facilitated the miniaturization of electronics, which pushed the invention of smart materials, reducing the satellite bus size and mass over time for manufacturers.

- Satellites are classified according to mass. The satellites with a mass of less than 500 kg are considered small satellites, and around 2,900+ small satellites were launched in the region during the historical period. There is a growing trend toward small satellites in the region due to their shorter development time, which can reduce overall mission costs. They have significantly reduced the time required to obtain scientific and technological results. Small spacecraft missions tend to be flexible and more responsive to new technological opportunities or needs. The small satellite industry in the United States is supported by the presence of a robust framework for designing and manufacturing small satellites tailored to serve specific application profiles. The number of small satellite operators in North America is expected to surge during 2023-2029 due to the growing demand in the commercial and military space sectors.

The increasing space expenditures of different space agencies are expected to impact the North American small satellite market positively

- In North America, government expenditure for space programs hit a record of approximately USD 103 billion in 2021. The region is the epicenter of space innovation and research, with the presence of the world's biggest space agency, NASA. In 2022, the US government spent nearly USD 62 billion on its space programs, making it the highest spender on space in the world.

- The United States is one of the leading countries globally in terms of satellite development and launches. Owing to the immense potential in several aspects of commercial and defense applications, the use of satellites has gained substantial acceptance in the country. The country has many satellites orbiting in space to serve its commercial and defense needs. In December 2022, Planet Labs announced that it had manufactured 36 SuperDove satellites, scheduled for launch using SpaceX's Falcon-9 rocket. Each SuperDove satellite weighs approximately 6 kg, and the data collected by these satellites are expected to provide organizations in agriculture, government, civilian agencies, and other industries to make informed decisions.

- In November 2022, NASA announced that it is planning to launch four CubeSats under the TROPICS mission. These satellites weigh approximately 5.3 kg and are developed to provide rapidly updating observations of storm intensity, as well as the horizontal and vertical structures of temperature and humidity within the storms and in their surrounding environment. The data collected is expected to help scientists better understand the processes that affect these high-impact storms, ultimately leading to improved modeling and prediction.

North America Small Satellite Industry Overview

The North America Small Satellite Market is fairly consolidated, with the top five companies occupying 99.57%. The major players in this market are Ball Corporation, Capella Space Corp., LeoStella, Planet Labs Inc. and Space Exploration Technologies Corp (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 69868

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Satellite Mass

- 4.2 Spending On Space Programs

- 4.3 Regulatory Framework

- 4.3.1 Canada

- 4.3.2 United States

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Application

- 5.1.1 Communication

- 5.1.2 Earth Observation

- 5.1.3 Navigation

- 5.1.4 Space Observation

- 5.1.5 Others

- 5.2 Orbit Class

- 5.2.1 GEO

- 5.2.2 LEO

- 5.2.3 MEO

- 5.3 End User

- 5.3.1 Commercial

- 5.3.2 Military & Government

- 5.3.3 Other

- 5.4 Propulsion Tech

- 5.4.1 Electric

- 5.4.2 Gas based

- 5.4.3 Liquid Fuel

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Ball Corporation

- 6.4.2 Capella Space Corp.

- 6.4.3 LeoStella

- 6.4.4 National Aeronautics and Space Administration (NASA)

- 6.4.5 Planet Labs Inc.

- 6.4.6 Space Exploration Technologies Corp

- 6.4.7 SpaceQuest Ltd

- 6.4.8 Spire Global, Inc.

- 6.4.9 Swarm Technologies, Inc.

7 KEY STRATEGIC QUESTIONS FOR SATELLITE CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.