PUBLISHER: Roots Analysis | PRODUCT CODE: 1830064

PUBLISHER: Roots Analysis | PRODUCT CODE: 1830064

Medical Device Coating and Surface Modification Market, Industry Trends and Global Forecasts, Till 2035: Distribution by Type of Medical Devices Coated, Type of Coating, Type of Coating Material, Company Size, and Geographical Regions

Medical Device Coatings Market: Overview

As per Roots Analysis, the global medical device coatings market size is currently valued at USD 8.8 billion and is projected to reach USD 17.3 billion by 2040, growing at a CAGR of 7.1% during the forecast period.

The opportunity for medical device coating market has been distributed across the following segments:

Type of Medical Device Coated

- Class I Devices

- Class II Devices

- Class III Devices

Type of Coating

- Hydrophilic

- Hydrophobic

Type of Coating Material

- Polymer Coatings

- Metal Coatings

- Other Coatings

Company Size

- Small

- Mid-sized

- Large

Geographical Regions

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and North Africa

Market in North America

- US

- Canada

Market in Europe

- Germany

- France

- Italy

- Spain

- UK

- Switzerland

- Poland

- Belgium

- Netherlands

- Rest of the Europe

Market in Asia-Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of the Asia-Pacific

Market in Latin America

- Brazil

- Mexico

- Argentina

- Rest of Latin America

Market in Middle East and North Africa

- Saudi Arabia

- Egypt

- Israel

- Rest of Middle East and North Africa

Medical Device Coatings Market: Growth and Trends

The demand for advanced medical devices is increasing, primarily due to the rise in elderly population, the higher occurrence of chronic illnesses, and the growing requirement for minimally invasive techniques. Medical device coatings are specialized coatings utilized in the healthcare sector to improve the performance, longevity, and safety of different medical instruments and equipment. These coatings enhance biocompatibility, decrease friction, offer antimicrobial features, and safeguard against corrosion. They are essential for ensuring the safety and efficacy of medical devices in various medical procedures.

The World Health Organization (WHO) states that currently, there are approximately two million medical devices available worldwide. With the advancement of medical devices, there is an urgent need for coatings that can fulfill the operational, clinical, and engineering demands of these technologies.

Medical device coatings offer various advantages that cater to the changing demands of the healthcare and pharmaceutical sectors. Currently, several hydrophilic coatings are in the market to meet the growing need for innovative medical devices. Moreover, different medical device makers are employing innovative surface modification techniques to improve physiochemical characteristics, minimize frictional resistance, and in some instances, the arrangement of the device substrate, thus improving both performance and patient results.

Medical coatings are being more widely used due to their simple application, effectiveness against microbes, and compatibility with biological systems. Consequently, there is a significant demand to enhance coating technologies and polymers to facilitate continual expansion in the worldwide medical device coating sector. Fueled by the growing incidence of chronic illnesses, advancements in technology, and a heightened emphasis on minimizing hospital-acquired infections, the medical device coating sector is expected to experience consistent growth in the next decade.

Medical Device Coatings Market: Key Insights

The report delves into the current state of the medical device coatings market and identifies potential growth opportunities within the industry. The key takeaways of the report are:

- Presently, more than 80 players are offering services for medical device coating across the globe; a relatively large proportion (70%) of these companies are based in North America.

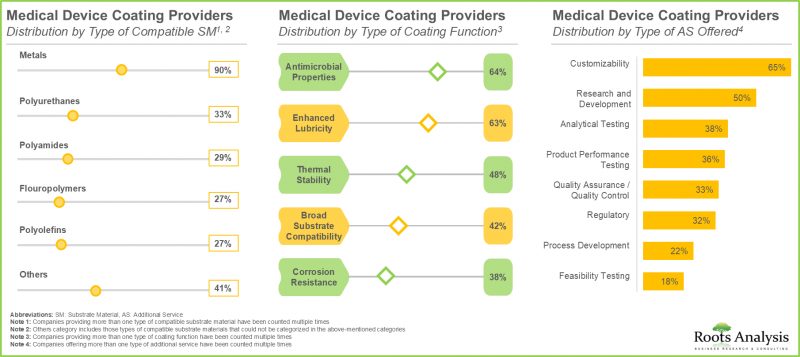

- Majority (64%) of companies are focused on providing coating materials that offer antimicrobial properties, primarily due to the increased risk of pathogen contamination associated with medical implants.

- Over 140 surface modification technologies and coating solutions are being offered by various firms; the market is characterized by the presence of both small and mid-sized companies.

- Notably, 85% of surface modification technologies and coating solutions utilize synthetic coating materials, which are applied to a wide range of compatible substrates to enhance device performance and safety.

- Likewise, a wide range of surface modification technologies / coatings are being provided by players across different regions to strengthen their respective offering portfolios.

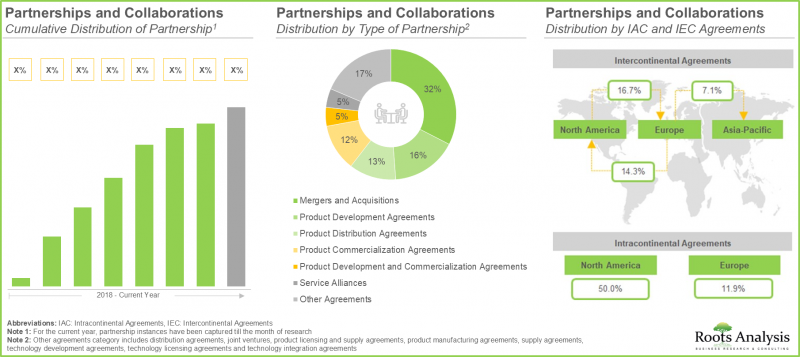

- The continuous interest of stakeholders in this domain is evident from the ongoing partnership activity; 62% of the total number of partnerships have been signed in the last five years.

- Driven by a range of factors, including the growing demand for minimally invasive surgeries and escalating global population with health issues, this market is poised to grow significantly over the coming years.

- The medical device coating market is likely to grow at a CAGR of 7.1% till 2035; this can be attributed to the rising preference for minimally invasive procedures leading to growing demand for coated devices.

- The global medical device coating market is currently dominated by mid-sized companies, and this trend is expected to remain unchanged in the coming years as well.

Medical Device Coatings Market: Key Segments

Class III Device Holds the Largest Share in the Current Year

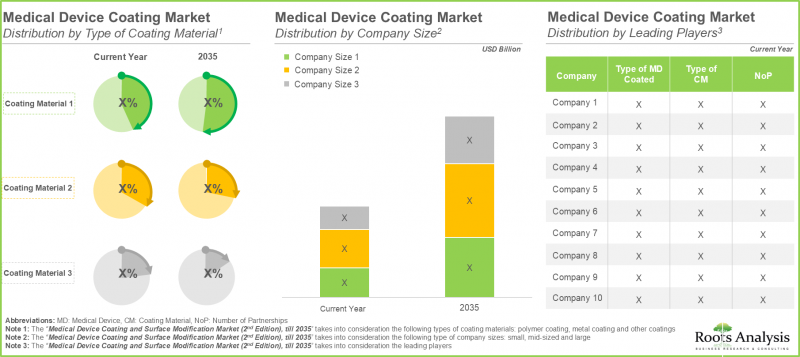

The medical device coatings market size is segmented into different types of medical devices coated, namely class I, class II and class III. In the current year, majority of the market share is captured by class III devices and is likely to grow at a relatively higher CAGR during the forecast period. This can be attributed to the stringent regulatory standards imposed by FDA guidelines, particularly the Premarket Approval (PMA) process, thereby increasing their requirement for advanced coatings that can facilitate regulatory acceptance.

Opportunities for Hydrophilic Coating Market in the Coming Future

Based on the type of coatings, the market is segmented across different types of coatings, such as hydrophilic and hydrophobic. The hydrophilic segment is likely to capture majority of the share in the current year (62%) and the trend is unlikely to change in the future as well.

Currently, Polymer Coatings Hold the Largest Share

The global market is segmented across different types of coating material, namely polymer coatings, metal coatings and other coatings. Currently, polymer-based coating material captures the highest market share (45.5%). This can be attributed to the benefits of polymer-based coating materials, such as cost efficiency, their light weight and customizability, making them suitable for diverse medical device applications.

Mid-sized Companies are Likely to Dominate Medical Device Coating Market

Based on the company size, the medical device coating industry is segmented across company size, namely small, mid-sized and large companies. The mid-sized players are likely to capture most (41%) of the market till 2035. The participation of mid-sized firms in the research and development of innovative coatings contributes to their significant market presence. Further, the market of small companies is likely to grow at a relatively higher CAGR till 2035.

Asia-Pacific to Propel in the Medical Device Coating Sector in the Coming Years

This segment highlights the distribution of the market across various geographies, namely North America, Europe, Asia-Pacific, Latin America, and Middle East and North Africa. According to our projections, North America is likely to capture the majority share (49%) in the overall market in the present year, and this trend is unlikely to change in the future. Further, the market in Asia-Pacific is likely to grow at a relatively higher CAGR (8.4%), during the till 2035.

Example Players in the Medical Device Coatings Market

- Advanced Coating

- Biocoat

- BioInteractions

- Biomerics

- Formacoat

- Harland Medical Systems

- LVD Biotech

- Para-Coat Technologies

- Polyzen

- Specialty Coating Systems

- Surmodics

- TUA Systems

Medical Device Coatings Market: Research Coverage

The report on medical device coatings market features insights into various sections, including:

- Market Sizing and Opportunity Analysis: An in-depth analysis of current market opportunity and the future growth potential of medical device coatings market, focusing on key market segments, including [A] type of medical device coated, [B] type of coating, [C] type of coating material, [D] company size, and [E] geographical regions.

- Market Landscape: A comprehensive evaluation of medical device coatings market, based on several relevant parameters, such as [A] type of medical device coated, [B] type of coating, [C] nature of coating material, [D] type of compatible substrate, [E] type of coating Function [F] year of establishment, [F] company size and [F] location of headquarters.

- Technology Landscape: A detailed analysis of medical device surface modification technologies and coating solutions, based on several relevant parameters, such as [A type of medium used for modification, [B] type of coating process employed, and [C] type of compatible substrate material, [D] type of coating, [E] type of resistance offered, [F] coating feature, [G] year of establishment, [H] company size and [I] location of headquarters.

- Company Competitiveness Analysis: An insightful competitiveness analysis of various medical device coating providers, based on various relevant parameters, such as [A] company strength, [B] portfolio strength, and [C] portfolio diversity.

- Technology Competitive Analysis: A detailed technology competitiveness analysis of the various surface modification technologies and coating solutions, based on several relevant parameters, such as [A] company strength, [B] technology strength and [C] coating features.

- Company Profiles: Comprehensive profiles of medical device coating providers, featuring information on [A] company overview, [B] financial information (if available), [C] medical device portfolio, [D] recent developments, and [E] future outlook statements.

- Partnerships and Collaborations: A detailed analysis of partnerships inked between stakeholders in the medical device coatings market , based on several relevant parameters, such as [A] year of partnership, [B] type of partnership, [C] type of partner, [D], end user, [E] most active players, and [F] geography.

- PESTLE Analysis: An insightful analysis of the leading medical device coating providers, considering the [A] affiliated factors, [B] key drivers, and [C] challenges under the PESTLE framework, highlighting the relative effect of each factor on the medical device coating providers.

- Market Impact Analysis: A thorough analysis of various factors, such as [A] drivers, [B] restraints, [C] opportunities, and [D] existing challenges that are likely to impact market growth.

Key Questions Answered in this Report

- How many companies are currently engaged in this market?

- Which are the leading companies in this market?

- What factors are likely to influence the evolution of this market?

- What is the current and future market size?

- What is the CAGR of this market?

- How is the current and future market opportunity likely to be distributed across key market segments?

Reasons to Buy this Report

- The report provides a comprehensive market analysis, offering detailed revenue projections of the overall market and its specific sub-segments. This information is valuable to both established market leaders and emerging entrants.

- Stakeholders can leverage the report to gain a deeper understanding of the competitive dynamics within the market. By analyzing the competitive landscape, businesses can make informed decisions to optimize their market positioning and develop effective go-to-market strategies.

- The report offers stakeholders a comprehensive overview of the market, including key drivers, barriers, opportunities, and challenges. This information empowers stakeholders to stay abreast of market trends and make data-driven decisions to capitalize on growth prospects.

Additional Benefits

- Complimentary PPT Insights Packs

- Complimentary Excel Data Packs for all Analytical Modules in the Report

- 15% Free Content Customization

- Detailed Report Walkthrough Session with Research Team

- Free Updated report if the report is 6-12 months old or older

TABLE OF CONTENTS

SECTION I: REPORT OVERVIEW

1. PREFACE

- 1.1. Introduction

- 1.2. Market Share Insights

- 1.3. Key Market Insights

- 1.4. Report Coverage

- 1.5. Key Questions Answered

- 1.6. Chapter Outlines

2. RESEARCH METHODOLOGY

- 2.1. Chapter Overview

- 2.2. Research Assumptions

- 2.2.1. Market Landscape and Market Trends

- 2.2.2. Market Forecast and Opportunity Analysis

- 2.2.3. Comparative Analysis

- 2.3. Database Building

- 2.3.1. Data Collection

- 2.3.2. Data Validation

- 2.3.3. Data Analysis

- 2.4. Project Methodology

- 2.4.1. Secondary Research

- 2.4.1.1. Annual Reports

- 2.4.1.2. Academic Research Papers

- 2.4.1.3. Company Websites

- 2.4.1.4. Investor Presentations

- 2.4.1.5. Regulatory Filings

- 2.4.1.6. White Papers

- 2.4.1.7. Industry Publications

- 2.4.1.8. Conferences and Seminars

- 2.4.1.9. Government Portals

- 2.4.1.10. Media and Press Releases

- 2.4.1.11. Newsletters

- 2.4.1.12. Industry Databases

- 2.4.1.13. Roots Proprietary Databases

- 2.4.1.14. Paid Databases and Sources

- 2.4.1.15. Social Media Portals

- 2.4.1.16. Other Secondary Sources

- 2.4.2. Primary Research

- 2.4.2.1. Types of Primary Research

- 2.4.2.1.1. Qualitative Research

- 2.4.2.1.2. Quantitative Research

- 2.4.2.1.3. Hybrid Approach

- 2.4.2.2. Advantages of Primary Research

- 2.4.2.3. Techniques for Primary Research

- 2.4.2.3.1. Interviews

- 2.4.2.3.2. Surveys

- 2.4.2.3.3. Focus Groups

- 2.4.2.3.4. Observational Research

- 2.4.2.3.5. Social Media Interactions

- 2.4.2.4. Key Opinion Leaders Considered in Primary Research

- 2.4.2.4.1. Company Executives (CXOs)

- 2.4.2.4.2. Board of Directors

- 2.4.2.4.3. Company Presidents and Vice Presidents

- 2.4.2.4.4. Research and Development Heads

- 2.4.2.4.5. Technical Experts

- 2.4.2.4.6. Subject Matter Experts

- 2.4.2.4.7. Scientists

- 2.4.2.4.8. Doctors and Other Healthcare Providers

- 2.4.2.5. Ethics and Integrity

- 2.4.2.5.1. Research Ethics

- 2.4.2.5.2. Data Integrity

- 2.4.2.1. Types of Primary Research

- 2.4.3. Analytical Tools and Databases

- 2.4.1. Secondary Research

- 2.5. Robust Quality Control

3. MARKET DYNAMICS

- 3.1. Chapter Overview

- 3.2. Forecast Methodology

- 3.2.1. Top-down Approach

- 3.2.2. Bottom-up Approach

- 3.2.3. Hybrid Approach

- 3.3. Market Assessment Framework

- 3.3.1. Total Addressable Market (TAM)

- 3.3.2. Serviceable Addressable Market (SAM)

- 3.3.3. Serviceable Obtainable Market (SOM)

- 3.3.4. Currently Acquired Market (CAM)

- 3.4. Forecasting Tools and Techniques

- 3.4.1. Qualitative Forecasting

- 3.4.2. Correlation

- 3.4.3. Regression

- 3.4.4. Extrapolation

- 3.4.5. Convergence

- 3.4.6. Sensitivity Analysis

- 3.4.7. Scenario Planning

- 3.4.8. Data Visualization

- 3.4.9. Time Series Analysis

- 3.4.10. Forecast Error Analysis

- 3.5. Key Considerations

- 3.5.1. Demographics

- 3.5.2. Government Regulations

- 3.5.3. Reimbursement Scenarios

- 3.5.4. Market Access

- 3.5.5. Supply Chain

- 3.5.6. Industry Consolidation

- 3.5.7. Pandemic / Unforeseen Disruptions Impact

- 3.6. Limitations

4. MACRO-ECONOMIC INDICATORS

- 4.1. Chapter Overview

- 4.2. Market Dynamics

- 4.2.1. Time Period

- 4.2.1.1. Historical Trends

- 4.2.1.2. Current and Forecasted Estimates

- 4.2.2. Currency Coverage

- 4.2.2.1. Major Currencies Affecting the Market

- 4.2.2.2. Factors Affecting Currency Fluctuations in the Industry

- 4.2.2.3. Impact of Currency Fluctuations on the Industry

- 4.2.3. Foreign Currency Exchange Rate

- 4.2.3.1. Impact of Foreign Exchange Rate Volatility on the Market

- 4.2.3.2. Strategies for Mitigating Foreign Exchange Risk

- 4.2.4. Recession

- 4.2.4.1. Assessment of Current Economic Conditions and Potential Impact on the Market

- 4.2.4.2. Historical Analysis of Past Recessions and Lessons Learnt

- 4.2.5. Inflation

- 4.2.5.1. Measurement and Analysis of Inflationary Pressures in the Economy

- 4.2.5.2. Potential Impact of Inflation on the Market Evolution

- 4.2.6. Interest Rates

- 4.2.6.1. Interest Rates and Their Impact on the Market

- 4.2.6.2. Strategies for Managing Interest Rate Risk

- 4.2.7. Commodity Flow Analysis

- 4.2.7.1. Type of Commodity

- 4.2.7.2. Origins and Destinations

- 4.2.7.3. Values and Weights

- 4.2.7.4. Modes of Transportation

- 4.2.8. Global Trade Dynamics

- 4.2.8.1. Import Scenario

- 4.2.8.2. Export Scenario

- 4.2.8.3. Trade Policies

- 4.2.8.4. Strategies for Mitigating the Risks Associated with Trade Barriers

- 4.2.8.5. Impact of Trade Barriers on the Market

- 4.2.9. War Impact Analysis

- 4.2.9.1. Russian-Ukraine War

- 4.2.9.2. Israel-Hamas War

- 4.2.10. COVID Impact / Related Factors

- 4.2.10.1. Global Economic Impact

- 4.2.10.2. Industry-specific Impact

- 4.2.10.3. Government Response and Stimulus Measures

- 4.2.10.4. Future Outlook and Adaptation Strategies

- 4.2.11. Other Indicators

- 4.2.11.1. Fiscal Policy

- 4.2.11.2. Consumer Spending

- 4.2.11.3. Gross Domestic Product

- 4.2.11.4. Employment

- 4.2.11.5. Taxes

- 4.2.11.6. Stock Market Performance

- 4.2.11.7. Cross Border Dynamics

- 4.2.1. Time Period

- 4.3. Conclusion

SECTION II: QUALITITAIVE INSIGHTS

5. EXECUTIVE SUMMARY

6. INTRODUCTION

- 6.1. Chapter Overview

- 6.2. Introduction to Medical Device Coating and Surface Modifications

- 6.2.1. Overview of Medical Device Coating

- 6.2.1.1. Types of Medical Device Coating

- 6.2.1.2. Advantages and Disadvantages of Medical Device Coating

- 6.2.2. Overview of Surface Modification Technologies

- 6.2.2.1. Type of Surface Modification Technologies

- 6.2.2.2. Advantages and Disadvantages of Surface Modification Technologies

- 6.2.1. Overview of Medical Device Coating

- 6.3. Future Perspectives

SECTION III: MARKET OVERVIEW

7. MARKET LANDSCAPE

- 7.1. Chapter Overview

- 7.2. Medical Device Coating Providers: Overall Market Landscape

- 7.2.1. Analysis by Year of Establishment

- 7.2.2. Analysis by Company Size

- 7.2.3. Analysis by Location of Headquarters

- 7.3. Medical Device Coating: Overall Market Landscape

- 7.3.1. Analysis by Type of Medical Device Coated

- 7.3.2. Analysis by Type of Coating

- 7.3.3. Analysis by Nature of Coating Material

- 7.3.4. Analysis by Type of Compatible Substrate

- 7.3.5. Analysis by Type of Coating Function

- 7.3.6. Analysis by Type of Additional Service Offered

8. TECHNOLOGY LANDSCAPE

- 8.1. Chapter Overview

- 8.2. Surface Modification Technologies and Coating Solutions: Overall Market Landscape

- 8.2.1. Analysis by Type of Medium Used for Modification

- 8.2.2. Analysis by Type of Coating Process Employed

- 8.2.3. Analysis by Type of Compatible Substrate

- 8.2.4. Analysis by Nature of Coating Material

- 8.2.5. Analysis by Type of Coating

- 8.2.6. Analysis by Type of Device Coated

- 8.2.7. Analysis by Type of Resistance Offered

- 8.2.8. Analysis by Coating Feature

- 8.3. Surface Modification Technologies and Coating Solutions: Providers Landscape

- 8.3.1. Analysis by Year of Establishment

- 8.3.2. Analysis by Company Size

- 8.3.3. Analysis by Location of Headquarters

9 COMPANY COMPETITIVENESS ANALYSIS

- 9.1. Chapter Overview

- 9.2. Assumptions and Key Parameters

- 9.3. Methodology

- 9.4. Medical Device Coating Providers: Company Competitiveness Analysis

- 9.4.1. Medical Device Coating Providers Based in North America (Peer Group I)

- 9.4.2. Medical Device Coating Providers Based in Europe (Peer Group II)

- 9.4.3. Medical Device Coating Providers Based in Asia-Pacific (Peer Group III)

10. TECHNOLOGY COMPETITIVENESS ANALYSIS

- 10.1. Chapter Overview

- 10.2. Assumptions and Key Parameters

- 10.3. Methodology

- 10.4. Surface Modification Technologies and Coating Solutions: Technology Competitiveness Analysis

- 10.4.1. Surface Modification Technologies and Coating Solutions in North America (Peer Group I)

- 10.4.2. Surface Modification Technologies and Coating Solutions in Europe (Peer Group II)

- 10.4.3. Surface Modification Technologies and Coating Solutions in Asia-Pacific (Peer Group III)

SECTION IV: COMPANY PROFILES

11. COMPANY PROFILES: MEDICAL DEVICE COATING PROVIDERS

- 11.1. Chapter Overview

- 11.2. Medical Device Coating Providers Based in North America

- 11.2.1. Advanced Coating

- 11.2.1.1. Company Overview

- 11.2.1.2. Medical Device Coating and Surface Modification Technology Portfolio

- 11.2.1.3. Recent Developments and Future Outlook

- 11.2.2. Biocoat

- 11.2.2.1. Company Overview

- 11.2.2.2. Medical Device Coating and Surface Modification Technology Portfolio

- 11.2.2.3. Recent Developments and Future Outlook

- 11.2.3. Formacoat

- 11.2.3.1. Company Overview

- 11.2.3.2. Medical Device Coating and Surface Modification Technology Portfolio

- 11.2.3.3. Recent Developments and Future Outlook

- 11.2.4. Harland Medical System

- 11.2.4.1. Company Overview

- 11.2.4.2. Medical Device Coating and Surface Modification Technology Portfolio

- 11.2.4.3. Recent Developments and Future Outlook

- 11.2.5. Para Coat Technologies

- 11.2.5.1. Company Overview

- 11.2.5.2. Medical Device Coating and Surface Modification Technology Portfolio

- 11.2.5.3. Recent Developments and Future Outlook

- 11.2.6. Surmodics

- 11.2.6.1. Company Overview

- 11.2.6.2. Financial Information

- 11.2.6.3. Medical Device Coating and Surface Modification Technology Portfolio

- 11.2.6.4. Recent Developments and Future Outlook

- 11.2.7. TUA Systems

- 11.2.7.1. Company Overview

- 11.2.7.2. Medical Device Coating and Surface Modification Technology Portfolio

- 11.2.7.3. Recent Developments and Future Outlook

- 11.2.8. Specialty Coating System

- 11.2.8.1. Company Overview

- 11.2.8.2. Medical Device Coating and Surface Modification Technology Portfolio

- 11.2.8.3. Recent Developments and Future Outlook

- 11.2.9. Polyzen

- 11.2.9.1. Company Overview

- 11.2.9.2. Medical Device Coating and Surface Modification Technology Portfolio

- 11.2.9.3. Recent Developments and Future Outlook

- 11.2.10. Biomerics

- 11.2.10.1. Company Overview

- 11.2.10.2. Medical Device Coating and Surface Modification Technology Portfolio

- 11.2.10.3. Recent Developments and Future Outlook

- 11.2.1. Advanced Coating

- 11.3. Medical Device Coating Providers Based in Europe

- 11.3.1. Biointeractions

- 11.3.1.1. Company Overview

- 11.3.1.2. Medical Device Coating and Surface Modification Technology Portfolio

- 11.3.1.3. Recent Developments and Future Outlook

- 11.3.2. LVD Biotech

- 11.3.2.1. Company Overview

- 11.3.2.2. Medical Device Coating and Surface Modification Technology Portfolio

- 11.3.2.3. Recent Developments and Future Outlook

- 11.3.1. Biointeractions

SECTION V: MARKET TRENDS

12. PARTNERSHIPS AND COLLABORATIONS

- 12.1. Chapter Overview

- 12.2. Partnership Models

- 12.3. Medical Device Coating Providers: Partnerships and Collaborations

- 12.3.1. Analysis by Year of Partnership

- 12.3.2. Analysis by Type of Partnership

- 12.3.3. Analysis by Year and Type of Partnership

- 12.3.4. Most Active Players: Analysis by Number of Partnerships

- 12.4. Analysis by Geography

- 12.4.1. Local and International Agreement

- 12.4.2. Intracontinental and Intercontinental Agreement

13. MEDICAL DEVICE COATING COMPANIES: PESTLE ANALYSIS

- 13.1. Chapter Overview

- 13.2. Methodology

- 13.3. Key Parameters

- 13.3.1. Political Factors

- 13.3.2. Economical Factors

- 13.3.3. Sociological Factors

- 13.3.4. Technological Factors

- 13.3.5. Legal Factors

- 13.3.6. Environmental Factors

- 13.4. PESTLE Analysis: Medical Device Coating Companies

- 13.4.1. Biocoat

- 13.4.2. Biomerics

- 13.4.3. Diamond-MT

- 13.4.4. Evonik Health Care

- 13.4.5. Fisher Barton

- 13.4.6. Formacoat

- 13.4.7. Freudenberg

- 13.4.8. Harland Medical Systems

- 13.4.9. Master Bond

- 13.4.10. Materion

- 13.4.11. N8 Medical

- 13.4.12. Para-Coat Technologies

- 13.4.13. Specialty Coating Systems

- 13.4.14. SurModics

- 13.4.15. Tractivus

- 13.5. Concluding Remarks

SECTION VI: MARKET OPPORTUNITY ANALYSIS

14. MARKET IMPACT ANALYSIS: DRIVERS, RESTRAINTS, OPPORTUNITIES AND CHALLENGES

- 14.1. Chapter Overview

- 14.2. Market Drivers

- 14.3. Market Restraints

- 14.4. Market Opportunities

- 14.5. Market Challenges

- 14.6. Conclusion

15. GLOBAL MEDICAL DEVICE COATING MARKET

- 15.1. Chapter Overview

- 15.2. Key Assumptions and Methodology

- 15.3. Global Medical Device Coatings Market, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 15.3.1. Scenario Analysis

- 15.3.1.1. Conservative Scenario

- 15.3.1.2. Optimistic Scenario

- 15.3.1. Scenario Analysis

- 15.4. Key Market Segmentations

16. MEDICAL DEVICE COATING MARKET, BY TYPE OF MEDICAL DEVICE

- 16.1. Chapter Overview

- 16.2. Assumptions and Methodology

- 16.2.1. Medical Device Coatings Market: Distribution by Type of Medical Device

- 16.2.1.1. Medical Device Coating Market for Class I, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 16.2.1.2. Medical Device Coating Market for Class II, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 16.2.1.3. Medical Device Coating Market for Class III, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 16.2.1. Medical Device Coatings Market: Distribution by Type of Medical Device

- 16.3. Data Triangulation and Validation

17. MEDICAL DEVICE COATING MARKET, BY TYPE OF COATING

- 17.1. Chapter Overview

- 17.2. Assumptions and Methodology

- 17.2.1. Medical Device Coatings Market: Distribution by Type of Coating

- 17.2.1.1. Medical Device Coating Market for Hydrophilic Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 17.2.1.2. Medical Device Coating Market for Hydrophobic Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 17.2.1.3. Medical Device Coating Market for Other Coating, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 17.2.1. Medical Device Coatings Market: Distribution by Type of Coating

- 17.3. Data Triangulation and Validation

18. MEDICAL DEVICE COATING MARKET, BY TYPE OF COATING MATERIAL

- 18.1. Chapter Overview

- 18.2. Assumptions and Methodology

- 18.2.1. Medical Device Coatings Market: Distribution by Type of Coating Material

- 18.2.1.1. Medical Device Coating Market for Polymer Coating, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 18.2.1.2. Medical Device Coating Market for Metal Coating, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 18.2.1.3. Medical Device Coating Market for Other Coating, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 18.2.1. Medical Device Coatings Market: Distribution by Type of Coating Material

- 18.3. Data Triangulation and Validation

19. MEDICAL DEVICE COATING MARKET, BY COMPANY SIZE

- 19.1. Chapter Overview

- 19.2. Assumptions and Methodology

- 19.2.1. Medical Device Coatings Market: Distribution by Company Size

- 19.2.1.1. Medical Device Coating Market for Small Companies, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 19.2.1.2. Medical Device Coating Market for Mid-Sized Companies, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 19.2.1.3. Medical Device Coating Market for Large Companies, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 19.2.1. Medical Device Coatings Market: Distribution by Company Size

- 19.3. Data Triangulation and Validation

20. MEDICAL DEVICE COATING MARKET, BY GEOGRAPHICAL REGIONS

- 20.1. Chapter Overview

- 20.2. Key Assumptions and Methodology

- 20.2.1. Medical Device Coating Market: Distribution by Key Geographical Regions

- 20.2.1.1. Medical Device Coating Market in North America, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 20.2.1.1.1. Medical Device Coating Market in the US, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 20.2.1.1.2. Medical Device Coating Market in Canada, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 20.2.1.2. Medical Device Coating Market in Europe, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 20.2.1.2.1. Medical Device Coating Market in Germany, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 20.2.1.2.2. Medical Device Coating Market in France, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 20.2.1.2.3. Medical Device Coating Market in Italy, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 20.2.1.2.4. Medical Device Coating Market in Spain, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 20.2.1.2.5. Medical Device Coating Market in UK, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 20.2.1.2.6. Medical Device Coating Market in Switzerland, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 20.2.1.2.7. Medical Device Coating Market in Poland, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 20.2.1.2.8. Medical Device Coating Market in Belgium, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 20.2.1.2.9. Medical Device Coating Market in Netherlands, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 20.2.1.2.10.Medical Device Coating Market in Rest of the Europe, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 20.2.1.3. Medical Device Coating Market in Asia-Pacific, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 20.2.1.3.1. Medical Device Coating Market in China, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 20.2.1.3.2. Medical Device Coating Market in Japan, H Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 20.2.1.3.3. Medical Device Coating Market in South Korea, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 20.2.1.3.4. Medical Device Coating Market in India, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 20.2.1.3.5. Medical Device Coating Market in Australia, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 20.2.1.3.6. Medical Device Coating Market in Rest of the Asia-Pacific, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 20.2.1.4. Medical Device Coating Market in Latin America, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 20.2.1.4.1. Medical Device Coating Market in Brazil, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 20.2.1.4.2. Medical Device Coating Market in Mexico, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 20.2.1.4.3. Medical Device Coating Market in Argentina, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 20.2.1.4.4. Medical Device Coating Market in Rest of Latin America, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 20.2.1.5. Medical Device Coating Market in Middle East and North Africa, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 20.2.1.5.1. Medical Device Coating Market in Saudi Arabia, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 20.2.1.5.2. Medical Device Coating Market in Egypt, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 20.2.1.5.3. Medical Device Coating Market in Israel, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 20.2.1.5.4. Medical Device Coating Market in Rest of Middle East and North Africa, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 20.2.1.1. Medical Device Coating Market in North America, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 20.2.2. Penetration Growth (P-G) Matrix

- 20.2.3. Market Movement Analysis

- 20.2.1. Medical Device Coating Market: Distribution by Key Geographical Regions

- 20.3. Data Triangulation and Validation

21. MEDICAL DEVICE COATING MARKET, BY LEADING DEVELOPERS

- 21.1. Chapter Overview

- 21.2. Assumptions and Methodology

- 21.2.1. Medical Device Coatings Market: Distribution by Leading Players

- 21.3. Data Triangulation and Validation

SECTION VII: OTHER EXCLUSIVE INSIGHTS

22. CONCLUDING REMARKS

23. EXECUTIVE INSIGHTS

- 23.1. Chapter Overview

- 23.2. Company A

- 23.2.1. Company Snapshot

- 23.2.2. Interview Transcript: Mark Eberhardt (Senior Director of Marketing)

- 23.3. Company B

- 23.3.1. Company Snapshot

- 23.3.2. Interview Transcript: Carl Genberg (Chief Scientific Officer)

- 23.4. Company C

- 23.4.1. Company Snapshot

- 23.4.2. Interview Transcript: David Wayne (Director of Sales and Marketing)

24. APPENDIX I: TABULATED DATA

25. APPENDIX II: LIST OF COMPANIES AND ORGANIZATIONS

List of Tables

- Table 7.1 Medical Device Coating Providers: Information on Year of Establishment, Company Size and Location of Headquarters

- Table 7.2 Medical Device Coating Providers: Information on Type of Medical Device Coated and Type of Coating

- Table 7.3 Medical Device Coating Providers: Information on Nature of Coating Material, Natural Coating Material and Synthetic Coating Material

- Table 8.1 Surface Modification Technologies and Coating Solutions: Information on Type of Medium Used for Modification and Type of Coating Process Employed

- Table 8.2 Surface Modification Technologies and Coating Solutions: Information on Type of Compatible Substrate Material and Nature of Coating Material

- Table 8.3 Surface Modification Technologies and Coating Solutions: Information on Type of Coating and Type of Device Coated

- Table 8.4 Surface Modification Technologies and Coating Solutions: Information on Type of Resistance Offered and Coating Feature

- Table 8.5 Surface Modification Technologies and Coating Solution Providers: Information on Year of Establishment, Company Size and Location of Headquarters

- Table 11.1 Medical Device Coating Providers: List of Companies Profiled

- Table 11.2 Advanced Coating: Company Overview

- Table 11.3 Advanced Coating: Medical Device Coating Portfolio

- Table 11.4 Biocoat: Company Overview

- Table 11.5 Biocoat: Medical Device Coating Portfolio

- Table 11.6 Biocoat: Recent Developments and Future Outlook

- Table 11.7 Fomacoat: Company Overview

- Table 11.8 Formacoat: Medical Device Coating Portfolio

- Table 11.9 Formacoat: Recent Developments and Future Outlook

- Table 11.10 Harland Medical Systems: Company Overview

- Table 11.11 Harland Medical Systems: Medical Device Coating Portfolio

- Table 11.12 Harland Medical Systems: Recent Developments and Future Outlook

- Table 11.13 Para Coat Technologies: Company Overview

- Table 11.14 Para Coat Technologies: Medical Device Coating Portfolio

- Table 11.15 Surmodics: Company Overview

- Table 11.16 Surmodics: Medical Device Coating Portfolio

- Table 11.17 Surmodics: Recent Developments and Future Outlook

- Table 11.18 TUA System: Company Overview

- Table 11.19 TUA System: Medical Device Coating Portfolio

- Table 11.20 Specialty Coating Systems: Company Overview

- Table 11.21 Specialty Coating Systems: Medical Device Coating Portfolio

- Table 11.22 Specialty Coating Systems: Recent Developments and Future Outlook

- Table 11.23 Polyzen: Company Overview

- Table 11.24 Polyzen: Medical Device Coating Portfolio

- Table 11.25 Biomerics: Company Overview

- Table 11.26 Biomerics: Medical Device Coating Portfolio

- Table 11.27 Biomerics: Recent Developments and Future Outlook

- Table 11.28 Biointeractions: Company Overview

- Table 11.29 Biointeractions: Medical Device Coating Portfolio

- Table 11.30 LVD Biotech: Company Overview

- Table 11.31 LVD Biotech: Medical Device Coating Portfolio

- Table 12.1 Medical Device Coating Providers: List of Partnerships and Collaborations, Till 2025

- Table 12.2 Partnerships and Collaborations: Information on Location of Headquarters and Type of Agreement

- Table 21.1 Leading Players in Medical Device Coating Market

- Table 23.1 Biocoat: Company Snapshot

- Table 23.2 N8 Medical: Company Snapshot

- Table 23.3 VaporTech: Company Snapshot

- Table 24.1 Medical Device Coating Providers: Distribution by Year of Establishment

- Table 24.2 Medical Device Coating Providers: Distribution by Company Size

- Table 24.3 Medical Device Coating Providers: Distribution by Headquarters

- Table 24.4 Medical Device Coating Providers: Distribution by Type of Medical Device Coated

- Table 24.5 Medical Device Coating Providers: Distribution by Type of Coating

- Table 24.6 Medical Device Coating Providers: Distribution by Nature of Coating Material

- Table 24.7 Medical Device Coating Providers: Distribution by Type of Compatible Substrate Material

- Table 24.8 Medical Device Coating Providers: Distribution by Type of Coating Function

- Table 24.9 Medical Device Coating Providers: Distribution by Additional Services Offered

- Table 24.10 Surface Modification Technologies and Coating Solutions: Distribution by Type of Medium Used for Modification

- Table 24.11 Surface Modification Technologies and Coating Solutions: Distribution by Type of Coating Process Employed

- Table 24.12 Surface Modification Technologies and Coating Solutions: Distribution by Type of Compatible Substrate

- Table 24.13 Surface Modification Technologies and Coating Solutions: Distribution by Nature of Coating Material

- Table 24.14 Surface Modification Technologies and Coating Solutions: Distribution by Type of Coating

- Table 24.15 Surface Modification Technologies and Coating Solutions: Distribution by Type of Device Coated

- Table 24.16 Surface Modification Technologies and Coatings: Distribution by Type of Resistance Offered

- Table 24.17 Surface Modification Technologies and Coating Solutions: Distribution by Coating Feature

- Table 24.18 Surface Modification Technologies and Coating Solution Providers: Distribution by Year of Establishment

- Table 24.19 Surface Modification Technologies and Coating Solution Providers: Distribution by Company Size

- Table 24.20 Surface Modification Technologies and Coating Solution Providers: Distribution by Location of Headquarters (Region)

- Table 24.21 Surface Modification Technologies and Coating Solution Providers: Distribution by Location of Headquarters (Country)

- Table 24.22 Partnerships and Collaborations: Cumulative Year-wise Trend, Till 2025

- Table 24.23 Partnerships and Collaborations: Distribution by Type of Partnership

- Table 24.24 Partnerships and Collaborations: Distribution by Year and Type of Partnership

- Table 24.25 Partnerships and Collaborations: Distribution by Agreement

- Table 24.26 Partnerships and Collaborations: Distribution by Country

- Table 24.27 Partnerships and Collaborations: Distribution by Region

- Table 24.28 Global Medical Device Coating Market, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Table 24.29 Global Medical Device Coating Market, Forecasted Estimates (Since 2023): Conservative Scenario (USD Billion)

- Table 24.30 Global Medical Device Coating Market, Forecasted Estimates (Since 2023): Optimistic Scenario (USD Billion)

- Table 24.31 Medical Device Coating Market: Distribution by Type of Medical Device Coated

- Table 24.32 Medical Device Coating Market for Class I Devices, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Table 24.32 Medical Device Coating Market for Class I Devices, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Table 24.33 Medical Device Coating Market for Class II Devices, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Table 24.34 Medical Device Coating Market for Class III Devices, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Table 24.35 Medical Device Coating Market: Distribution by Type of Coating

- Table 24.36 Medical Device Coating Market for Hydrophilic Coating, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Table 24.37 Medical Device Coating Market for Hydrophobic Coating, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Table 24.38 Medical Device Coating Market: Distribution by Type of Coating Material

- Table 24.39 Medical Device Coating Market for Polymer Coating, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Table 24.40 Medical Device Coating Market for Metal Coating, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Table 24.41 Medical Device Coating Market for Other Coatings, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Table 24.42 Medical Device Coating Market: Distribution by Company Size

- Table 24.43 Medical Device Coating Market for Small Companies, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Table 24.44 Medical Device Coating Market for Mid-sized Companies, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Table 24.45 Medical Device Coating Market for Large Companies, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Table 24.46 Medical Device Coating Market: Distribution by Geographical Region

- Table 24.47 Medical Device Coating Market in North America, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Table 24.48 Medical Device Coating Market in the US, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Table 24.49 Medical Device Coating Market in Canada, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Table 24.50 Medical Device Coating Market in Europe, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Table 24.51 Medical Device Coating Market in Germany, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Table 24.52 Medical Device Coating Market in France, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Table 24.53 Medical Device Coating Market in Italy, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Table 24.54 Medical Device Coating Market in Spain, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Table 24.55 Medical Device Coating Market in the UK, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Table 24.56 Medical Device Coating Market in Switzerland, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Table 24.57 Medical Device Coating Market in Poland, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Table 24.58 Medical Device Coating Market in Belgium, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Table 24.59 Medical Device Coating Market in the Netherlands, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Table 24.60 Medical Device Coating Market in Rest of Europe, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Table 24.61 Medical Device Coating Market in Asia-Pacific, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Table 24.62 Medical Device Coating Market in China, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Table 24.63 Medical Device Coating Market in Japan, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Table 24.64 Medical Device Coating Market in South Korea, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Table 24.65 Medical Device Coating Market in India, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Table 24.66 Medical Device Coating Market in Australia, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Table 24.67 Medical Device Coating Market in Rest of Asia-Pacific, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Table 24.68 Medical Device Coating Market in Latin America, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Table 24.69 Medical Device Coating Market in Brazil, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Table 24.70 Medical Device Coating Market in Mexico, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Table 24.71 Medical Device Coating Market in Argentina, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Table 24.72 Medical Device Coating Market in Rest of Latin America, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)(USD Billion)

- Table 24.73 Medical Device Coating Market in Middle East and North Africa, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Table 24.74 Medical Device Coating Market in Saudi Arabia, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Table 24.75 Medical Device Coating Market in Egypt, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Table 24.76 Medical Device Coating Market in Israel, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Table 24.77 Medical Device Coating Market in Rest of Middle East and North Africa, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

List of Figures

- Figure 2.1 Research Methodology: Project Methodology

- Figure 2.2 Research Methodology: Data Sources for Secondary Research

- Figure 2.3 Research Methodology: Robust Quality Control

- Figure 3.1 Market Dynamics: Forecast Methodology

- Figure 3.2 Market Dynamics: Key Market Segmentation

- Figure 4.1 Lessons Learnt from Past Recessions

- Figure 5.1 Executive Summary: Medical Device Coating Providers Market Landscape

- Figure 5.2 Executive Summary: Surface Modification Technologies and Coating Solutions: Technology Landscape

- Figure 5.3 Executive Summary: Partnerships and Collaborations

- Figure 5.4 Executive Summary: Market Forecast and Opportunity Analysis

- Figure 6.1 Features of Medical Device Coatings

- Figure 6.2 Advantages and Disadvantages of Medical Device Coatings

- Figure 6.3 Advantages and Disadvantages of Surface Modification Technologies

- Figure 7.1 Medical Device Coating Providers: Distribution by Year of Establishment

- Figure 7.2 Medical Device Coating Providers: Distribution by Company Size

- Figure 7.3 Medical Device Coatings Providers: Distribution by Location of Headquarters

- Figure 7.4 Medical Device Coating Providers: Distribution by Type of Medical Device Coated

- Figure 7.5 Medical Device Coating Providers: Distribution by Type of Coating

- Figure 7.6 Medical Device Coating Providers: Distribution by Nature of Coating Material

- Figure 7.7 Medical Device Coating Providers: Distribution by Type of Compatible Substrate Material

- Figure 7.8 Medical Device Coating Providers: Distribution by Type of Coating Function

- Figure 7.9 Medical Device Coating Providers: Distribution by Additional Service Offered

- Figure 8.1 Surface Modification Technologies and Coating Solutions: Distribution by Type of Medium Used for Modification

- Figure 8.2 Surface Modification Technologies and Coating Solutions: Distribution by Type of Coating Process Employed

- Figure 8.3 Surface Modification Technologies and Coating Solutions: Distribution by Type of Compatible Substrate Material

- Figure 8.4 Surface Modification Technologies and Coating Solutions: Distribution by Nature of Coating Material

- Figure 8.5 Surface Modification Technologies and Coating Solutions: Distribution by Type of Coating

- Figure 8.6 Surface Modification Technologies and Coating Solutions: Distribution by Type of Device Coated

- Figure 8.7 Surface Modification Technologies and Coatings: Distribution by Type of Resistance Offered

- Figure 8.8 Surface Modification Technologies and Coating Solutions: Distribution by Coating Feature

- Figure 8.9 Surface Modification Technologies and Coating Solution Providers: Distribution by Year of Establishment

- Figure 8.10 Surface Modification Technologies and Coating Solution Providers: Distribution by Company Size

- Figure 8.11 Surface Modification Technologies and Coating Solution Providers: Distribution by Location of Headquarters (Region)

- Figure 8.12 Surface Modification Technologies and Coating Solution Providers: Distribution by Location of Headquarters (Country)

- Figure 11.1 Surmodics: Business Segment-wise Revenues and Consolidated Financial Details (USD Million)

- Figure 12.1 Partnerships and Collaborations: Cumulative Year-wise Trend, Till 2025

- Figure 12.2 Partnerships and Collaborations: Distribution by Type of Partnership

- Figure 12.3 Partnerships and Collaborations: Distribution by Year and Type of Partnership

- Figure 12.4 Most Active Players: Distribution by Number of Partnerships

- Figure 12.5 Partnerships and Collaborations: Distribution by Local and International Agreements

- Figure 12.6 Partnerships and Collaborations: Distribution by Intracontinental and Intercontinental Agreements

- Figure 13.1 PESTLE Analysis: Impact of Internal and External Factors

- Figure 13.2 PESTLE Analysis: Key Factors

- Figure 13.3 PESTLE Analysis: Biocoat

- Figure 13.4 PESTLE Analysis: Biomerics

- Figure 13.5 PESTLE Analysis: Diamond-MT

- Figure 13.6 PESTLE Analysis: Evonik Health Care

- Figure 13.7 PESTLE Analysis: Fisher Barton

- Figure 13.8 PESTLE Analysis: Formacoat

- Figure 13.9 PESTLE Analysis: Freudenberg

- Figure 13.10 PESTLE Analysis: Harland Medical Systems

- Figure 13.11 PESTLE Analysis: Master Bond

- Figure 13.12 PESTLE Analysis: Materion

- Figure 13.13 PESTLE Analysis: N8 Medical

- Figure 13.14 PESTLE Analysis: Para-Coat Technologies

- Figure 13.15 PESTLE Analysis: Specialty Coating Systems

- Figure 13.16 PESTLE Analysis: SurModics

- Figure 13.17 PESTLE Analysis: Tractivus

- Figure 13.19 PESTLE Analysis: Concluding Remarks

- Figure 15.1 Global Medical Device Coating Market, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 15.2 Global Medical Device Coating Market, Forecasted Estimates (Since 2023): Conservative Scenario (USD Billion)

- Figure 15.3 Global Medical Device Coating Market, Forecasted Estimates (Since 2023): Optimistic Scenario (USD Billion)

- Figure 16.1 Medical Device Coating Market: Distribution by Type of Medical Device Coated

- Figure 16.2 Medical Device Coating Market for Class I, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 16.3 Medical Device Coating Market for Class II, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 16.4 Medical Device Coating Market for Class III, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 17.1 Medical Device Coatings Market: Distribution by Type of Coating Material

- Figure 17.2 Medical Device Coating Market for Hydrophilic Coating, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 17.3 Medical Device Coating Market for Hydrophobic Coating, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 17.4 Medical Device Coating Market for Other Coatings, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 18.1 Medical Device Coatings Market: Distribution by Type of Coating Material

- Figure 18.2 Medical Device Coating Market for Polymer Coating, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 18.3 Medical Device Coating Market for Metal Coating, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 18.4 Medical Device Coating Market for Other Coating, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 19.1 Medical Device Coating Market: Distribution by Company Size

- Figure 19.2 Medical Device Coating Market for Small Companies, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 19.3 Medical Device Coating Market for Mid-Sized Companies, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 19.4 Medical Device Coating Market for Large Companies, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 20.1 Medical Device Coating Market: Distribution by Key Geographical Regions

- Figure 20.2 Medical Device Coating Market in North America, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 20.3 Medical Device Coating Market in the US, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 20.4 Medical Device Coating Market in Canada, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 20.5 Medical Device Coating Market in Europe, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 20.6 Medical Device Coating Market in Germany, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 20.7 Medical Device Coating Market in France, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 20.8 Medical Device Coating Market in Italy, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 20.9 Medical Device Coating Market in Spain, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 20.10 Medical Device Coating Market in the UK, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 20.11 Medical Device Coating Market in Switzerland, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 20.12 Medical Device Coating Market in Poland, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 20.13 Medical Device Coating Market in Belgium, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 20.14 Medical Device Coating Market in Netherlands, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 20.15 Medical Device Coating Market in Rest of Europe, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 20.16 Medical Device Coating Market in Asia-Pacific, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 20.17 Medical Device Coating Market in China, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 20.18 Medical Device Coating Market in Japan, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 20.19 Medical Device Coating Market in South Korea, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 20.20 Medical Device Coating Market in India, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 20.21 Medical Device Coating Market in Australia, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 20.22 Medical Device Coating Market in Rest of the Asia-Pacific, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 20.23 Medical Device Coating Market in Latin America, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 20.24 Medical Device Coating Market in Brazil, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 20.25 Medical Device Coating Market in Mexico, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 20.26 Medical Device Coating Market in Argentina, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 20.27 Medical Device Coating Market in Rest of Latin America, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 20.28 Medical Device Coating Market in Middle East and North Africa, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 20.29 Medical Device Coating Market in Saudi Arabia, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 20.30 Medical Device Coating Market in Egypt, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 20.31 Medical Device Coating Market in Israel, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 20.32 Medical Device Coating Market in Rest of Middle East and North Africa, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 20.33 Penetration Growth (P-G) Matrix: Geographical Regions

- Figure 20.34 Market Movement Analysis: Geographical Regions

- Figure 22.1 Concluding Remarks: Medical Device Coating Providers Market Landscape

- Figure 22.2 Concluding Remarks: Surface Modification Technologies and Coating Solutions Market Landscape

- Figure 22.3 Concluding Remarks: Partnerships and Collaborations

- Figure 22.4 Concluding Remarks: PESTLE Analysis

- Figure 22.5 Concluding Remarks: Market Forecast and Opportunity Analysis