PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1643186

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1643186

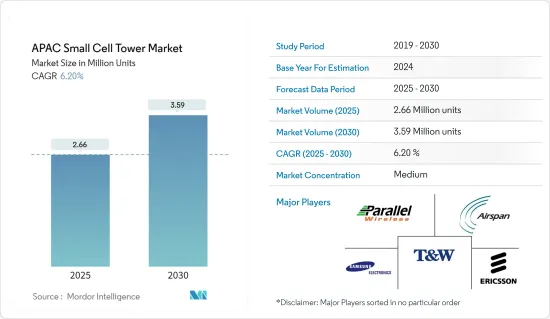

APAC Small Cell Tower - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The APAC Small Cell Tower Market size is estimated at 2.66 million units in 2025, and is expected to reach 3.59 million units by 2030, at a CAGR of 6.2% during the forecast period (2025-2030).

Small cells are low-power cellular radio access nodes ranging from a few hundred meters to several kilometers. These base stations use little energy, are inexpensive, and may deliver high data rates by being placed close together to maximize spatial spectrum efficiency.

Key Highlights

- Most of the 5G networks will likely be composed of small cells. Small cells are vital to the functionality of 5G networks because they provide the increased data capacity that 5G demands. They also help providers reduce costs by eliminating expensive rooftop systems and installation costs, and they are expected to help improve the performance and battery life of mobile handsets.

- In addition to the evolution of network technology and connectivity devices, the market is also driven due to the growth of demand for mobile devices worldwide. Such demand has been driving the shift in how IT services are delivered and has been providing the players in the market with significant opportunities for enhancing their presence across the Asia-Pacific region.

- Moreover, Small cells are essential today for the increasing number of linked devices and Internet of Things (IoT) applications. Installing microcell towers in the low-frequency spectrum is another area of focus for 5G telecom providers as they work to increase bandwidth options for their consumers.

- While small cells can ensure improved network coverage at a low cost, the deployment has brought in new challenges, such as the backhaul development of small cell networks.

- The COVID-19 pandemic has increased demand for wireless internet as people were restricted at home all day (due to lockdowns in many countries) and forced to work from home, connect remotely with their peers, and use the internet services for both work and entertainment. This has led to a surge in online traffic, which acted as a key factor driving the growth of small cell networks, which are easy to install and cost-effective.

APAC Small Cell Tower Market Trends

Indoor applications are Expected to Have a Major Market Share.

- Indoor scenarios are inherently more complex in comparison to outdoor ones. Indoor scenarios typically include large and medium public locations, small and medium enterprises, and homes, which vary in-service requirements and need diverse solutions to cater to these requirements.

- Small cells are essential to networks because they provide coverage and capacity outside of the macro network in a quick, affordable, and high-performing manner that allows for interior use. For instance, Ericsson's indoor small cells meet the requirement for enhanced indoor voice and data coverage and capacity.

- Small indoor cells provide coverage expansion in areas with heavy traffic and limited capacity, such as universities, well-known tourist destinations, stadiums, music halls, convention centers, hospitality settings, and various large meeting spaces. This makes it possible for the general public to utilize their various devices effectively wherever they are.

- To meet the rising demand for private 5G enterprise connectivity for campus, industrial, and venue applications, for instance, in March 2022, STL, one of the leading digital network integrators in the market, announced the launch of the first end-to-end 5G Enterprise solution is in partnership with ASOCS and VMWare. These future-ready 5G networks, which can handle dense environments required for seamless interior coverage, will be made possible by open standards-based designs.

China to Witness the Growth

- The rapid development of 5G technology and mobile connectivity in such countries collectively contributes to the growth of the market in the region.

- China is at the forefront of 5G adoption in the Asia Pacific. China reportedly took the lead in 5G development in May 2022, with 819,000 5G base stations, or more than 70% of the total number installed globally, according to Xinhua. By the end of 2023, China projects that the number of 5G users will be close to 560 USD million, or 35% of the total number of consumers worldwide. Also, every 10,000 Chinese would have access to more than 18 5G base stations, according to the official release.

- In addition, various global companies are stepping into the country to drive 5G experiences for consumers by creating a dense environment for indoor coverage with the required speed, capacity, and low latency.

- A small cell network enables retailers a higher rapid mobile connectivity, which can scale and unlock new experiences and may offer customers and retailers new ways to shop and run their businesses. Furthermore, the growing adoption of IoT devices in the sector further expands the scope.

- Moreover, With the nationwide rollout of the 5G network, small-cell networks will see a significant increase in adoption over the coming years. In recent years, small cell networks have established themselves as a viable option for all retail businesses seeking improved mobile coverage and capacity indoors and outdoors.

- According to the GSMA 2022 Study on the mobile economy in China, it is predicted that in 2025, the number of 4G connections will decline to 840 USD million with a 48% adoption rate, while the number of 5G connections is predicted to increase to 892 USD million with a 52% adoption rate.

APAC Small Cell Tower Industry Overview

The competition in the Asia-Pacific Small Cell Tower Market is semi-consolidated. To launch new items, organizations in the market are implementing mergers and acquisitions, strategic collaborations, and product development. The major players are Samsung Electronics Co., Ltd., Parallel Wireless Inc., and Airspan Networks Inc.

- February 2023 - Airspan Networks Inc has announced to expand of its 5G Innovation Lab initiative in Tokyo to accommodate accelerating network adoption and scaling in the Asia-Pacific region. In contrast, Airspan Japan's Tokyo office will spearhead the effort to meet the growing demand for critical interoperability testing and integration simplicity in public and private networks as technology continue to reach new 5G use cases.

- February 2023 - Telefonaktiebolaget LM Ericsson has announced the addition of three new low-cost, quick-to-deploy solutions such as a radio unit called IRU 8850, Ericsson Indoor Fusion Unit, and a new software feature for indoor networks 5G Precise Positioning to its indoor mobile connectivity lineup to bring 5G capabilities and coverage to any workplace setting, regardless of the size or complexity of the facility. Adding additional solutions to the Ericsson Radio Dot System range increases the flexibility of this market-leading offering.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Intensity of Competitive Rivalry

- 4.2.5 Threat of Substitutes

- 4.3 Industry Value Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rapid Increase in Mobile Data Traffic in the Region

- 5.1.2 Growing Emphasis on Operational Efficiency and Reduction of Capital Expenditure through Replacement of Older Networks with Small Cell Towers

- 5.1.3 Steady Growth in Installations by Market Incumbents in Mature Markets such as China and South Korea

- 5.2 Market Challenges

- 5.2.1 Concerns with State Regulations and Operational Challenges Related to Deployment in 5G Networks

- 5.3 Industry Standards & Regulations

- 5.4 Impact of COVID-19 on the Small Cell Deployments and Connectivity

- 5.5 Major Implications and Technical Considerations Related to Installation of Small Cell Towers

- 5.6 Current Ownership Models and Emergence of Small Cell Leasing/Sharing Mechanism

- 5.7 Current Breakdown of the Connectivity Technology in Asia Pacific (3G, 4G & 5G)

6 ANALYSIS OF 5G ROADMAP IN ASIA PACIFIC (CHINA, SOUTH KOREA, SINGAPORE, JAPAN)

7 ASIA PACIFIC SMALL CELL NETWORK SEGMENTATION BY TYPE

- 7.1 By Application

- 7.1.1 Outdoor

- 7.1.2 Indoor

- 7.2 By Country

- 7.2.1 China

- 7.2.2 South Korea

- 7.2.3 Japan

- 7.2.4 India

- 7.2.5 Philippines

- 7.2.6 Rest of Asia Pacific

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 Parallel Wireless Inc.

- 8.1.2 Airspan Networks Inc.

- 8.1.3 T&W Electronics Co Ltd

- 8.1.4 Samsung Electronics Co., Ltd.

- 8.1.5 Telefonaktiebolaget LM Ericsson

- 8.1.6 Huawei Technologies Co., Ltd.

- 8.1.7 ZTE Corporation

- 8.1.8 Baicells Technologies Co., Ltd.

- 8.1.9 NEC Corporation

- 8.1.10 Nokia Corporation

9 INVESTMENT ANALYSIS AND MARKET OUTLOOK