PUBLISHER: Roots Analysis | PRODUCT CODE: 2005199

PUBLISHER: Roots Analysis | PRODUCT CODE: 2005199

Middle East & Africa Pharmaceutical Contract Manufacturing Market: Trends and Forecast Till 2035 - Distribution by Type of Product Manufactured, API, FDF, Dosage Form, Oral Solid, End User, and Key Players

Middle East and Africa Pharmaceutical Contract Manufacturing market: Overview

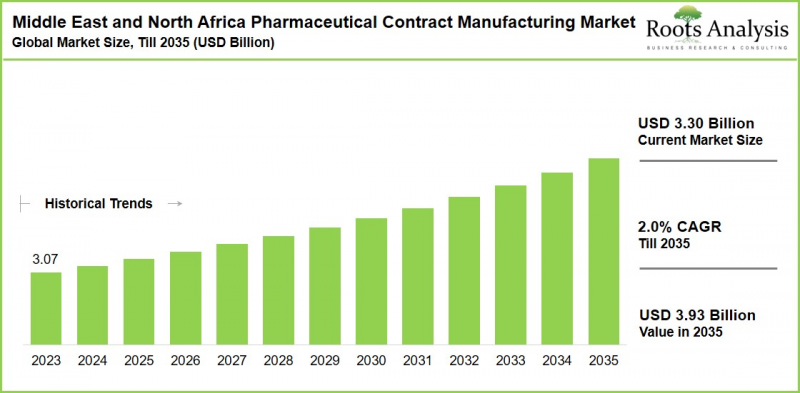

As per Roots Analysis, the Middle East and Africa Pharmaceutical Contract Manufacturing Market is estimated to grow from USD 3.30 billion in the current year to USD 3.93 billion by 2035 at a CAGR of 2.0% during the forecast period, till 2035.

Middle east and Africa Pharmaceutical Contract Manufacturing market: Growth and Trends

The rise of new therapeutic approaches has added complexity to pharmaceutical development and manufacturing, making it difficult for many firms to handle these operations without external expertise. As a result, pharmaceutical companies face numerous challenges when trying to manage their development and manufacturing processes independently. This has led many small and large pharmaceutical businesses to turn to contract manufacturing organizations (CMOs) and contract development and manufacturing organizations (CDMOs) for outsourcing their manufacturing tasks. Moreover, outsourcing allows developers to tap into specialized knowledge, enhance production processes, maintain regulatory compliance, and ensure consistent product quality. To navigate these evolving dynamics and meet the demands of a rapidly changing industry, the need for customized, advanced contract manufacturing solutions is projected to grow during the forecast period.

The growth of the Middle East and North Africa pharmaceutical contract manufacturing market is fueled by the rising healthcare spending, chronic disease prevalence, government localization initiatives and outsourcing trends to cut costs and build supply chain resilience. In addition, biopharma / biologics and cell / gene therapies are emerging, supported by regional investments in advanced manufacturing like continuous processes. MENA's strategic position as a trade hub linking Asia, Europe, and Africa significantly boosts export potential. Overall, this continuous development indicates that the market for pharmaceutical contract manufacturing to be viable for an extended period, presenting unique opportunities for industry participants in terms of strategic efforts and product innovation.

Growth Drivers: Strategic Enablers of Market Expansion

The MENA pharmaceutical contract manufacturing market is driven by rising healthcare demands, fueled by increasing prevalence of chronic diseases like cancer and the need for advanced therapies. This has encouraged pharmaceutical companies to outsource the production of pharmaceuticals for efficiency and scalability. Further, government initiatives across key markets such as Saudi Arabia, UAE, and Egypt promote localization of manufacturing through incentives, infrastructure investments, and policies reducing import dependency, creating a favorable environment for CDMOs. Cost-effectiveness is crucial since outsourcing reduces labor, operating costs, and equipment capital requirements, enabling businesses to concentrate on R&D and optimize supply chains while utilizing the strategic placement of regional hubs. AI, machine learning, and automation are examples of technological developments that further speed up the mass production of complicated medications like biologics, allowing for quicker market entry and increased competitiveness.

Market Challenges: Critical Barriers Impeding Progress

Despite the abovementioned drivers, the market encounters notable restraints that hinder market growth. Regulatory complexities and inconsistencies across MENA countries lead to prolonged approval processes, diverse quality standards, and compliance burdens, often delaying product launches and increasing operational costs. Intellectual property risks and the potential leakage of confidential information deter outsourcing, as companies fear competitive disadvantages in a region with varying IP protections. Further, infrastructure limitations, particularly in North Africa and rural areas, coupled with shortages of skilled workforce and technical expertise, hinder advanced manufacturing capabilities and supply chain reliability. Additionally, many pharmaceutical firms are establishing in-house facilities to gain control and cut long-term costs, reducing reliance on contract manufacturers amid digitalization and personalized medicine trends. Logistical challenges like inadequate transport networks and economic/political volatility in some areas further complicate operations.

Manufacturing of Low Potent APIs is Most Widely Outsourced to Contract Manufacturing Organizations

Currently, low potent API holds majority of the overall market share. This is primarily because of their scalability for bulk production in generics and high-volume drugs like those for diabetes and infections. Further, pharmaceutical companies use these APIs for the treatment of various diseases, such as diabetes and infectious diseases. This widespread use of low potent APIs drives consistently high global demand and the segment is anticipated to grow at a relatively faster pace.

Oral Solid Dosage Forms Lead the Pharmaceutical Contract Manufacturing Industry with Unparalleled Demand

According to the MENA pharma contract manufacturing market forecast, the oral solid dosage manufacturing segment accounts for majority of the overall market revenue. This is due to their affordability, patient convenience, and efficiency in large-scale production. In future, the liquids segment is likely to show higher pharmaceutical contract manufacturing market growth during the forecast period.

Middle east and Africa Pharmaceutical Contract Manufacturing market: Key Segments

Type of Product

- API & Intermediates

- FDF

By Type of API

- Originator APIs

- Generic APIs

By API Potency

- Low Potent API

- High Potent API

By Type of FDF

- Originator FDF

- Generic FDF

By Dosage Form

- Oral Solids

- Liquids

- Emulsions

- Other Dosage Forms

By Type of Packaging Offered

- Bottles

- Blister Packs

- Vials

- Prefilled Syringes

- Cartridges

- Ampoules

- Oral Liquid Bottles

- Others

By Scale of Operation

- Clinical

- Commercial

By End User

- Small

- Mid-sized

- Large and Very Large

Example Players in Middle East and North Africa Pharmaceutical Contract Manufacturing Market

- Al Haramain Pharmaceutical

- Aster DM Healthcare

- Catalent

- Dar Aldawa

- EIPICO

- Hikma Pharmaceuticals

- IQVIA

- Recipharm

- Syngene

- Tabuk Pharmaceuticals

- Thermo Fisher Scientific

Key Questions Answered in this Report

- How many MENA pharmaceutical contract manufacturers are currently engaged in this market?

- Which are the leading companies in this market?

- Which country dominates the MENA pharmaceutical contract manufacturing market?

- What are the key trends observed in the MENA pharmaceutical contract manufacturing market?

- What factors are likely to influence the evolution of this market?

- What are the primary challenges faced by pharmaceutical contract manufacturers in MENA?

- What is the current and future MENA Middle East and North Africa Pharmaceutical Contract Manufacturing Market size?

- What is the CAGR of MENA pharmaceutical contract manufacturing market?

- How is the current and future market opportunity likely to be distributed across key market segments?

Reasons to Buy this Report

- The report provides a comprehensive market analysis, offering detailed revenue projections of the overall market and its specific sub-segments. This information is valuable to both established market leaders and emerging entrants.

- The report offers stakeholders a comprehensive overview of the market, including key drivers, barriers, opportunities, and challenges. This information empowers stakeholders to stay abreast of market trends and make data-driven decisions to capitalize on growth prospects.

- The report can aid businesses in identifying future opportunities in any sector. It also helps in understanding if those opportunities are worth pursuing.

- The report helps in identifying customer demand by understanding the needs, preferences, and behavior of the target audience in order to tailor products or services effectively.

- The report equips new entrants with requisite information regarding a particular market to help them build successful business strategies.

- The report allows for more effective communication with the audience and in building strong business relations.

Complementary Benefits

- Complimentary PPT Insights Packs

- Complimentary Excel Data Packs for all Analytical Modules in the Report

- 15% Free Content Customization

- Detailed Report Walkthrough Session with Research Team

- Free Updated report if the report is 6-12 months old or older

TABLE OF CONTENTS

1. PREFACE

- 1.1. Introduction

- 1.2. Market Share Insights

- 1.3. Key Market Insights

- 1.4. Report Coverage

- 1.5. Key Questions Answered

- 1.6. Chapter Outlines

2. RESEARCH METHODOLOGY

- 2.1. Chapter Overview

- 2.2. Research Assumptions

- 2.2.1. Market Landscape and Market Trends

- 2.2.2. Market Forecast and Opportunity Analysis

- 2.2.3. Comparative Analysis

- 2.3. Database Building

- 2.3.1. Data Collection

- 2.3.2. Data Validation

- 2.3.3. Data Analysis

- 2.4. Project Methodology

- 2.4.1. Secondary Research

- 2.4.1.1. Annual Reports

- 2.4.1.2. Academic Research Papers

- 2.4.1.3. Company Websites

- 2.4.1.4. Investor Presentations

- 2.4.1.5. Regulatory Filings

- 2.4.1.6. White Papers

- 2.4.1.7. Industry Publications

- 2.4.1.8. Conferences and Seminars

- 2.4.1.9. Government Portals

- 2.4.1.10. Media and Press Releases

- 2.4.1.11. Newsletters

- 2.4.1.12. Industry Databases

- 2.4.1.13. Roots Proprietary Databases

- 2.4.1.14. Paid Databases and Sources

- 2.4.1.15. Social Media Portals

- 2.4.1.16. Other Secondary Sources

- 2.4.2. Primary Research

- 2.4.2.1. Types of Primary Research

- 2.4.2.1.1. Qualitative Research

- 2.4.2.1.2. Quantitative Research

- 2.4.2.1.3. Hybrid Approach

- 2.4.2.2. Advantages of Primary Research

- 2.4.2.3. Techniques for Primary Research

- 2.4.2.3.1. Interviews

- 2.4.2.3.2. Surveys

- 2.4.2.3.3. Focus Groups

- 2.4.2.3.4. Observational Research

- 2.4.2.3.5. Social Media Interactions

- 2.4.2.4. Key Opinion Leaders Considered in Primary Research

- 2.4.2.4.1. Company Executives (CXOs)

- 2.4.2.4.2. Board of Directors

- 2.4.2.4.3. Company Presidents and Vice Presidents

- 2.4.2.4.4. Research and Development Heads

- 2.4.2.4.5. Technical Experts

- 2.4.2.4.6. Subject Matter Experts

- 2.4.2.4.7. Scientists

- 2.4.2.4.8. Doctors and Other Healthcare Providers

- 2.4.2.5. Ethics and Integrity

- 2.4.2.5.1. Research Ethics

- 2.4.2.5.2. Data Integrity

- 2.4.2.1. Types of Primary Research

- 2.4.3. Analytical Tools and Databases

- 2.4.1. Secondary Research

- 2.5. Robust Quality Control

3. MARKET DYNAMICS

- 3.1. Chapter Overview

- 3.2. Forecast Methodology

- 3.2.1. Top-down Approach

- 3.2.2. Bottom-up Approach

- 3.2.3. Hybrid Approach

- 3.3. Market Assessment Framework

- 3.3.1. Total Addressable Market (TAM)

- 3.3.2. Serviceable Addressable Market (SAM)

- 3.3.3. Serviceable Obtainable Market (SOM)

- 3.3.4. Currently Acquired Market (CAM)

- 3.4. Forecasting Tools and Techniques

- 3.4.1. Qualitative Forecasting

- 3.4.2. Correlation

- 3.4.3. Regression

- 3.4.4. Extrapolation

- 3.4.5. Convergence

- 3.4.6. Sensitivity Analysis

- 3.4.7. Scenario Planning

- 3.4.8. Data Visualization

- 3.4.9. Time Series Analysis

- 3.4.10. Forecast Error Analysis

- 3.5. Key Considerations

- 3.5.1. Demographics

- 3.5.2. Government Regulations

- 3.5.3. Reimbursement Scenarios

- 3.5.4. Market Access

- 3.5.5. Supply Chain

- 3.5.6. Industry Consolidation

- 3.5.7. Pandemic / Unforeseen Disruptions Impact

- 3.6. Limitations

4. MACRO-ECONOMIC INDICATORS

- 4.1. Chapter Overview

- 4.2. Market Dynamics

- 4.2.1. Time Period

- 4.2.1.1. Historical Trends

- 4.2.1.2. Current and Forecasted Estimates

- 4.2.2. Currency Coverage

- 4.2.2.1. Major Currencies Affecting the Market

- 4.2.2.2. Factors Affecting Currency Fluctuations on the Industry

- 4.2.2.3. Impact of Currency Fluctuations on the Industry

- 4.2.3. Foreign Currency Exchange Rate

- 4.2.3.1. Impact of Foreign Exchange Rate Volatility on the Market

- 4.2.3.2. Strategies for Mitigating Foreign Exchange Risk

- 4.2.4. Recession

- 4.2.4.1. Assessment of Current Economic Conditions and Potential Impact on the Market

- 4.2.4.2. Historical Analysis of Past Recessions and Lessons Learnt

- 4.2.5. Inflation

- 4.2.5.1. Measurement and Analysis of Inflationary Pressures in the Economy

- 4.2.5.2. Potential Impact of Inflation on the Market Evolution

- 4.2.6. Interest Rates

- 4.2.6.1. Interest Rates and Their Impact on the Market

- 4.2.6.2. Strategies for Managing Interest Rate Risk

- 4.2.7. Commodity Flow Analysis

- 4.2.7.1. Type of Commodity

- 4.2.7.2. Origins and Destinations

- 4.2.7.3. Value and Weights

- 4.2.7.4. Modes of Transportation

- 4.2.8. Global Trade Dynamics

- 4.2.8.1. Import Scenario

- 4.2.8.2. Export Scenario

- 4.2.8.3. Trade Policies

- 4.2.8.4. Strategies for Mitigating the Risks Associated with Trade Barriers

- 4.2.8.5. Impact of Trade Barriers on the Market

- 4.2.9. War Impact Analysis

- 4.2.9.1. Russian-Ukraine War

- 4.2.9.2. Israel-Hamas War

- 4.2.10. COVID Impact / Related Factors

- 4.2.10.1. Global Economic Impact

- 4.2.10.2. Industry-specific Impact

- 4.2.10.3. Government Response and Stimulus Measures

- 4.2.10.4. Future Outlook and Adaptation Strategies

- 4.2.11. Other Indicators

- 4.2.11.1. Fiscal Policy

- 4.2.11.2. Consumer Spending

- 4.2.11.3. Gross Domestic Product (GDP)

- 4.2.11.4. Employment

- 4.2.11.5. Taxes

- 4.2.11.6. Stock Market Performance

- 4.2.11.7. Cross-Border Dynamics

- 4.2.1. Time Period

- 4.3. Conclusion

5. EXECUTIVE SUMMARY

6. INTRODUCTION

- 6.1. Chapter Overview

- 6.2. Type of Third-party Manufacturers

- 6.3. Overview of Pharmaceutical Contract Manufacturing

- 6.4. Evolution of Pharmaceutical Contract Manufacturing

- 6.4.1. Traditional Pharmaceutical Contract Manufacturing Organizations

- 6.4.2. Modern Pharmaceutical Contract Manufacturing Organizations

- 6.5. Need for Outsourcing in the Pharmaceutical Industry

- 6.6. Recent Developments in the Pharmaceutical Contract Manufacturing Industry

- 6.6.1. Integration of Artificial Intelligence

- 6.6.2. Strategic Partnerships and Collaborations

- 6.6.2.1. Strategic Long-Term Alliance

- 6.6.2.2. Flexible Short-Term Partnership Agreements

- 6.6.3. Integrated End-to-End Business Model

- 6.6.4. Dependence on Software Service Providers

- 6.7. Services Offered by Contract Manufacturing Organizations

- 6.8. Key Considerations while Selecting a Contract Manufacturing Organization

- 6.9. Risks and Challenges Associated with Outsourcing Pharmaceutical Manufacturing Operations

- 6.10. Future Perspectives

7. MARKET LANDSCAPE

- 7.1. Chapter Overview

- 7.2. Pharmaceutical Contract Manufacturing Organizations: Overall Market Landscape

- 7.2.1. Analysis by Year of Establishment

- 7.2.2. Analysis by Company Size

- 7.2.3. Analysis by Location of Headquarters (Region)

- 7.2.4. Analysis by Location of Headquarters (Country)

- 7.2.5. Analysis by Location of Manufacturing Facility (Region)

- 7.2.6. Analysis by Type of Offering

- 7.2.7. Analysis by Type of Pharmaceutical Product Manufactured

- 7.2.8. Analysis by Scale of Operation

- 7.2.9. Analysis by Type of Service Offered

- 7.2.10. Analysis by Finished Dosage Form Manufactured

- 7.2.11. Analysis by Type of Packaging Offered

8. COMPANY PROFILES: MIDDLE EAST AND NORTH AFRICA PHARMACEUTICAL CONTRACT MANUFACTURING MARKET

- 8.1. Chapter Overview

- 8.2. Al Haramain Pharmaceutical

- 8.2.1. Company Overview

- 8.2.2. Product Portfolio

- 8.2.3. Financial Information

- 8.2.4. Recent Developments and Future Outlook

- 8.3. Aster DM Healthcare

- 8.4. Catalent

- 8.5. Dar Aldawa

- 8.6. EIPICO

- 8.7. Hikma Pharmaceuticals

- 8.8. IQVIA

- 8.9. Recipharm

- 8.10. Syngene

- 8.11. Tabuk Pharmaceuticals

- 8.12. Thermo Fisher Scientific

9. CAPACITY ANALYSIS

- 9.1. Chapter Overview

- 9.2. Key Assumptions and Methodology

- 9.3. Pharmaceutical Contract Manufacturing: Global Production Capacity

- 9.3.1. Analysis by Company Size

- 9.3.2. Analysis by Scale of Operation

- 9.3.3. Analysis by Location of Manufacturing Facility

- 9.3.3.1. Pharmaceutical Contract Manufacturing Capacity in North America

- 9.3.3.2. Pharmaceutical Contract Manufacturing Capacity in Europe

- 9.3.3.3. Pharmaceutical Contract Manufacturing Capacity in Asia-Pacific

- 9.4. Concluding Remarks

10. DEMAND ANALYSIS

- 10.1. Chapter Overview

- 10.2. Key Assumptions and Methodology

- 10.3. Global Demand for Pharmaceutical Contract Manufacturing

- 10.3.1. Demand for Pharmaceutical Contract Manufacturing: Analysis by Scale of Operation

- 10.3.2. Demand for Pharmaceutical Contract Manufacturing: Analysis by Type of API

- 10.3.3. Demand for Pharmaceutical Contract Manufacturing: Analysis by Potency of API

- 10.3.4. Demand for Pharmaceutical Contract Manufacturing: Analysis by Geographical Regions

11. MARKET IMPACT ANALYSIS

- 11.1. Chapter Overview

- 11.2. Market Drivers

- 11.3. Market Restraints

- 11.4. Market Opportunities

- 11.5. Market Challenges

- 11.6. Conclusion

12. MIDDLE EAST AND NORTH AFRICA PHARMACEUTICAL CONTRACT MANUFACTURING MARKET

- 12.1. Chapter Overview

- 12.2. Key Assumptions and Methodology

- 12.3. Middle East and Africa Pharmaceutical Contract Manufacturing Market, Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 12.4. Roots Analysis Perspective on Market Growth

- 12.5 Scenario Analysis

- 12.5.1. Conservative Scenario

- 12.5.2. Optimistic Scenario

- 12.6. Key Market Segmentations

13. MIDDLE EAST AND NORTH AFRICA PHARMACEUTICAL CONTRACT MANUFACTURING MARKET, BY TYPE OF PRODUCT

- 13.3. Pharmaceutical Contract Manufacturing Market: Distribution by Type of Product Manufactured

- 13.3.1. Middle East and North Africa Pharmaceutical Contract Manufacturing Market for API and Intermediates: Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 13.3.2. Middle East and North Africa Pharmaceutical Contract Manufacturing Market for FDFs: Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 13.4. Data Triangulation and Validation

14. MIDDLE EAST AND NORTH AFRICA PHARMACEUTICAL CONTRACT MANUFACTURING MARKET, BY TYPE OF API

- 14.1. Chapter Overview

- 14.2. Key Assumptions and Methodology

- 14.3. Pharmaceutical Contract Manufacturing Market: Distribution by Type of API

- 14.3.1. Middle East and North Africa Pharmaceutical Contract Manufacturing Market for Originator APIs: Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 14.3.2. Middle East and North Africa Pharmaceutical Contract Manufacturing Market for Generic APIs: Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 14.4. Data Triangulation and Validation

15. MIDDLE EAST AND NORTH AFRICA PHARMACEUTICAL CONTRACT MANUFACTURING MARKET, BY API POTENCY

- 15.1. Chapter Overview

- 15.2. Key Assumptions and Methodology

- 15.3. Pharmaceutical Contract Manufacturing Market: Distribution by API Potency

- 15.3.1. Middle East and North Africa Pharmaceutical Contract Manufacturing Market for Low Potent APIs: Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 15.3.2. Middle East and North Africa Pharmaceutical Contract Manufacturing Market for High Potent APIs: Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 15.4. Data Triangulation and Validation

16. MIDDLE EAST AND NORTH AFRICA PHARMACEUTICAL CONTRACT MANUFACTURING MARKET, BY TYPE OF FDF

- 16.1. Chapter Overview

- 16.2. Key Assumptions and Methodology

- 16.3. Pharmaceutical Contract Manufacturing Market: Distribution by Type of FDF

- 16.3.1. Middle East and North Africa Pharmaceutical Contract Manufacturing Market for Originator FDFs: Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 16.3.2. Middle East and North Africa Pharmaceutical Contract Manufacturing Market for Generic FDFs: Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 16.4. Data Triangulation and Validation

17. MIDDLE EAST AND NORTH AFRICA PHARMACEUTICAL CONTRACT MANUFACTURING MARKET, BY DOSAGE FORM

- 17.1. Chapter Overview

- 17.2. Key Assumptions and Methodology

- 17.3. Pharmaceutical Contract Manufacturing Market: Distribution by Dosage Form

- 17.3.1. Middle East and North Africa Pharmaceutical Contract Manufacturing Market for Oral Solids: Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 17.3.2. Middle East and North Africa Pharmaceutical Contract Manufacturing Market for Liquids: Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 17.3.3. Middle East and North Africa Pharmaceutical Contract Manufacturing Market for Emulsions: Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 17.3.4. Middle East and North Africa Pharmaceutical Contract Manufacturing Market for Other Dosage Forms: Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 17.4. Data Triangulation and Validation

18. MIDDLE EAST AND NORTH AFRICA PHARMACEUTICAL CONTRACT MANUFACTURING MARKET, BY ORAL SOLIDS

- 18.1. Chapter Overview

- 18.2. Key Assumptions and Methodology

- 18.3. Pharmaceutical Contract Manufacturing Market: Distribution by Oral Solids

- 18.3.1. Middle East and North Africa Pharmaceutical Contract Manufacturing Market for Tablets: Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 18.3.2. Middle East and North Africa Pharmaceutical Contract Manufacturing Market for Capsules: Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 18.3.3. Middle East and North Africa Pharmaceutical Contract Manufacturing Market for Other Solid Doses: Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 18.4. Data Triangulation and Validation

19. MIDDLE EAST AND NORTH AFRICA PHARMACEUTICAL CONTRACT MANUFACTURING MARKET, BY TYPE OF PACKAGING OFFERED

- 19.1. Chapter Overview

- 19.2. Key Assumptions and Methodology

- 19.3. Pharmaceutical Contract Manufacturing Market: Distribution by Type of Packaging Offered

- 19.3.1. Middle East and North Africa Pharmaceutical Contract Manufacturing Market for Bottles: Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 19.3.2. Middle East and North Africa Pharmaceutical Contract Manufacturing Market for Blister Packs: Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 19.3.3. Middle East and North Africa Pharmaceutical Contract Manufacturing Market for Oral Liquid Bottles: Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 19.3.4. Middle East and North Africa Pharmaceutical Contract Manufacturing Market for Vials: Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 19.3.5. Middle East and North Africa Pharmaceutical Contract Manufacturing Market for Prefilled Syringe: Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 19.3.6. Middle East and North Africa Pharmaceutical Contract Manufacturing Market for Cartridegs: Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 19.3.7. Middle East and North Africa Pharmaceutical Contract Manufacturing Market for Ampoules: Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 19.3.8. Middle East and North Africa Pharmaceutical Contract Manufacturing Market for Other Types of Packaging: Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 19.4. Data Triangulation and Validation

20. MIDDLE EAST AND NORTH AFRICA PHARMACEUTICAL CONTRACT MANUFACTURING MARKET, BY SCALE OF OPERATION

- 20.1. Chapter Overview

- 20.2. Key Assumptions and Methodology

- 20.3. Pharmaceutical Contract Manufacturing Market: Distribution by Scale of Operation

- 20.3.1. Middle East and North Africa Pharmaceutical Contract Manufacturing Market for Clinical Scale: Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 20.3.2. Middle East and North Africa Pharmaceutical Contract Manufacturing Market for Commercial Scale: Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 20.4. Data Triangulation and Validation

21. MIDDLE EAST AND NORTH AFRICA PHARMACEUTICAL CONTRACT MANUFACTURING MARKET, BY END-USER

- 21.1. Chapter Overview

- 21.2. Key Assumptions and Methodology

- 21.3. Pharmaceutical Contract Manufacturing Market: Distribution by End-user

- 21.3.1. Middle East and North Africa Pharmaceutical Contract Manufacturing Market for Small Companies: Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 21.3.2. Middle East and North Africa Pharmaceutical Contract Manufacturing Market for Mid-sized Companies: Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 21.3.3. Middle East and North Africa Pharmaceutical Contract Manufacturing Market for Large and Very Large Companies: Historical Trends (Since 2022) and Forecasted Estimates (Till 2035)

- 21.4. Data Triangulation and Validation

22. CONCLUDING REMARKS

23. APPENDIX I: TABULATED DATA

24. APPENDIX II: LIST OF COMPANIES AND ORGANIZATIONS