PUBLISHER: Roots Analysis | PRODUCT CODE: 1830278

PUBLISHER: Roots Analysis | PRODUCT CODE: 1830278

Microprocessor Market Till 2035: Distribution by Type of Architecture, Size, Bit Size, Core Count, Areas of Application, Type of Microprocessor, Company Size, and Key Geographical Regions: Industry Trends and Global Forecasts

Microprocessor Market Overview

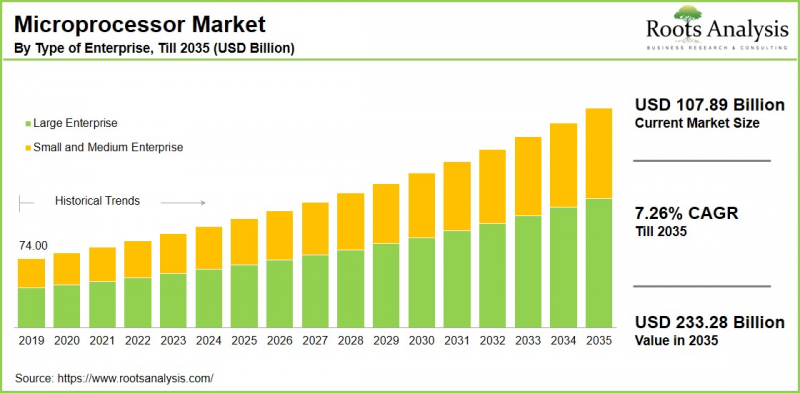

As per Roots Analysis, the global microprocessor market size is estimated to grow from USD 107.89 billion in the current year to USD 233.28 billion by 2035, at a CAGR of 7.26% during the forecast period, till 2035.

The opportunity for microprocessor market has been distributed across the following segments:

Type of Architecture

- Application Specific Integrated Circuit (ASIC)

- ARM MPU

- Complex Instruction Set Computer (CISC)

- Digital Signal Processor (DSP)

- MIPS

- Reduced Instruction Set Computer (RISC)

- Superscalar

- x64

- x86

Size

- Less than 10nm

- 10nm-22nm

- More than 28nm

Bit Size

- 4 bits

- 8 bits

- 16 bits

- 32 bits

- 64 bits

Core Count

- Less than 4 cores

- 8 cores

- 16 cores

- More than 32 cores

Areas of Application

- Aerospace and Defense

- Automotive and Transportation

- Consumer Electronics

- Embedded Devices

- Enterprise

- Industrial

- Medical Systems

- Networking and Communication

Type of Microprocessors

- APU

- Application-Specific Microprocessors

- CPU

- FPGA

- General-Purpose Microprocessors

- GPU

- Microcontrollers

Company Size

- Large Enterprises

- Small and Medium Enterprises

Geographical Regions

- North America

- US

- Canada

- Mexico

- Other North American countries

- Europe

- Austria

- Belgium

- Denmark

- France

- Germany

- Ireland

- Italy

- Netherlands

- Norway

- Russia

- Spain

- Sweden

- Switzerland

- UK

- Other European countries

- Asia

- China

- India

- Japan

- Singapore

- South Korea

- Other Asian countries

- Latin America

- Brazil

- Chile

- Colombia

- Venezuela

- Other Latin American countries

- Middle East and North Africa

- Egypt

- Iran

- Iraq

- Israel

- Kuwait

- Saudi Arabia

- UAE

- Other MENA countries

- Rest of the World

- Australia

- New Zealand

- Other countries

Microprocessor Market: Growth and Trends

Microprocessors are specialized integrated circuits (ICs) that function as the central processing units (CPUs) of computer systems. They are designed to execute complex instructions while carrying out arithmetic and logical operations. Unlike general-purpose ICs, microprocessors are specifically tailored for general computing tasks. In comparison, microcontrollers are ICs that integrate a microprocessor core with memory, input/output interfaces, and timers, forming a self-contained unit ideal for embedded systems and dedicated applications.

The growth of the consumer electronics market, which includes smartphones, tablets, laptops, and smart home devices, has a significant impact on the demand for microprocessors. As users increasingly seek devices with higher performance, improved energy efficiency, and advanced functionalities, manufacturers are compelled to adopt the latest microprocessor technologies. Owing to the rising demand, continuous innovation and advancements in microprocessor design, the microprocessor market is expected to grow significantly during the forecast period.

Microprocessor Market: Key Segments

Market Share by Type of Architecture

Based on type of architecture, the global microprocessor market is segmented into application specific integrated circuit (ASIC), ARM MPU, complex instruction set computer (CISC), digital signal processor (DSP), MIPS, reduced instruction set computer (RISC), superscalar, x64, and x86. According to our estimates, currently, the ARM MPU segment captures the majority of the market share and this trend is unlikely to change in future.

This can be attributed to the surging demand for ARM-based processors in smartphones and personal computers, driven by their energy efficiency and strong performance capabilities. Owing to these advantages, the ARM architecture is particularly well-suited for portable, low-power embedded systems, making it a core enabler of the mobile computing ecosystem.

On the other hand, the x64 segment is expected to grow at a higher CAGR during the forecast period, owing to its superior memory capacity and processing power compared to x86 processors. Unlike 32-bit x86 chips, x64 processors can efficiently handle double instruction sets, resulting in improved performance.

Market Share by Size

Based on size, the global microprocessor market is segmented into less than 10nm, 10nm-22nm, and more than 28nm. According to our estimates, currently, the 10nm-22nm segment captures the majority of the market share during the forecast period. This can be attributed to its optimal balance of performance and power efficiency, making this node size widely adopted across consumer electronics and high-performance computing applications.

However, the less than 10nm segment is anticipated to grow at a relatively higher rate during the forecast period, owing to the growing demand for high-performance processors in advanced fields such as artificial intelligence (AI), machine learning (ML), and next-generation computing systems.

Market Share by Bit Size

Based on bit size, the global microprocessor market is segmented into bulk materials and less than 4 bits, 8 bits, 16 bits, 32 bits, and 64 bits. According to our estimates, currently, the 32 bits segment captures the majority of the market share.

This can be attributed to the extensive use of 32-bit processors in electronics and embedded systems, as they offer a balanced mix of performance, efficiency, and broad software compatibility. Their versatility has ensured sustained demand across diverse applications.

Market Share by Core Count

Based on core count, the global microprocessor market is segmented into less than 4 cores, 8 cores, 16 cores and more than 32 cores. According to our estimates, currently, the 8 cores segment captures the majority of the market share. This can be attributed to their widespread adoption across diverse applications, offering an effective balance between performance and energy efficiency.

On the other hand, the 16 cores segment is expected to grow at a higher CAGR during the forecast period. This rapid expansion is fueled by technological advancements in multi-core architecture, enabling manufacturers to design chips that integrate both performance and efficiency cores. Such processors are increasingly suited for high-demand applications like gaming, multimedia content creation, and artificial intelligence (AI).

Market Share by Areas of Application

Based on areas of application, the global microprocessor market is segmented into aerospace and defense, automotive and transportation, consumer electronics, embedded devices, enterprise, industrial, medical systems, and networking and communication. According to our estimates, currently, the consumer electronics segment captures the majority of the market share. This can be attributed to the strong demand for microprocessors that deliver enhanced performance and advanced functionality in devices such as smartphones, laptops, and smart home products.

On the other hand, the automotive and transportation segment is expected to grow at a higher CAGR during the forecast period. This surge reflects the rising integration of microprocessors into advanced driver assistance systems (ADAS), infotainment platforms, and other automotive technologies, where sophisticated processing power is essential.

Market Share by Type of Microprocessor

Based on type of microprocessor, the global microprocessor market is segmented into APU, application-specific microprocessors, CPU, FPGA, general-purpose microprocessors, GPU, and microcontrollers. According to our estimates, currently, the general-purpose microprocessors segment captures the majority of the market share. This can be attributed to their versatility and strong performance, which enable widespread adoption across multiple industries.

On the other hand, the application-specific microprocessors segment is expected to grow at a higher CAGR during the forecast period. This can be ascribed to the rising demand for specialized processing solutions in industries such as automotive, industrial automation, and consumer electronics, where tailored performance is critical.

Market Share by Company Size

Based on company size, the global microprocessor market is segmented into large and small and medium enterprise. According to our estimates, currently, the large enterprise segment captures the majority of the market share. This can be attributed to the strong demand for microprocessors that deliver enhanced performance and advanced functionality in devices such as smartphones, laptops, and smart home products.

On the other hand, the SME segment is expected to grow at a higher CAGR during the forecast period. This can be attributed to their agility, innovation-driven approach, and strong focus on niche technologies, which allow them to rapidly adapt to emerging trends and drive efficiency.

Market Share by Geographical Regions

Based on geographical regions, the microprocessor market is segmented into North America, Europe, Asia, Latin America, Middle East and North Africa, and the rest of the world. According to our estimates, currently, Asia captures the majority share of the market. This dominance is driven by government initiatives aimed at strengthening domestic semiconductor production and reducing reliance on imported microprocessors. Additionally, the expanding consumer base for smartphones, laptops, and other consumer electronics continues to accelerate demand for microprocessors across the region.

Example Players in Microprocessor Market

- Advanced Micro Devices

- Analog Devices

- Apple

- APU

- Broadcom

- GlobalFoundries

- HiSilicon Technologies

- IBM

- Intel

- Marvell Technology

- MediaTek

- Micron Technology

- Microchip Technology

- NVIDIA

- NXP Semiconductors

- Nuvoton Technology

- Renesas

- Samsung

- SK Hynix

- SiFive

- Sony

- Taiwan Semiconductor Manufacturing Company

- Texas Instruments

- The Western Design Center

- Toshiba

Microprocessor Market: Research Coverage

The report on the microprocessor market features insights on various sections, including:

- Market Sizing and Opportunity Analysis: An in-depth analysis of the microprocessor market, focusing on key market segments, including [A] type of architecture, [B] size, [C] bit size, [D] core count, [E] areas of application, [F] type of microprocessor, [G] company size, and [H] key geographical regions.

- Competitive Landscape: A comprehensive analysis of the companies engaged in the microprocessor market, based on several relevant parameters, such as [A] year of establishment, [B] company size, [C] location of headquarters and [D] ownership structure.

- Company Profiles: Elaborate profiles of prominent players engaged in the microprocessor market, providing details on [A] location of headquarters, [B] company size, [C] company mission, [D] company footprint, [E] management team, [F] contact details, [G] financial information, [H] operating business segments, [I] microprocessor portfolio, [J] moat analysis, [K] recent developments, and an informed future outlook.

- Megatrends: An evaluation of ongoing megatrends in the microprocessor industry.

- Patent Analysis: An insightful analysis of patents filed / granted in the microprocessor domain, based on relevant parameters, including [A] type of patent, [B] patent publication year, [C] patent age and [D] leading players.

- Recent Developments: An overview of the recent developments made in the microprocessor market, along with analysis based on relevant parameters, including [A] year of initiative, [B] type of initiative, [C] geographical distribution and [D] most active players.

- Porter's Five Forces Analysis: An analysis of five competitive forces prevailing in the microprocessor market, including threats of new entrants, bargaining power of buyers, bargaining power of suppliers, threats of substitute products and rivalry among existing competitors.

- SWOT Analysis: An insightful SWOT framework, highlighting the strengths, weaknesses, opportunities and threats in the domain. Additionally, it provides Harvey ball analysis, highlighting the relative impact of each SWOT parameter.

- Value Chain Analysis: A comprehensive analysis of the value chain, providing information on the different phases and stakeholders involved in the microprocessor market

Key Questions Answered in this Report

- How many companies are currently engaged in microprocessor market?

- Which are the leading companies in this market?

- What factors are likely to influence the evolution of this market?

- What is the current and future market size?

- What is the CAGR of this market?

- How is the current and future market opportunity likely to be distributed across key market segments?

Reasons to Buy this Report

- The report provides a comprehensive market analysis, offering detailed revenue projections of the overall market and its specific sub-segments. This information is valuable to both established market leaders and emerging entrants.

- Stakeholders can leverage the report to gain a deeper understanding of the competitive dynamics within the market. By analyzing the competitive landscape, businesses can make informed decisions to optimize their market positioning and develop effective go-to-market strategies.

- The report offers stakeholders a comprehensive overview of the market, including key drivers, barriers, opportunities, and challenges. This information empowers stakeholders to stay abreast of market trends and make data-driven decisions to capitalize on growth prospects.

Additional Benefits

- Complimentary Excel Data Packs for all Analytical Modules in the Report

- 15% Free Content Customization

- Detailed Report Walkthrough Session with Research Team

- Free Updated report if the report is 6-12 months old or older

TABLE OF CONTENTS

SECTION I: REPORT OVERVIEW

1. PREFACE

- 1.1. Introduction

- 1.2. Market Share Insights

- 1.3. Key Market Insights

- 1.4. Report Coverage

- 1.5. Key Questions Answered

- 1.6. Chapter Outlines

2. RESEARCH METHODOLOGY

- 2.1. Chapter Overview

- 2.2. Research Assumptions

- 2.3. Database Building

- 2.3.1. Data Collection

- 2.3.2. Data Validation

- 2.3.3. Data Analysis

- 2.4. Project Methodology

- 2.4.1. Secondary Research

- 2.4.1.1. Annual Reports

- 2.4.1.2. Academic Research Papers

- 2.4.1.3. Company Websites

- 2.4.1.4. Investor Presentations

- 2.4.1.5. Regulatory Filings

- 2.4.1.6. White Papers

- 2.4.1.7. Industry Publications

- 2.4.1.8. Conferences and Seminars

- 2.4.1.9. Government Portals

- 2.4.1.10. Media and Press Releases

- 2.4.1.11. Newsletters

- 2.4.1.12. Industry Databases

- 2.4.1.13. Roots Proprietary Databases

- 2.4.1.14. Paid Databases and Sources

- 2.4.1.15. Social Media Portals

- 2.4.1.16. Other Secondary Sources

- 2.4.2. Primary Research

- 2.4.2.1. Introduction

- 2.4.2.2. Types

- 2.4.2.2.1. Qualitative

- 2.4.2.2.2. Quantitative

- 2.4.2.3. Advantages

- 2.4.2.4. Techniques

- 2.4.2.4.1. Interviews

- 2.4.2.4.2. Surveys

- 2.4.2.4.3. Focus Groups

- 2.4.2.4.4. Observational Research

- 2.4.2.4.5. Social Media Interactions

- 2.4.2.5. Stakeholders

- 2.4.2.5.1. Company Executives (CXOs)

- 2.4.2.5.2. Board of Directors

- 2.4.2.5.3. Company Presidents and Vice Presidents

- 2.4.2.5.4. Key Opinion Leaders

- 2.4.2.5.5. Research and Development Heads

- 2.4.2.5.6. Technical Experts

- 2.4.2.5.7. Subject Matter Experts

- 2.4.2.5.8. Scientists

- 2.4.2.5.9. Doctors and Other Healthcare Providers

- 2.4.2.6. Ethics and Integrity

- 2.4.2.6.1. Research Ethics

- 2.4.2.6.2. Data Integrity

- 2.4.3. Analytical Tools and Databases

- 2.4.1. Secondary Research

3. MARKET DYNAMICS

- 3.1. Forecast Methodology

- 3.1.1. Top-Down Approach

- 3.1.2. Bottom-Up Approach

- 3.1.3. Hybrid Approach

- 3.2. Market Assessment Framework

- 3.2.1. Total Addressable Market (TAM)

- 3.2.2. Serviceable Addressable Market (SAM)

- 3.2.3. Serviceable Obtainable Market (SOM)

- 3.2.4. Currently Acquired Market (CAM)

- 3.3. Forecasting Tools and Techniques

- 3.3.1. Qualitative Forecasting

- 3.3.2. Correlation

- 3.3.3. Regression

- 3.3.4. Time Series Analysis

- 3.3.5. Extrapolation

- 3.3.6. Convergence

- 3.3.7. Forecast Error Analysis

- 3.3.8. Data Visualization

- 3.3.9. Scenario Planning

- 3.3.10. Sensitivity Analysis

- 3.4. Key Considerations

- 3.4.1. Demographics

- 3.4.2. Market Access

- 3.4.3. Reimbursement Scenarios

- 3.4.4. Industry Consolidation

- 3.5. Robust Quality Control

- 3.6. Key Market Segmentations

- 3.7. Limitations

4. MACRO-ECONOMIC INDICATORS

- 4.1. Chapter Overview

- 4.2. Market Dynamics

- 4.2.1. Time Period

- 4.2.1.1. Historical Trends

- 4.2.1.2. Current and Forecasted Estimates

- 4.2.2. Currency Coverage

- 4.2.2.1. Overview of Major Currencies Affecting the Market

- 4.2.2.2. Impact of Currency Fluctuations on the Industry

- 4.2.3. Foreign Exchange Impact

- 4.2.3.1. Evaluation of Foreign Exchange Rates and Their Impact on Market

- 4.2.3.2. Strategies for Mitigating Foreign Exchange Risk

- 4.2.4. Recession

- 4.2.4.1. Historical Analysis of Past Recessions and Lessons Learnt

- 4.2.4.2. Assessment of Current Economic Conditions and Potential Impact on the Market

- 4.2.5. Inflation

- 4.2.5.1. Measurement and Analysis of Inflationary Pressures in the Economy

- 4.2.5.2. Potential Impact of Inflation on the Market Evolution

- 4.2.6. Interest Rates

- 4.2.6.1. Overview of Interest Rates and Their Impact on the Market

- 4.2.6.2. Strategies for Managing Interest Rate Risk

- 4.2.7. Commodity Flow Analysis

- 4.2.7.1. Type of Commodity

- 4.2.7.2. Origins and Destinations

- 4.2.7.3. Values and Weights

- 4.2.7.4. Modes of Transportation

- 4.2.8. Global Trade Dynamics

- 4.2.8.1. Import Scenario

- 4.2.8.2. Export Scenario

- 4.2.9. War Impact Analysis

- 4.2.9.1. Russian-Ukraine War

- 4.2.9.2. Israel-Hamas War

- 4.2.10. COVID Impact / Related Factors

- 4.2.10.1. Global Economic Impact

- 4.2.10.2. Industry-specific Impact

- 4.2.10.3. Government Response and Stimulus Measures

- 4.2.10.4. Future Outlook and Adaptation Strategies

- 4.2.11. Other Indicators

- 4.2.11.1. Fiscal Policy

- 4.2.11.2. Consumer Spending

- 4.2.11.3. Gross Domestic Product (GDP)

- 4.2.11.4. Employment

- 4.2.11.5. Taxes

- 4.2.11.6. R&D Innovation

- 4.2.11.7. Stock Market Performance

- 4.2.11.8. Supply Chain

- 4.2.11.9. Cross-Border Dynamics

- 4.2.1. Time Period

SECTION II: QUALITATIVE INSIGHTS

5. EXECUTIVE SUMMARY

6. INTRODUCTION

- 6.1. Chapter Overview

- 6.2. Overview of Microprocessor Market

- 6.2.1. Type of Architecture

- 6.2.2. Type of Size

- 6.2.3. Type of Bit Size

- 6.2.4. Core Count

- 6.2.5. Areas of Application

- 6.2.6. Types of Microprocessors

- 6.3. Future Perspective

7. REGULATORY SCENARIO

SECTION III: MARKET OVERVIEW

8. COMPREHENSIVE DATABASE OF LEADING PLAYERS

9. COMPETITIVE LANDSCAPE

- 9.1. Chapter Overview

- 9.2. Edge Computing: Overall Market Landscape

- 9.2.1. Analysis by Year of Establishment

- 9.2.2. Analysis by Company Size

- 9.2.3. Analysis by Location of Headquarters

- 9.2.4. Analysis by Ownership Structure

10. WHITE SPACE ANALYSIS

11. COMPANY COMPETITIVENESS ANALYSIS

12. STARTUP ECOSYSTEM IN THE MICROPROCESSOR MARKET

- 12.1. Microprocessor Market: Market Landscape of Startups

- 12.1.1. Analysis by Year of Establishment

- 12.1.2. Analysis by Company Size

- 12.1.3. Analysis by Company Size and Year of Establishment

- 12.1.4. Analysis by Location of Headquarters

- 12.1.5. Analysis by Company Size and Location of Headquarters

- 12.1.6. Analysis by Ownership Structure

- 12.2. Key Findings

SECTION IV: COMPANY PROFILES

13. COMPANY PROFILES

- 13.1. Chapter Overview

- 13.2. Advanced Micro Devices*

- 13.2.1. Company Overview

- 13.2.2. Company Mission

- 13.2.3. Company Footprint

- 13.2.4. Management Team

- 13.2.5. Contact Details

- 13.2.6. Financial Performance

- 13.2.7. Operating Business Segments

- 13.2.8. Service / Product Portfolio (project specific)

- 13.2.9. MOAT Analysis

- 13.2.10. Recent Developments and Future Outlook

- 13.3. Analog Devices

- 13.4. Apple

- 13.5. APU

- 13.6. Broadcom

- 13.7. GlobalFoundries

- 13.8. HiSilicon Technologies

- 13.9. IBM

- 13.10. Intel

- 13.11. Marvell Technology

- 13.12. MediaTek

- 13.13. Micron Technology

- 13.14. Microchip Technology

- 13.15. NVIDIA

- 13.16. NXP Semiconductors

- 13.17. Nuvoton Technology

- 13.18. Renesas

- 13.19. Samsung

SECTION V: MARKET TRENDS

14. MEGA TRENDS ANALYSIS

15. UNMEET NEED ANALYSIS

16. PATENT ANALYSIS

17. RECENT DEVELOPMENTS

- 17.1. Chapter Overview

- 17.2. Recent Funding

- 17.3. Recent Partnerships

- 17.4. Other Recent Initiatives

SECTION VI: MARKET OPPORTUNITY ANALYSIS

18. GLOBAL MICROPROCESSOR MARKET

- 18.1. Chapter Overview

- 18.2. Key Assumptions and Methodology

- 18.3. Trends Disruption Impacting Market

- 18.4. Demand Side Trends

- 18.5. Supply Side Trends

- 18.6. Global Microprocessor Market, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 18.7. Multivariate Scenario Analysis

- 18.7.1. Conservative Scenario

- 18.7.2. Optimistic Scenario

- 18.8. Investment Feasibility Index

- 18.9. Key Market Segmentations

19. MARKET OPPORTUNITIES BASED ON TYPE OF ARCHITECTURE

- 19.1. Chapter Overview

- 19.2. Key Assumptions and Methodology

- 19.3. Revenue Shift Analysis

- 19.4. Market Movement Analysis

- 19.5. Penetration-Growth (P-G) Matrix

- 19.6. Microprocessor Market for Application Specific Integrated Circuit (ASIC): Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 19.7. Microprocessor Market for ARM MPU: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 19.8. Microprocessor Market for Complex Instruction Set Computer (CISC): Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 19.9. Microprocessor Market for Digital Signal Processor (DSP): Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 19.10. Microprocessor Market for MIPS: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 19.11. Microprocessor Market for Reduced Instruction Set Computer (RISC): Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 19.12. Microprocessor Market for Superscalar: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 19.13. Microprocessor Market for x64: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 19.14. Microprocessor Market for x86: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 19.15. Data Triangulation and Validation

- 19.15.1. Secondary Sources

- 19.15.2. Primary Sources

- 19.15.3. Statistical Modeling

20. MARKET OPPORTUNITIES BASED ON SIZE

- 20.1. Chapter Overview

- 20.2. Key Assumptions and Methodology

- 20.3. Revenue Shift Analysis

- 20.4. Market Movement Analysis

- 20.5. Penetration-Growth (P-G) Matrix

- 20.6. Microprocessor Market for Less than 10nm: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 20.7. Microprocessor Market for 10nm-22nm: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 20.8. Microprocessor Market for More than 28nm: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 20.9. Data Triangulation and Validation

- 20.9.1. Secondary Sources

- 20.9.2. Primary Sources

- 20.9.3. Statistical Modeling

21. MARKET OPPORTUNITIES BASED ON TYPE OF BIT SIZE

- 21.1. Chapter Overview

- 21.2. Key Assumptions and Methodology

- 21.3. Revenue Shift Analysis

- 21.4. Market Movement Analysis

- 21.5. Penetration-Growth (P-G) Matrix

- 21.6. Microprocessor Market for 4 bits: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 21.7. Microprocessor Market for 8 bits: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 21.8. Microprocessor Market for 16 bits: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 21.9. Microprocessor Market for 32 bits: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 21.10. Microprocessor Market for 64 bits: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 21.11. Data Triangulation and Validation

- 21.11.1. Secondary Sources

- 21.11.2. Primary Sources

- 21.11.3. Statistical Modeling

22. MARKET OPPORTUNITIES BASED ON CORE COUNT

- 22.1. Chapter Overview

- 22.2. Key Assumptions and Methodology

- 22.3. Revenue Shift Analysis

- 22.4. Market Movement Analysis

- 22.5. Penetration-Growth (P-G) Matrix

- 22.6. Microprocessor Market for Less than 4 cores: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 22.7. Microprocessor Market for 8 cores: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 22.8. Microprocessor Market for 16 cores: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 22.9. Microprocessor Market for More than 32 cores: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 22.10. Data Triangulation and Validation

- 22.10.1. Secondary Sources

- 22.10.2. Primary Sources

- 22.10.3. Statistical Modeling

23. MARKET OPPORTUNITIES BASED ON AREAS OF APPLICATION

- 23.1. Chapter Overview

- 23.2. Key Assumptions and Methodology

- 23.3. Revenue Shift Analysis

- 23.4. Market Movement Analysis

- 23.5. Penetration-Growth (P-G) Matrix

- 23.6. Microprocessor Market for Aerospace and Defense: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 23.7. Microprocessor Market for Automotive and Transportation: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 23.8. Microprocessor Market for Consumer Electronics: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 23.9. Microprocessor Market for Embedded Devices: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 23.10. Microprocessor Market for Enterprise: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 23.11. Microprocessor Market for Industrial: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 23.12. Microprocessor Market for Medical Systems: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 23.13. Microprocessor Market for Networking and Communication: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 23.14. Data Triangulation and Validation

- 23.14.1. Secondary Sources

- 23.14.2. Primary Sources

- 23.14.3. Statistical Modeling

24. MARKET OPPORTUNITIES BASED ON TYPE OF MICROPROCESSOR

- 24.1. Chapter Overview

- 24.2. Key Assumptions and Methodology

- 24.3. Revenue Shift Analysis

- 24.4. Market Movement Analysis

- 24.5. Penetration-Growth (P-G) Matrix

- 24.6. Microprocessor Market for APU: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.7. Microprocessor Market for Application-Specific Microprocessors: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.8. Microprocessor Market for CPU: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.9. Microprocessor Market for FPGA: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.10. Microprocessor Market for General-Purpose Microprocessors: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.11. Microprocessor Market for GPU: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.12. Microprocessor Market for Microcontrollers: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.13. Data Triangulation and Validation

- 24.13.1. Secondary Sources

- 24.13.2. Primary Sources

- 24.13.3. Statistical Modeling

25. MARKET OPPORTUNITIES FOR MICROPROCESSOR IN NORTH AMERICA

- 25.1. Chapter Overview

- 25.2. Key Assumptions and Methodology

- 25.3. Revenue Shift Analysis

- 25.4. Market Movement Analysis

- 25.5. Penetration-Growth (P-G) Matrix

- 25.6. Microprocessor Market in North America: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 25.6.1. Microprocessor Market in the US: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 25.6.2. Microprocessor Market in Canada: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 25.6.3. Microprocessor Market in Mexico: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 25.6.4. Microprocessor Market in Other North American Countries: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 25.7. Data Triangulation and Validation

26. MARKET OPPORTUNITIES FOR MICROPROCESSOR IN EUROPE

- 26.1. Chapter Overview

- 26.2. Key Assumptions and Methodology

- 26.3. Revenue Shift Analysis

- 26.4. Market Movement Analysis

- 26.5. Penetration-Growth (P-G) Matrix

- 26.6. Microprocessor Market in Europe: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 26.6.1. Microprocessor Market in Austria: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 26.6.2. Microprocessor Market in Belgium: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 26.6.3. Microprocessor Market in Denmark: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 26.6.4. Microprocessor Market in France: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 26.6.5. Microprocessor Market in Germany: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 26.6.6. Microprocessor Market in Ireland: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 26.6.7. Microprocessor Market in Italy: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 26.6.8. Microprocessor Market in Netherlands: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 26.6.9. Microprocessor Market in Norway: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 26.6.10. Microprocessor Market in Russia: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 26.6.11. Microprocessor Market in Spain: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 26.6.12. Microprocessor Market in Sweden: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 26.6.13. Microprocessor Market in Switzerland: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 26.6.14. Microprocessor Market in the UK: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 26.6.15. Microprocessor Market in Other European Countries: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 26.7. Data Triangulation and Validation

27. MARKET OPPORTUNITIES FOR MICROPROCESSOR IN ASIA

- 27.1. Chapter Overview

- 27.2. Key Assumptions and Methodology

- 27.3. Revenue Shift Analysis

- 27.4. Market Movement Analysis

- 27.5. Penetration-Growth (P-G) Matrix

- 27.6. Microprocessor Market in Asia: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 27.6.1. Microprocessor Market in China: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 27.6.2. Microprocessor Market in India: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 27.6.3. Microprocessor Market in Japan: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 27.6.4. Microprocessor Market in Singapore: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 27.6.5. Microprocessor Market in South Korea: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 27.6.6. Microprocessor Market in Other Asian Countries: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 27.7. Data Triangulation and Validation

28. MARKET OPPORTUNITIES FOR MICROPROCESSOR IN MIDDLE EAST AND NORTH AFRICA (MENA)

- 28.1. Chapter Overview

- 28.2. Key Assumptions and Methodology

- 28.3. Revenue Shift Analysis

- 28.4. Market Movement Analysis

- 28.5. Penetration-Growth (P-G) Matrix

- 28.6. Microprocessor Market in Middle East and North Africa (MENA): Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 28.6.1. Microprocessor Market in Egypt: Historical Trends (Since 2019) and Forecasted Estimates (Till 205)

- 28.6.2. Microprocessor Market in Iran: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 28.6.3. Microprocessor Market in Iraq: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 28.6.4. Microprocessor Market in Israel: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 28.6.5. Microprocessor Market in Kuwait: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 28.6.6. Microprocessor Market in Saudi Arabia: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 28.6.7. Microprocessor Market in United Arab Emirates (UAE): Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 28.6.8. Microprocessor Market in Other MENA Countries: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 28.7. Data Triangulation and Validation

29. MARKET OPPORTUNITIES FOR MICROPROCESSOR IN LATIN AMERICA

- 29.1. Chapter Overview

- 29.2. Key Assumptions and Methodology

- 29.3. Revenue Shift Analysis

- 29.4. Market Movement Analysis

- 29.5. Penetration-Growth (P-G) Matrix

- 29.6. Microprocessor Market in Latin America: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 29.6.1. Microprocessor Market in Argentina: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 29.6.2. Microprocessor Market in Brazil: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 29.6.3. Microprocessor Market in Chile: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 29.6.4. Microprocessor Market in Colombia Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 29.6.5. Microprocessor Market in Venezuela: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 29.6.6. Microprocessor Market in Other Latin American Countries: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 29.7. Data Triangulation and Validation

30. MARKET OPPORTUNITIES FOR MICROPROCESSOR IN REST OF THE WORLD

- 30.1. Chapter Overview

- 30.2. Key Assumptions and Methodology

- 30.3. Revenue Shift Analysis

- 30.4. Market Movement Analysis

- 30.5. Penetration-Growth (P-G) Matrix

- 30.6. Microprocessor Market in Rest of the World: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 30.6.1. Microprocessor Market in Australia: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 30.6.2. Microprocessor Market in New Zealand: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 30.6.3. Microprocessor Market in Other Countries

- 30.7. Data Triangulation and Validation

31. MARKET CONCENTRATION ANALYSIS: DISTRIBUTION BY LEADING PLAYERS

- 31.1. Leading Player 1

- 31.2. Leading Player 2

- 31.3. Leading Player 3

- 31.4. Leading Player 4

- 31.5. Leading Player 5

- 31.6. Leading Player 6

- 31.7. Leading Player 7

- 31.8. Leading Player 8

32. ADJACENT MARKET ANALYSIS

SECTION VII: STRATEGIC TOOLS

33. KEY WINNING STRATEGIES

34. PORTER FIVE FORCES ANALYSIS

35. SWOT ANALYSIS

36. VALUE CHAIN ANALYSIS

37. ROOTS STRATEGIC RECOMMENDATIONS

- 37.1. Chapter Overview

- 37.2. Key Business-related Strategies

- 37.2.1. Research & Development

- 37.2.2. Product Manufacturing

- 37.2.3. Commercialization / Go-to-Market

- 37.2.4. Sales and Marketing

- 37.3. Key Operations-related Strategies

- 37.3.1. Risk Management

- 37.3.2. Workforce

- 37.3.3. Finance

- 37.3.4. Others

SECTION VIII: OTHER EXCLUSIVE INSIGHTS

38. INSIGHTS FROM PRIMARY RESEARCH

39. REPORT CONCLUSION

SECTION IX: APPENDIX

40. TABULATED DATA

41. LIST OF COMPANIES AND ORGANIZATIONS

42. CUSTOMIZATION OPPORTUNITIES

43. ROOTS SUBSCRIPTION SERVICES

44. AUTHOR DETAILS