PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1690745

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1690745

5G Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

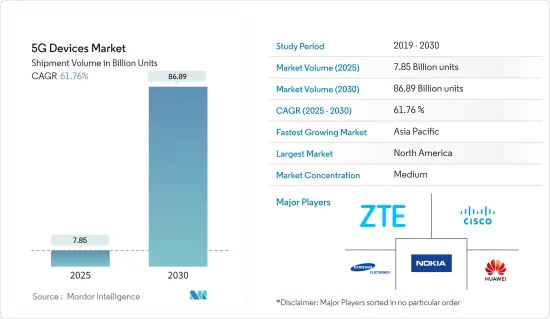

The 5G Devices Market size in terms of shipment volume is expected to grow from 7.85 billion units in 2025 to 86.89 billion units by 2030, at a CAGR of 61.76% during the forecast period (2025-2030).

5G technology will offer ultra-high-speed network coverage and enable numerous new applications with the help of IoT. Also, the COVID-19 pandemic has delayed the widespread deployment of 5G.

Key Highlights

- According to the last year's Ericsson ConsumerLab report, Online interviews were conducted with 49,100 customers in 37 markets between April and July last year. The respondents chosen for the interview represent the surveyed markets' online population of 1.7 billion customers and 430 million 5G users, who range in age from 15 to 69. According to studies, the next wave of 5G is already in motion, with mainstream customers starting to accept the technology in early adopter markets.

- The growing adoption of connectivity, digital applications, and wearable technology is expected to drive growth for players in the 5G devices market. Moreover, upgrading existing supporting infrastructure, including modems, towers, and other supporting infrastructure, will present significant opportunities for new players. The 5G devices market's growth is expected to drive significant opportunities as the adoption of 5G technology has received positive signals in several local markets worldwide.

- Major chip makers also focus on 5G device component development to boost device penetration in the market. This includes chipset vendors competing in volume-driven markets as they introduce more models for mass deployments. In May last year, MediaTek launched Dimensity 1050 mmWave SoC, and related models, to highlight 5G connectivity in devices.

- Also, emerging applications, business models, and falling device costs have driven IoT adoption, increasing the number of connected devices and endpoints globally. 5G offers massive machine-type communication (mMTC), poised to support tens of billions of network-enabled devices to be wirelessly connected. Modern communication systems already serve several MTC applications. However, the characteristic properties of mMTC, i.e., the massive number of devices and the tiny payload sizes, require novel concepts and approaches. 5G allows a density of approximately one million devices per square kilometer.

- However, the global operation and installation of the supportive infrastructure continue to be a significant hurdle in many areas. For instance, in September last year, the international standardization body, 3GPP, updated the next release of the 5G specification, Release 17, for the second half of the previous year. The release was frozen in March last year due to the pandemic and other reasons. Such delays create subsequent delays in companies' supply chains and other operational activities.

- The COVID-19 pandemic's immediate effects have been felt in every industry, causing widespread layoffs, record unemployment, and severely curtailing consumer spending. The spread of COVID-19 resulted in a significant supply chain disruption impeding the 5G buildout process in the short & medium term. The critical 5G hardware delays and general effects of the economic slowdown thus apply.

5G Devices Market Trends

Smartphone Segment is Expected to Witness the Highest Growth

- According to the Ericsson Mobility Report 2021, around 650 new 5G smartphones have been launched globally, accounting for 50% of all the 5G from all form factors. The handheld wireless form factor and convenience of 5G access offered by smartphones are nearly unmatched. As several parts of the world have already begun rolling out 5G, some untouched regions are preparing to receive 5G-enabled smartphone launches to leverage the upcoming 5G launch.

- The increasing technological advancements and growing demand for ultra-high bandwidth, ultra-low latency, and massive connectivity are expected to offer growth opportunities to the market. Moreover, the rising demand for high-speed data connectivity for integrated IoT (Internet of Things) applications, such as energy management and smart home products, is anticipated to propel the adoption of 5G smartphones over the forecast period.

- Several smartphone manufacturers adapt and plan strategic launches according to the local market responses to compete in the highly competitive landscapes. In August last year, Samsung shared plans to launch more smartphones in the Indian market after recording sales of INR 600 crore in less than 12 hours for its new generation 5G-enabled foldable devices. The company would launch the devices ahead of the 5G roll-out in India in the previous year.

- Further, the market players focus on providing customers with a high-end 5G smartphone experience. For instance, in May last year, Qualcomm launched Snapdragon 8 Gen 1 SoC, with clock speeds up to 3.2 GHz for major smartphone implementation. The processor features the fourth-generation Snapdragon X65 5G Modem-RF System, bringing 5G speeds of up to 10 Gbps.

- Such developments attract buyers to upgrade their non-5G smartphones to get the latest and fastest, all-around experience in their smartphone, driving the 5G smartphone market.

North America Expected to Hold a Significant Share

- Service providers in the region have already launched commercial 5G services focused on mobile broadband. The introduction of 5G devices that support all three spectrum bands will enable early adoption of the technology in the region. As of now, 5G services are integrated with 4G services or with hand-off from 5G to 4G when a customer moves from an area where 5G service is available to one where it is not.

- According to the Ericson Mobility Report 2021, around 64 million 5G subscriptions were added in 2021 as migration from 4G to 5G subscriptions picked up significantly. The number of 5G subscriptions is expected to reach 250 million at the end of the current year and 400 million by 2027, accounting for 90 percent of mobile subscriptions.

- Similarly, the report also mentioned North America registering the strongest increase in the number of fixed wireless access (FWA), with about 60% of all service providers surveyed offering FWA. Such regional launches boost the infrastructural support for the 5G roll-out, reaching maximum areas in North America for new users.

- Multiple product launches have enabled 5G connectivity across the region recently. In September last year, Nokia announced extending its Industrial portfolio of user equipment to facilitate private wireless network connectivity in North America. Its new Nokia 5G Industrial fieldrouter and dongle, radio access spectrum capabilities, and Nokia Connectivity Operations Dashboard would provide more options for deploying and managing secure, reliable private 4G/LTE and 5G wireless. The Nokia 5G fieldrouter and 5G dongle could be deployed in the US and Canada Citizen Broadband Radio Service (CBRS) 3.5 GHz spectrum.

5G Devices Industry Overview

The 5G devices market is moderately competitive and consists of many global and regional players. These players account for a considerable market share and focus on expanding their customer base. The vendors focus on the research and development investment in introducing new solutions, strategic partnerships, and other organic & inorganic growth strategies to earn a competitive edge over their counterparts.

- September 2022 - HMD Global launched the new Nokia X30 5G smartphone and a few more Nokia products at IFA 2022 in Berlin, Germany, featuring around eleven 5G bands.

- August 2022 - Bharti Airtel (Airtel) announced signing 5G network agreements with Ericsson, Nokia, and Samsung to commence 5G deployment in August 2022. The partnership with Samsung to supply 5G equipment and solutions would begin in 2022, along with the older partners, Nokia and Ericsson. The 5G partnerships would follow closely on the edge of spectrum auctions conducted by the Department of Telecom in India, where Airtel bid for and acquired 19867.8 MHZ spectrum in 900 MHz, 1800 MHz, 2100 MHz, 3300 MHz, and 26 GHz frequencies.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Market Definition and Scope

- 1.2 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Stakeholder Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Impact of COVID-19 on the 5G Landscape

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Sustained Increase in Number of Devices and Endpoints Worldwide

- 5.1.2 Technological Innovations at a Component and Device Level to Aid Adoption

- 5.1.3 Increasing use of Smart Phones and rising Technological advancement in the smart phones is expected to drive market.

- 5.2 Market Restraints

- 5.2.1 Regulatory and Standardization Delays

- 5.2.2 Design and Operational Challenges

- 5.3 Market Opportunities

- 5.3.1 Anticipated Rise in Demand from the Industrial Sector

- 5.3.2 Ongoing Efforts toward Introduction of 5G in Emerging Countries

- 5.4 5G Timeline and proliferation 5G enabled devices

- 5.5 5G and Beyond - The Path Ahead

- 5.6 Key Industry Regulations and Policies

6 TECHNOLOGY SNAPSHOT

7 5G ADOPTION MARKET LANDSCAPE

- 7.1 Number of Operators Worldwide - Breakdown by Trials and Commercial Launches (Q2'18 - Q1'20)

- 7.2 Country-level coverage on 5G Adoption - Investment and Commercialization Trends

- 7.3 Total Cell-site Backhaul, Macro, and Small Cell-site Backhaul Usage - In Percentage (Microwave, Satellite, Sub-6 GHz)

- 7.4 Market Outlook

8 MARKET SEGMENTATION

- 8.1 Form Factor

- 8.1.1 Modules

- 8.1.2 CPE (Indoor/Outdoor)

- 8.1.3 Smartphone

- 8.1.4 Hotspots

- 8.1.5 Laptops

- 8.1.6 Industrial Grade CPE/Router/Gateway

- 8.1.7 Other Form Factors

- 8.2 Spectrum Support

- 8.2.1 Sub-6 GHz

- 8.2.2 mmWave

- 8.2.3 Both Spectrum Bands

- 8.3 Geography

- 8.3.1 North America

- 8.3.1.1 United States

- 8.3.1.2 Canada

- 8.3.2 Europe

- 8.3.2.1 Germany

- 8.3.2.2 UK

- 8.3.2.3 France

- 8.3.2.4 Spain

- 8.3.2.5 Rest of Europe

- 8.3.3 Asia-Pacific

- 8.3.3.1 China

- 8.3.3.2 Japan

- 8.3.3.3 India

- 8.3.3.4 Australia

- 8.3.3.5 Rest of Asia-Pacific

- 8.3.4 Latin America

- 8.3.4.1 Brazil

- 8.3.4.2 Mexico

- 8.3.4.3 Argentina

- 8.3.4.4 Rest of Latin America

- 8.3.5 Middle East and Africa

- 8.3.5.1 UAE

- 8.3.5.2 Saudi Arabia

- 8.3.5.3 South Africa

- 8.3.5.4 Rest of Middle East and Africa

- 8.3.1 North America

9 COMPETITIVE LANDSCAPE

- 9.1 Company Profiles

- 9.1.1 ZTE Corporation

- 9.1.2 Cisco Systems Inc

- 9.1.3 Nokia Corporation

- 9.1.4 Huawei Technologies Co. Ltd

- 9.1.5 Samsung Electronics Co. Ltd

- 9.1.6 Xiaomi Corporation

- 9.1.7 Motorola Mobility LLC (Lenovo Group Limited)

- 9.1.8 BBK Electronics Corporation

- 9.1.9 Keysight Technologies Inc.

10 INVESTMENT ANALYSIS

11 MARKET OPPORTUNITIES AND FUTURE TRENDS