PUBLISHER: Roots Analysis | PRODUCT CODE: 1993594

PUBLISHER: Roots Analysis | PRODUCT CODE: 1993594

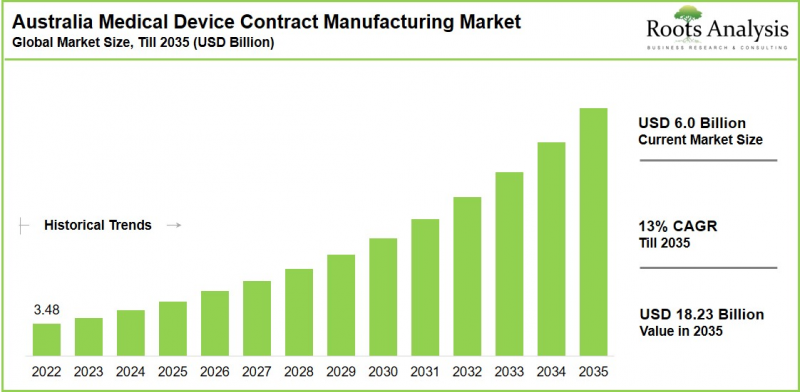

Australia Medical Device Contract Manufacturing Market - Distribution by Application Area, Target Therapeutic Area, and Device Class: Industry Trends and Global Forecasts, till 2035

Australia Medical Device Contract Manufacturing Market: Overview

As per Roots Analysis, the Australia medical device contract manufacturing market is estimated to grow from USD 6.0 billion in the current year to USD 18.23 billion by 2035 at a CAGR of 13% during the forecast period, till 2035.

Australia Medical Device Contract Manufacturing Market: Growth and Trends

The contract manufacturing medical devices (MDCMO) market is experiencing significant growth fueled by the increasing prevalence of chronic diseases worldwide. It is important to highlight that patients with chronic conditions require ongoing medical supervision to effectively manage their disease progression. However, many individuals face challenges while accessing healthcare facilities, including distance and the additional costs associated with diagnostic testing. To mitigate these challenges, medical devices and smart wearables are emerging as effective solutions, enabling remote monitoring of health metrics and delivery of appropriate interventions.

According to the World Health Organization, there are approximately two million distinct types of medical devices worldwide, classified into more than 7,000 general categories. These devices were developed to enhance patient adherence and allow for treatment without geographical constraints.. Medical device contract manufacturing functions as an outsourcing approach that utilizes specialized knowledge to produce particular components or complete devices for another organization. Notably, outsourcing medical device production provides significant advantages to firms in this sector by allowing them to bypass the need to set up manufacturing facilities, lower overall production expenses, and concentrate on their primary operations. Medical device contract manufacturers offer a range of outsourcing services, including device development, installation, manufacturing, quality assurance, regulatory guidance, and supply chain management.

Key elements driving the expansion of the medical device contract manufacturing market include the increasing elderly population and the demand for advanced technology-based devices for rapid monitoring. Additionally, the growing emphasis on patient-oriented medical devices for disease diagnosis and clinical research has amplified the need for cutting-edge remote monitoring equipment that assists in tracking health metrics from a distance.

The Australia medical device contract manufacturing market shows robust growth activity in the short-term, driven by outsourcing trends and demand for advanced devices such as next-generation implants, diagnostics, and wearable health monitors. This expansion is also fueled by an aging population, prompting original equipment manufacturers (OEMs) to partner with local CDMOs for cost efficiencies, thus reducing in-house capital needs faster time-to-market through specialized capabilities in Class III device assembly and regulatory compliance.

Growth Drivers: Strategic Enablers of Market Expansion

The market for medical device contract manufacturing in Australia is experiencing growth due to a rising demand for advanced medical devices, driven by the heightened need for diagnostics, implants, and equipment for home use. Companies outsource extensively to specialized contract manufacturers, slashing capital expenditures on facilities while accelerating development timelines through access to expertise of contract manufacturers. Further, technological advancements, including automation, 3D printing, and AI-driven quality control, enable faster prototyping and scalability, attracting numerous biotech firms and MedTech players alongside giants like Pfizer and Novartis that leverage local CDMOs for compliant production.

Market Challenges: Critical Barriers Impeding Progress

Despite encouraging development, Australia sector faces fundamental challenges that slows its swift progress in the medical device contract manufacturing market. Compliance with the Therapeutic Goods Administration (TGA)'s rigorous standards for Class I-III devices create significant barriers, demanding extensive documentation, audits, and validation that delay market entry and raise costs. Supply chain disruptions exacerbated by global events lead to raw material shortages for critical components like biocompatible polymers and electronics, forcing production halts and inventory stacking. In addition, heightened competition from low-cost Asian manufacturers pressures pricing, while skilled labor shortages in specialized areas like cleanroom operations and regulatory affairs further strain capacity amid rising demand.

Therapeutic Medical Devices Dominating Market Segment

In terms of application areas, the medical device contract manufacturing market is segmented into therapeutic medical devices, diagnostic medical devices, drug delivery medical devices and others. Our projections indicate that therapeutic medical devices hold the largest market share, anticipated to account for 31% of total revenue in the long term. This is due to the rising demand for therapeutic devices like insulin pumps, respiratory equipment, and infusion pumps used for managing chronic illnesses. However, the drug delivery devices have shown the highest growth potential and are estimated to grow at a higher CAGR during the forecast period.

Orthopedic Disorders: Leading Market Segment

In terms of therapeutic application area, the medical device contract manufacturing market is bifurcated into cardiovascular disorders, CNS disorders, metabolic disorders, oncological disorders, orthopedic disorders, ophthalmic disorders, pain disorders, respiratory disorders, and others. Fueled by the increasing need for orthopedic devices and advanced materials for joint replacements, along with other joint-related issues in the elderly population, orthopedic disorders are projected to hold the largest share (20.9%) by 2035.

However, over the long term, metabolic disorders have demonstrated significant growth potential and are expected to grow at a higher CAGR throughout the forecast period. This can be linked to the swift rise in metabolic conditions like obesity, insulin resistance, Type 1 diabetes, and hypertension. Individuals with metabolic disorders need constant monitoring to manage their health conditions, which is expected to raise the need for medical devices

Australia medical device contract manufacturing market: Key Segments

Application Areas

- Therapeutic Medical Devices

- Diagnostic Medical Devices

- Drug Delivery Medical Devices

- Other Devices

Device Class

- Class I

- Class II

- Class III

Target Therapeutic Area

- Cardiovascular Disorders

- CNS Disorders

- Metabolic Disorders

- Oncological Disorders

- Ophthalmological Disorders

- Orthopedic Disorders

- Pain Disorders

- Respiratory Disorders

- Others

Example Players in Australia Medical Device Contract Manufacturing Market

- Cochlear

- CSL

- Fisher & Paykel Healthcare

- Freudenberg Medical

- Johnson & Johnson

- Medtronic

- Nanosonics

- Osmosis Medical

- ResMed

Key Questions Answered in this Report

- How many medical device contract manufacturers are currently engaged in this market?

- Which are the leading companies in this market?

- What are the key trends observed in the Australia medical device contract manufacturing market?

- What factors are likely to influence the evolution of this market?

- What are the primary challenges faced by medical device contract manufacturing market in Australia?

- What is the current and future Australia medical device contract manufacturing market size?

- What is the CAGR of Australia medical device contract manufacturing market?

- How is the current and future market opportunity likely to be distributed across key market segments?

Reasons to Buy this Report

- The report provides a comprehensive market analysis, offering detailed revenue projections of the overall market and its specific sub-segments. This information is valuable to both established market leaders and emerging entrants.

- The report offers stakeholders a comprehensive overview of the market, including key drivers, barriers, opportunities, and challenges. This information empowers stakeholders to stay abreast of market trends and make data-driven decisions to capitalize on growth prospects.

- The report can aid businesses in identifying future opportunities in any sector. It also helps in understanding if those opportunities are worth pursuing.

- The report helps in identifying customer demand by understanding the needs, preferences, and behavior of the target audience in order to tailor products or services effectively.

- The report equips new entrants with requisite information regarding a particular market to help them build successful business strategies.

- The report allows for more effective communication with the audience and in building strong business relations.

Complementary Benefits

- Complimentary Excel Data Packs for all Analytical Modules in the Report

- 15% Free Content Customization

- Detailed Report Walkthrough Session with Research Team

- Free Updated report if the report is 6-12 months old or older

TABLE OF CONTENTS

1. PREFACE

- 1.1. Introduction

- 1.2. Market Share Insights

- 1.3. Key Market Insights

- 1.4. Report Coverage

- 1.5. Key Questions Answered

- 1.6. Chapter Outlines

2. RESEARCH METHODOLOGY

- 2.1. Chapter Overview

- 2.2. Research Assumptions

- 2.2.1. Market Landscape and Market Trends

- 2.2.2. Market Forecast and Opportunity Analysis

- 2.2.3. Comparative Analysis

- 2.3. Database Building

- 2.3.1. Data Collection

- 2.3.2. Data Validation

- 2.3.3. Data Analysis

- 2.4. Project Methodology

- 2.4.1. Secondary Research

- 2.4.1.1. Annual Reports

- 2.4.1.2. Academic Research Papers

- 2.4.1.3. Company Websites

- 2.4.1.4. Investor Presentations

- 2.4.1.5. Regulatory Filings

- 2.4.1.6. White Papers

- 2.4.1.7. Industry Publications

- 2.4.1.8. Conferences and Seminars

- 2.4.1.9. Government Portals

- 2.4.1.10. Media and Press Releases

- 2.4.1.11. Newsletters

- 2.4.1.12. Industry Databases

- 2.4.1.13. Roots Proprietary Databases

- 2.4.1.14. Paid Databases and Sources

- 2.4.1.15. Social Media Portals

- 2.4.1.16. Other Secondary Sources

- 2.4.2. Primary Research

- 2.4.2.1. Types of Primary Research

- 2.4.2.1.1. Qualitative Research

- 2.4.2.1.2. Quantitative Research

- 2.4.2.1.3. Hybrid Approach

- 2.4.2.2. Advantages of Primary Research

- 2.4.2.3. Techniques for Primary Research

- 2.4.2.3.1. Interviews

- 2.4.2.3.2. Surveys

- 2.4.2.3.3. Focus Groups

- 2.4.2.3.4. Observational Research

- 2.4.2.3.5. Social Media Interactions

- 2.4.2.4. Key Opinion Leaders Considered in Primary Research

- 2.4.2.4.1. Company Executives (CXOs)

- 2.4.2.4.2. Board of Directors

- 2.4.2.4.3. Company Presidents and Vice Presidents

- 2.4.2.4.4. Research and Development Heads

- 2.4.2.4.5. Technical Experts

- 2.4.2.4.6. Subject Matter Experts

- 2.4.2.4.7. Scientists

- 2.4.2.4.8. Doctors and Other Healthcare Providers

- 2.4.2.5. Ethics and Integrity

- 2.4.2.5.1. Research Ethics

- 2.4.2.5.2. Data Integrity

- 2.4.2.1. Types of Primary Research

- 2.4.3. Analytical Tools and Databases

- 2.4.1. Secondary Research

- 2.5. Robust Quality Control

3. MARKET DYNAMICS

- 3.1. Chapter Overview

- 3.2. Forecast Methodology

- 3.2.1. Top-down Approach

- 3.2.2. Bottom-up Approach

- 3.2.3. Hybrid Approach

- 3.3. Market Assessment Framework

- 3.3.1. Total Addressable Market (TAM)

- 3.3.2. Serviceable Addressable Market (SAM)

- 3.3.3. Serviceable Obtainable Market (SOM)

- 3.3.4. Currently Acquired Market (CAM)

- 3.4. Forecasting Tools and Techniques

- 3.4.1. Qualitative Forecasting

- 3.4.2. Correlation

- 3.4.3. Regression

- 3.4.4. Extrapolation

- 3.4.5. Convergence

- 3.4.6. Sensitivity Analysis

- 3.4.7. Scenario Planning

- 3.4.8. Data Visualization

- 3.4.9. Time Series Analysis

- 3.4.10. Forecast Error Analysis

- 3.5. Key Considerations

- 3.5.1. Demographics

- 3.5.2. Government Regulations

- 3.5.3. Reimbursement Scenarios

- 3.5.4. Market Access

- 3.5.5. Supply Chain

- 3.5.6. Industry Consolidation

- 3.5.7. Pandemic / Unforeseen Disruptions Impact

- 3.6. Limitations

4. MACRO-ECONOMIC INDICATORS

- 4.1. Chapter Overview

- 4.2. Market Dynamics

- 4.2.1. Time Period

- 4.2.1.1. Historical Trends

- 4.2.1.2. Current and Forecasted Estimates

- 4.2.2. Currency Coverage

- 4.2.2.1. Major Currencies Affecting the Market

- 4.2.2.2. Factors Affecting Currency Fluctuations on the Industry

- 4.2.2.3. Impact of Currency Fluctuations on the Industry

- 4.2.3. Foreign Currency Exchange Rate

- 4.2.3.1. Impact of Foreign Exchange Rate Volatility on the Market

- 4.2.3.2. Strategies for Mitigating Foreign Exchange Risk

- 4.2.4. Recession

- 4.2.4.1. Assessment of Current Economic Conditions and Potential Impact on the Market

- 4.2.4.2. Historical Analysis of Past Recessions and Lessons Learnt

- 4.2.5. Inflation

- 4.2.5.1. Measurement and Analysis of Inflationary Pressures in the Economy

- 4.2.5.2. Potential Impact of Inflation on the Market Evolution

- 4.2.6. Interest Rates

- 4.2.6.1. Interest Rates and Their Impact on the Market

- 4.2.6.2. Strategies for Managing Interest Rate Risk

- 4.2.7. Commodity Flow Analysis

- 4.2.7.1. Type of Commodity

- 4.2.7.2. Origins and Destinations

- 4.2.7.3. Value and Weights

- 4.2.7.4. Modes of Transportation

- 4.2.8. Global Trade Dynamics

- 4.2.8.1. Import Scenario

- 4.2.8.2. Export Scenario

- 4.2.8.3. Trade Policies

- 4.2.8.4. Strategies for Mitigating the Risks Associated with Trade Barriers

- 4.2.8.5. Impact of Trade Barriers on the Market

- 4.2.9. War Impact Analysis

- 4.2.9.1. Russian-Ukraine War

- 4.2.9.2. Israel-Hamas War

- 4.2.10. COVID Impact / Related Factors

- 4.2.10.1. Global Economic Impact

- 4.2.10.2. Industry-specific Impact

- 4.2.10.3. Government Response and Stimulus Measures

- 4.2.10.4. Future Outlook and Adaptation Strategies

- 4.2.11. Other Indicators

- 4.2.11.1. Fiscal Policy

- 4.2.11.2. Consumer Spending

- 4.2.11.3. Gross Domestic Product (GDP)

- 4.2.11.4. Employment

- 4.2.11.5. Taxes

- 4.2.11.6. Stock Market Performance

- 4.2.11.7. Cross-Border Dynamics

- 4.2.1. Time Period

- 4.3. Conclusion

5. EXECUTIVE SUMMARY

6. INTRODUCTION

- 6.1. Chapter Overview

- 6.2. Medical Devices: An Overview

- 6.2.1. History of Medical Devices

- 6.2.2. Classification of Medical Devices

- 6.3. Medical Device Manufacturing

- 6.3.1. Challenges Associated with Medical Device Manufacturing

- 6.3.2. Role of CMOs in Medical Device Manufacturing

- 6.3.3. Role of Automation in Medical Device Manufacturing Process

- 6.4. Historical Timeline for Medical Device CMOs

- 6.5. Services Offered by Medical Device CMOs

- 6.6. Advantages Offered by Medical Device CMOs

- 6.7. Risks associated with Outsourcing to CMOs

- 6.8. Key Considerations

- 6.9. Concluding Remarks

7. REGULATORY LANDSCAPE FOR MEDICAL DEVICES

- 7.1. Chapter Overview

- 7.2. General Regulatory Guidelines for Medical Devices

- 7.3. Regulatory Landscape in Asia-Pacific

- 7.3.1. Regulatory Authority

- 7.3.2. Review / Approval Process

- 7.4. Conclusion

8. MARKET OVERVIEW

- 8.1. Chapter Overview

- 8.2. Medical Device CMOs Offering Services for Medical Devices

- 8.2.1. Analysis by Year of Establishment

- 8.2.2. Analysis by Size of Employee Base

- 8.2.3. Analysis by Location of Headquarters

- 8.2.4. Analysis by Location of Manufacturing Facility

- 8.2.5. Analysis by Regulatory Certifications / Accreditations

- 8.2.6. Analysis by Production Services Offered

- 8.2.7. Analysis by Post-production Services Offered

- 8.2.8. Analysis by Other Services Offered

- 8.2.9. Analysis by Device Class

- 8.2.10. Analysis by Type of Material(s) Handled

- 8.2.11. Analysis by Scale of Operation

- 8.2.12. Leading Players

9. COMPANY PROFILES: AUSTRALIA MEDICAL DEVICE CONTRACT MANUFACTURING MARKET

- 9.1. Chapter Overview

- 9.2. Cochlear

- 9.2.1. Company Overview

- 9.2.2. Product Portfolio

- 9.2.3. Financial Information

- 9.2.4. Recent Developments and Future Outlook

- 9.3. CSL

- 9.4. Fisher & Paykel Healthcare

- 9.5. Freudenberg Medical

- 9.6. Johnson & Johnson

- 9.7. Medtronic

- 9.8. Nanosonics

- 9.9. Osmosis Medical

- 9.10. ResMed

10. CLINICAL TRIAL ANALYSIS

- 10.1. Chapter Overview

- 10.2. Analysis of Clinical Trials

- 10.2.1. Analysis by Trial Start Year

- 10.2.2. Analysis by Trial Status

- 10.2.3. Analysis by Phase of Development

- 10.2.4. Analysis by Target Indication

- 10.2.5. Analysis by Type of Sponsor

- 10.2.6. Analysis by Geography

- 10.2.7. Analysis by Trial Start Year and Geography

- 10.3. Analysis of Enrolled Patient Population

- 10.3.1. Analysis by Trial Status

- 10.3.2. Analysis by Phase of Development

- 10.3.3. Analysis by Geography

- 10.4. Analysis of Focus Therapeutic Areas

- 10.4.1. Analysis by Type of Sponsor

- 10.4.2. Analysis by Geography

11. MERGERS AND ACQUISITIONS

- 11.1. Chapter Overview

- 11.2. Merger and Acquisition Models

- 11.3. Medical Device Contract Manufacturing: Mergers and Acquisitions

- 11.3.1. Analysis by Year of Mergers and Acquisitions

- 11.3.2. Analysis by Type of Acquisition

- 11.3.3. Most Active Acquirers: Analysis by Number of Acquisitions

- 11.3.4. Analysis by Key Value Drivers

12. MARKET IMPACT ANALYSIS

- 12.1. Chapter Overview

- 12.2. Market Drivers

- 12.3. Market Restraints

- 12.4. Market Opportunities

- 12.5. Market Challenges

- 12.6. Conclusion

13. AUSTRALIA MEDICAL DEVICE CONTRACT MANUFACTURING MARKET

- 13.1. Chapter Overview

- 13.2. Key Assumptions and Methodology

- 13.3. Australia Medical Device Contract Manufacturing Market, (Since 2023) and Forecasted Estimates (Till 2035)

- 13.4. Roots Analysis Perspective on Market Growth

- 13.5 Scenario Analysis

- 13.5.1. Conservative Scenario

- 13.5.2. Optimistic Scenario

- 13.6. Key Market Segmentations

14. MEDICAL DEVICE CONTRACT MANUFACTURING MARKET IN AUSTRALIA, BY APPLICATION AREA

- 14.1. Chapter Overview

- 14.2. Key Assumptions and Methodology

- 14.3. Medical Device Contract Manufacturing Market in Australia: Distribution by Application Area

- 14.3.1. Medical Device Contract Manufacturing Market in Australia for Therapeutic Devices: Historical Trends (Since 2023) and Forecasted Estimates (Since 2023) and Forecasted Estimates (Till 2035)

- 14.3.2. Medical Device Contract Manufacturing Market in Australia for Diagnostic Devices, Historical Trends (Since 2023) and Forecasted Estimates (Since 2023) and Forecasted Estimates (Till 2035)

- 14.3.3. Medical Device Contract Manufacturing Market in Australia for Drug Delivery Devices, Historical Trends (Since 2023) and Forecasted Estimates (Since 2023) and Forecasted Estimates (Till 2035)

- 14.3.4. Medical Device Contract Manufacturing Market in Australia for Other Devices, Historical Trends (Since 2023) and Forecasted Estimates (Since 2023) and Forecasted Estimates (Till 2035)

- 14.4. Data Triangulation and Validation

15. MEDICAL DEVICE CONTRACT MANUFACTURING MARKET IN AUSTRALIA, BY DEVICE CLASS

- 15.1. Chapter Overview

- 15.2. Key Assumptions and Methodology

- 15.3. Medical Device Contract Manufacturing Market in Australia: Distribution by Device Class

- 15.3.1. Medical Device Contract Manufacturing Market in Australia for Class I Devices, Historical Trends (Since 2023) and Forecasted Estimates (Since 2023) and Forecasted Estimates (Till 2035)

- 15.3.2. Medical Device Contract Manufacturing Market in Australia for Class II Devices Historical Trends (Since 2023) and Forecasted Estimates (Since 2023) and Forecasted Estimates (Till 2035)

- 15.3.3. Medical Device Contract Manufacturing Market in Australia for Class III Devices, Historical Trends (Since 2023) and Forecasted Estimates (Since 2023) and

- 15.4. Data Triangulation and Validation

16. MEDICAL DEVICE CONTRACT MANUFACTURING MARKET IN AUSTRALIA, BY THERAPEUTIC AREA

- 16.1. Chapter Overview

- 16.2. Key Assumptions and Methodology

- 16.3. Medical Device Contract Manufacturing Market in Australia: Distribution by Therapeutic Area

- 16.3.1. Medical Device Contract Manufacturing Market in Australia for Cardiovascular Disorders, Historical Trends (Since 2023) and Forecasted Estimates (Since 2023) and Forecasted Estimates (Till 2035)

- 16.3.2. Medical Device Contract Manufacturing Market in Australia for CNS Disorders, (Since 2023) and Forecasted Estimates (Till 2035)

- 16.3.3. Medical Device Contract Manufacturing Market in Australia for Metabolic Disorders, (Since 2023) and Forecasted Estimates (Till 2035)

- 16.3.4. Medical Device Contract Manufacturing Market in Australia for Oncological Disorders, (Since 2023) and Forecasted Estimates (Till 2035)

- 16.3.5. Medical Device Contract Manufacturing Market in Australia for Orthopedic Disorders, (Since 2023) and Forecasted Estimates (Till 2035)

- 16.3.6. Medical Device Contract Manufacturing Market in Australia for Ophthalmic Disorders, (Since 2023) and Forecasted Estimates (Till 2035)

- 16.3.7. Medical Device Contract Manufacturing Market in Australia for Pain Disorders, (Since 2023) and Forecasted Estimates (Till 2035)

- 16.3.8. Medical Device Contract Manufacturing Market in Australia for Respiratory Disorders (Since 2023) and Forecasted Estimates (Till 2035)

- 16.3.9. Medical Device Contract Manufacturing Market in Australia for Other Therapeutic Areas, (Since 2023) and Forecasted Estimates (Till 2035)

- 16.4. Data Triangulation and Validation

17. CONCLUDING REMARKS

18. APPENDIX I: TABULATED DATA

19. APPENDIX II: LIST OF COMPANIES AND ORGANIZATIONS