PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1437617

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1437617

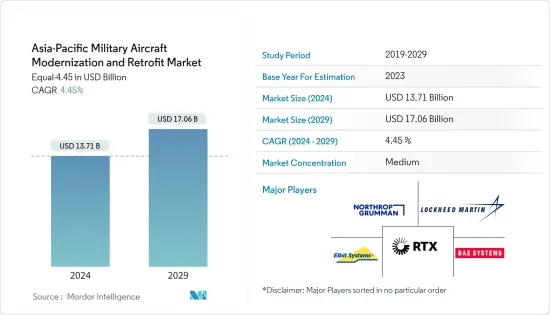

Asia-Pacific Military Aircraft Modernization And Retrofit - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

The Asia-Pacific Military Aircraft Modernization And Retrofit Market size is estimated at USD 13.71 billion in 2024, and is expected to reach USD 17.06 billion by 2029, growing at a CAGR of 4.45% during the forecast period (2024-2029).

The growing need for interoperability with allies, evolving mission requirements, and the obsolescence of older aircraft are creating the demand for military aircraft modernization and retrofit market in the region. Concerns over regional security challenges have prompted nations to strengthen their defense capabilities, leading to a surge in demand for advanced military aircraft.

The retrofit market plays a crucial role as countries look to extend the operational life of existing aircraft while integrating new technologies. Upgrading communication systems, sensors, and weapon systems are common retrofit objectives, ensuring that older platforms remain relevant in the face of evolving threats. The regional drive to develop indigenous military aircraft has driven the administration to draft favorable policies for the market players to promote an R&D-intensive environment, thereby acting as a growth driver for the market studied.

Asia-Pacific Military Aircraft Modernization And Retrofit Market Trends

Fixed-wing Aircraft Segment Holds Highest Shares in the Market

The fixed-wing aircraft segment currently dominates the market studied and is expected to continue its dominance during the forecast period. The increasing military expenditure and current ongoing political tensions in the region are propelling the growth of the segment in the region. In 2022, China and India were the second and fourth largest defense spenders in the world, with defense budgets of USD 292 billion and USD 81.4 billion, respectively. The region is home to several flashpoints, such as the South China Sea, the East China Sea, the Taiwan Strait, the Korean Peninsula, and the India-China border, where tensions have escalated in recent years. These disputes have prompted the countries involved to strengthen their air power and deterrence by acquiring or developing new combat aircraft, such as stealth fighters, bombers, and drones.

For instance, in November 2023, the Indian MoD contracted Hindustan Aeronautics Limited to deliver 97 Tejas Light Combat Aircraft (Mark 1A) for the Indian Air Force (IAF). The Tejas Mk-1A Light Combat Aircraft is an indigenously designed and manufactured fourth-generation fighter equipped with AESA Radar, EW suite consisting of radar warning and self-protection jamming, Digital Map Generator (DMG), Smart Multi-function Displays (SMFD), Combined Interrogator and Transponder (CIT), advanced radio altimeter, and other advances features. Similarly, in December 2023, South Korea contracted Embraer for its Large Transport Aircraft II program. Under the contract, Embraer will deliver C-390 transport aircraft to the country to carry out various missions. Such developments are envisioned to support the growth of the segment during the forecast period.

China Will Dominate the Market During the Forecast Period

China has the highest market share in the Asia-Pacific military aircraft modernization and retrofit market. The growing military spending of the country, fueled by geopolitical tensions and border disputes between the country and its neighboring countries, is driving investments into the procurement of advanced air defense systems. The country is the highest defense spender in the Asia-Pacific region, with military spending of USD 292 billion in 2022, a growth of 2% compared to the military spending in 2021. China's current military spending priorities follow the guiding principles set out in the 14th Five-Year Plan (2021-2025). With this mass defense spending, the country has invested in various military aircraft modernization and retrofit programs.

For instance, in October 2023, the US Pentagon announced that the People's Liberation Army Air Force was upgrading the Chengdu J-20 Mighty Dragon to compete with Lockheed Martin's F-22 multi-role aircraft. China is also rapidly modernizing its transport aircraft fleet to support longer-range military operations. For instance, in August 2022, China commissioned the air refueller variant of the Y-20 Kunpeng transport aircraft into its military. The aircraft was manufactured by Xi'an Aircraft Company (XAC), a subsidiary of the state-owned Aviation Industry Corporation of China (AVIC). The Y-20's entry into service is expected to fill a significant gap in the PLAAF's airlift capability. Overall, such advancements in technology and growing in-house capabilities are anticipated to support the growth of the market studied during the forecast period.

Asia-Pacific Military Aircraft Modernization And Retrofit Industry Overview

The Asia-Pacific military aircraft modernization and retrofit market is semi-consolidated, and it is dominated by players such as Lockheed Martin Corporation, RTX Corporation, Elbit Systems Ltd, Northrop Grumman Corporation, and BAE Systems PLC. These market players focus on designing, engineering, and manufacturing aerostructures, subassemblies, and systems. Several companies have formed long-term partnerships with the air forces to upgrade and enhance military aircraft capabilities as well as for the development of future aircraft modernization programs for the defense ministry.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.2 Market Restraints

- 4.3 Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Aircraft Type

- 5.1.1 Fixed-wing

- 5.1.2 Rotary-wing

- 5.2 Geography

- 5.2.1 China

- 5.2.2 India

- 5.2.3 Japan

- 5.2.4 South Korea

- 5.2.5 Australia

- 5.2.6 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 RTX Corporation

- 6.2.2 L3Harris Technologies Inc.

- 6.2.3 BAE Systems PLC

- 6.2.4 Lockheed Martin Corporation

- 6.2.5 Elbit Systems Ltd

- 6.2.6 Honeywell International Inc.

- 6.2.7 Northrop Grumman Corporation

- 6.2.8 Safran

- 6.2.9 General Dynamics Corporation

- 6.2.10 Leonardo SpA

- 6.2.11 THALES

7 MARKET OPPORTUNITIES AND FUTURE TRENDS