PUBLISHER: Roots Analysis | PRODUCT CODE: 2088573

PUBLISHER: Roots Analysis | PRODUCT CODE: 2088573

Hyperscale Data Center Market, Till 2040: Distribution by Type of Component, Type of Deployment, Data Center Size, End User, Type of Workload, Cooling Technology, Geographical Regions, and Leading Players: Industry Trends and Global Forecasts

Hyperscale Data Center Market Outlook

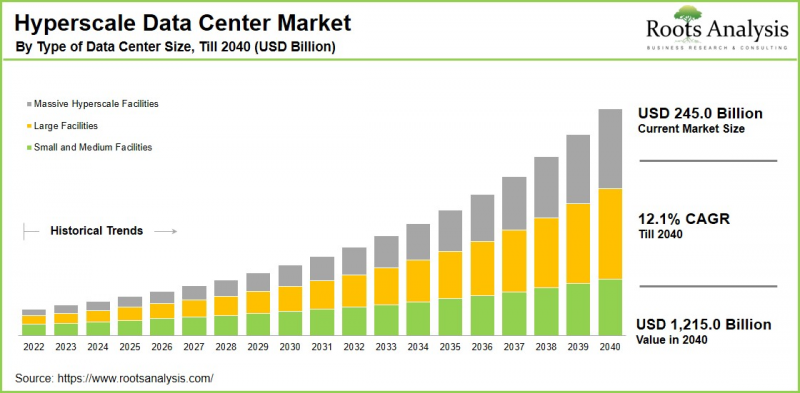

As per Roots Analysis, the global hyperscale data center market size is estimated to grow from USD 245.0 billion in the current year to USD 1,215.0 billion by 2040, at a CAGR of 12.1% during the forecast period, till 2040.

The hyperscale data center market is undergoing a significant transformation, driven by the rapid rise of artificial intelligence (AI) workloads. The focus of infrastructure development has shifted from traditional cloud capacity optimization to the expansion of power-intensive GPU clusters. This is resulting in substantial demand for advanced liquid cooling technologies, high-speed networking solutions, and large-scale gigawatt-capacity data center campuses. Major cloud service providers are accelerating investments in hyperscale infrastructure as enterprise AI adoption continues to expand alongside evolving data sovereignty requirements and increasingly stringent sustainability regulations. These factors are driving greater complexity in regional deployment strategies and infrastructure planning. Strategic developments within the industry further underscore this momentum; for instance, Alphabet's acquisition of renewable energy developer Intersect in December 2025 highlights the growing convergence of clean energy procurement and hyperscale data center expansion.

Some of the key takeaways from this report are highlighted below:

- Market Share by Type of Component: The IT Infrastructure segment is projected to account for 34.0% of the global hyperscale data center market in 2026, underscoring its critical role in supporting large-scale computing environments. Meanwhile, the liquid cooling systems segment is anticipated to witness the fastest growth, through 2040.

- Market Share by Type of Deployment: The cloud segment is expected to hold the largest market share of 46.0% in 2026, reflecting the continued dominance of cloud-based digital services. In contrast, the multi-cloud segment is expected to grow at a higher CAGR through 2040.

- Market Share by Data Center Size: assive hyperscale facilities are estimated to represent 49.0% of the market in 2026, highlighting the industry's preference for large-scale, centralized infrastructure; this trend is unlikely to change in future as well.

- Market Share by Type of Workload: The cloud computing segment is anticipated to capture 31.0% of the market share in 2026, maintaining its position as the primary application area for hyperscale infrastructure.

- Market Share by Geography: North America is expected to dominate the market with a 41.0% share in 2026, supported by its mature cloud ecosystem and strong technology investment landscape. Meanwhile, Asia-Pacific is projected to emerge as the fastest-growing regional market, recording a CAGR of 14.5% through 2040.

Looking ahead, the market is projected to grow at a significant pace, as AI infrastructure deployment becomes more mature and operators increasingly prioritize thermal management, energy efficiency, and multi-cloud optimization. Industry confidence in the long-term potential of hyperscale AI infrastructure is also reflected in large-scale investment activity, exemplified by the USD 40 billion acquisition of Aligned Data Centers by a consortium comprising BlackRock, Microsoft, NVIDIA, and xAI. Such developments reinforce the strategic importance of hyperscale facilities as foundational assets supporting the next generation of AI-driven digital infrastructure.

Strategic Insights For Senior Leaders

Competitive Landscape of Players in the Hyperscale Data Center Industry

The hyperscale data center market is increasingly characterized by the emergence of vertically integrated cloud and AI infrastructure ecosystems. The leading hyperscale operators maintain end-to-end control over critical components, including compute resources, networking infrastructure, AI accelerators, and software platforms.

A key factor shaping the competitive landscape is the accelerating demand for AI infrastructure, which has prompted substantial investments in capacity expansion across global markets. This trend is driving the development of AI-optimized data centers, GPU-powered cloud platforms, advanced liquid cooling solutions, and dedicated AI computing facilities across the regions. As organizations seek to support the growing computational requirements of generative AI, machine learning, and high-performance applications, hyperscale providers are strengthening their infrastructure capabilities to enhance scalability, and long-term competitive positioning.

Leading Hyperscale Data Center Companies andheir Recent Initiatives

Leading technology companies, including Amazon, Alphabet (Google), Microsoft, Meta, and Oracle, are significantly increasing capital expenditures to support the growing demand for AI computing capacity, advanced networking infrastructure, and next-generation data center facilities. Collectively, these organizations are expected to invest between USD 660 billion and USD 690 billion in capital expenditure during 2026, representing a substantial increase compared to 2025 spending levels. Some of the other initiatives are mentioned below:

- Amazon (AWS): The company has projected approximately USD 200 billion in capital expenditure for 2026, compared to approximately USD 125 billion in the previous year, highlighting its commitment to expanding AI and cloud infrastructure capabilities.

- Microsoft (Azure): Microsoft is accelerating investments in AI-native infrastructure to strengthen the capabilities of its Azure cloud platform and support growing demand for generative AI applications. The company allocated USD 80 billion in 2025 towards the development of AI-optimized data centers and the expansion of Azure's AI service portfolio.

- Alphabet (Google): Alphabet is undertaking its most ambitious AI infrastructure expansion to date as it strengthens Google Cloud's position in the rapidly evolving AI landscape. The company committed approximately USD 75 billion in capital expenditure during 2025 to support the deployment of next-generation AI-enabled data centers. Investment levels are expected to rise significantly in 2026, with projected capital expenditures ranging between USD 175 billion and USD 185 billion.

Emerging Startups in Hyperscale Data Center Market

The hyperscale data center ecosystem is experiencing a significant surge in startup activity, driven by growing investment in AI infrastructure, sustainable computing technologies, and advanced energy management solutions. Notably, among data center-focused companies that have raised more than USD 500 million, approximately 70% completed their latest equity financing rounds during 2024 or 2025

- CoreWeave: Originally established as a cryptocurrency mining company, the firm successfully transitioned into AI-focused cloud infrastructure and has rapidly scaled its operations to meet growing demand for high-performance computing resources. As of 2025, CoreWeave operates 32 data center facilities, supports a fleet of approximately 250,000 GPUs, and manages millions of square feet of computing capacity.

- Vantage Data Centers: Vantage Data Centers continues to strengthen its position as one of the largest pure-play hyperscale data center developers globally. The company secured more than USD 2 billion in Series C financing in January 2026, following an additional USD 1.6 billion equity investment in November 2025, to support the expansion of its international data center portfolio.

- Emerald AI: Emerald AI is addressing one of the most critical challenges facing the hyperscale data center industry, namely power grid capacity constraints. The company's proprietary Conductor platform leverages real-time grid intelligence to dynamically schedule, redistribute, or temporarily defer AI workloads based on energy availability and grid conditions. Following its seed funding round in 2025, Emerald AI has positioned itself at the convergence of AI infrastructure and intelligent energy management.

Potential Opportunities in the Hyperscale Data Center Market

The growing adoption of multi-cloud strategies and the emergence of sovereign AI infrastructure initiatives are creating significant opportunities for hyperscale data center expansion, strategic partnerships, and the development of specialized AI-ready facilities. As organizations increasingly seek greater flexibility, operational resilience, and compliance with evolving data sovereignty regulations, demand for infrastructure capable of supporting multiple cloud environments is rising. Consequently, the multi-cloud deployment segment is projected to grow at a CAGR of 14.7% through 2040, driven by enterprises' need to seamlessly distribute workloads across diverse cloud platforms while optimizing performance and risk management.

The expansion of regional cloud infrastructure is further accelerating this trend. In August 2025, leading hyperscale cloud providers, including AWS, Microsoft, and Google, announced and advanced multiple cloud region deployments across Asia-Pacific and Europe. These developments are expected to generate substantial opportunities for providers of networking equipment, advanced cooling technologies, power management systems, and other critical infrastructure solutions.

Why This Report Matters to Decision Makers?

The rapid expansion of AI infrastructure, sovereign cloud initiatives, and hyperscale GPU deployments is reshaping the global digital infrastructure landscape. As hyperscale data centers become increasingly critical to cloud scalability, enterprise AI adoption, and energy infrastructure planning, stakeholders require actionable intelligence to navigate a rapidly evolving market.

This report provides comprehensive insights to support infrastructure investment decisions, regional expansion strategies, technology adoption planning, and long-term growth initiatives across the hyperscale ecosystem.

- Identifying Market Gaps and Emerging Opportunities: The report highlights key infrastructure gaps across liquid cooling technologies, power availability, sovereign AI capacity, and high-density networking infrastructure. The analysis supports market entry decisions, partnerships, capacity expansion strategies, and infrastructure specialization initiatives.

- Evaluating Investment and Funding Opportunities: The study examines capital flows across hyperscale operators, AI-focused cloud providers, cooling technology developers, and renewable energy-linked infrastructure projects. Investors, private equity firms, and corporate development teams can assess high-growth segments. The report also supports acquisition screening, infrastructure financing decisions, and regional investment prioritization.

- Understanding Technology Innovation and Adoption Trends: The report assesses the adoption of emerging technologies, including direct-to-chip liquid cooling, immersion cooling, AI accelerator infrastructure, multi-cloud orchestration platforms, and advanced thermal management systems. Technology leaders can benchmark modernization initiatives against evolving workload requirements and increasing rack density demands.

- Competitive Landscape and Industry Benchmarking: The report provides an in-depth evaluation of leading hyperscale cloud providers, colocation operators, networking vendors, cooling infrastructure suppliers, and AI-native cloud platforms. Stakeholders can assess competitive positioning, regional expansion activities, ecosystem integration strategies, and AI infrastructure investments.

- Strategic Partnerships and Ecosystem Development: The study explores collaborations between hyperscale operators, semiconductor manufacturers, utility providers, cooling technology companies, and infrastructure investors. Business development teams can identify partnership opportunities that accelerate deployment timelines, improve operational efficiency, and reduce infrastructure risks.

- Market Growth Outlook and Revenue Opportunities: The report delivers detailed market forecasts, and segment-level growth projections through 2040 across deployment models, cooling technologies, workload types, end users, and geographic regions. Strategy and finance teams can identify the most attractive growth segments and prioritize investments accordingly.

Hyperscale Data Center Market: Key Market Segmentation

By Type of Component

- IT Infrastructure

- Servers

- Storage Systems

- Networking Equipment

- Power Infrastructure

- UPS Systems

- PDUs

- Generators

- Cooling Infrastructure

- Liquid Cooling Systems

- Air-Based Cooling Systems

- Construction and Facility Infrastructure

- Security and Monitoring Solutions

By Type of Deployment

- Cloud

- Colocation

- On-Premises

- Hybrid

- Multi-Cloud

By Data Center Size

- Small and Medium Facilities

- Large Facilities

- Massive Hyperscale Facilities

By End User

- Cloud Service Providers

- Colocation Providers

- Enterprises

- Government and Public Sector

- Telecommunications Providers

- Social Media and Digital Platforms

- BFSI

- Healthcare and Life Sciences

- Retail and E-commerce

By Type of Workload

- AI and Machine Learning

- Big Data Analytics

- Cloud Computing

- Content Delivery and Streaming

- Enterprise Applications

- High-Performance Computing

- IoT and Edge Processing

By Cooling Technology

- Air Cooling

- Direct-to-Chip Liquid Cooling

- Immersion Cooling

- Hybrid Cooling

- Free Cooling Systems

By Geographical Regions

- North America

- US

- Canada

- Mexico

- Rest of North America

- Europe

- Austria

- Belgium

- Denmark

- France

- Germany

- Ireland

- Italy

- Netherlands

- Norway

- Russia

- Spain

- Sweden

- Switzerland

- UK

- Rest of Europe

- Asia-Pacific

- Australia

- China

- India

- Japan

- New-Zealand

- Singapore

- South Korea

- Rest of Asia-Pacific

- Latin America

- Argentina

- Brazil

- Chile

- Colombia

- Venezuela

- Rest of Latin America

- Middle East and North Africa (MENA)

- Egypt

- Iran

- Iraq

- Israel

- Kuwait

- Saudi Arabia

- UAE

- Rest of MENA

- Rest of the World

Hyperscale Data Center Market: Modules Covered

The report on the hyperscale data center market features insights on various sections, including:

- Market Sizing and Opportunity Analysis: An in-depth analysis of the hyperscale data center market, focusing on key market segments, including [A] type of component, [B] type of deployment, [C] data center size, [D] end user, [E] type of workload, [F] cooling technology, [G] geographical regions, and [H] leading players.

- Competitive Landscape: A comprehensive analysis of the companies engaged in the hyperscale data center market, based on several relevant parameters, such as [A] year of establishment, [B] company size, [C] location of headquarters and [D] ownership structure.

- Company Profiles: Elaborate profiles of prominent players engaged in the hyperscale data center market, providing details on [A] location of headquarters, [B] company size, [C] company mission, [D] company footprint, [E] management team, [F] contact details, [G] financial information, [H] operating business segments, [I] product / technology portfolio, [J] recent developments, and an informed future outlook.

- Megatrends: An evaluation of ongoing megatrends in the hyperscale data center industry.

- Patent Analysis: An insightful analysis of patents filed / granted in the hyperscale data center domain, based on relevant parameters, including [A] type of patent, [B] patent publication year, [C] patent age and [D] leading players.

- Recent Developments: An overview of the recent developments made in the hyperscale data center market, along with analysis based on relevant parameters, including [A] year of initiative, [B] type of initiative, [C] geographical distribution and [D] most active players.

- Porter's Five Forces Analysis: An analysis of five competitive forces prevailing in the hyperscale data center market, including threats of new entrants, bargaining power of buyers, bargaining power of suppliers, threats of substitute products and rivalry among existing competitors.

- SWOT Analysis: An insightful SWOT framework, highlighting the strengths, weaknesses, opportunities and threats in the domain. Additionally, it provides Harvey ball analysis, highlighting the relative impact of each SWOT parameter.

Key Questions Answered in this Report

- What is the current and future market size?

- Who are the leading companies in this market?

- What are the growth drivers that are likely to influence the evolution of this market?

- What are the key partnership and funding trends shaping this industry?

- Which region is likely to grow at higher CAGR till 2040?

- How is the current and future market opportunity likely to be distributed across key market segments?

Additional Benefits of Buying the Report

- Complimentary Dynamic Excel Dashboards for Analytical Modules

- Exclusive 15% Free Content Customization

- Personalized Interactive Report Walkthrough with Our Expert Research Team

- Free Report Updates for Versions Older than 6-12 Months

TABLE OF CONTENTS

1. PROJECT OVERVIEW

- 1.1. Context

- 1.2. Project Objectives

2. RESEARCH METHODOLOGY

- 2.1. Chapter Overview

- 2.2. Research Assumptions

- 2.3. Database Building

- 2.3.1. Data Collection

- 2.3.2. Data Validation

- 2.3.3. Data Analysis

- 2.4. Project Methodology

- 2.4.1. Secondary Research

- 2.4.1.1. Annual Reports

- 2.4.1.2. Academic Research Papers

- 2.4.1.3. Company Websites

- 2.4.1.4. Investor Presentations

- 2.4.1.5. Regulatory Filings

- 2.4.1.6. White Papers

- 2.4.1.7. Industry Publications

- 2.4.1.8. Conferences and Seminars

- 2.4.1.9. Government Portals

- 2.4.1.10. Media and Press Releases

- 2.4.1.11. Newsletters

- 2.4.1.12. Industry Databases

- 2.4.1.13. Roots Proprietary Databases

- 2.4.1.14. Paid Databases and Sources

- 2.4.1.15. Social Media Portals

- 2.4.1.16. Other Secondary Sources

- 2.4.2. Primary Research

- 2.4.2.1. Introduction

- 2.4.2.2. Types

- 2.4.2.2.1. Qualitative

- 2.4.2.2.2. Quantitative

- 2.4.2.3. Advantages

- 2.4.2.4. Techniques

- 2.4.2.4.1. Interviews

- 2.4.2.4.2. Surveys

- 2.4.2.4.3. Focus Groups

- 2.4.2.4.4. Observational Research

- 2.4.2.4.5. Social Media Interactions

- 2.4.2.5. Stakeholders

- 2.4.2.5.1. Company Executives (CXOs)

- 2.4.2.5.2. Board of Directors

- 2.4.2.5.3. Company Presidents and Vice Presidents

- 2.4.2.5.4. Key Opinion Leaders

- 2.4.2.5.5. Research and Development Heads

- 2.4.2.5.6. Technical Experts

- 2.4.2.5.7. Subject Matter Experts

- 2.4.2.5.8. Scientists

- 2.4.2.5.9. Doctors and Other Healthcare Providers

- 2.4.2.6. Ethics and Integrity

- 2.4.2.6.1. Research Ethics

- 2.4.2.6.2. Data Integrity

- 2.4.3. Analytical Tools and Databases

- 2.4.1. Secondary Research

3. MARKET DYNAMICS

- 3.1. Forecast Methodology

- 3.1.1. Top-Down Approach

- 3.1.2. Bottom-Up Approach

- 3.1.3. Hybrid Approach

- 3.2. Market Assessment Framework

- 3.2.1. Total Addressable Market (TAM)

- 3.2.2. Serviceable Addressable Market (SAM)

- 3.2.3. Serviceable Obtainable Market (SOM)

- 3.2.4. Currently Acquired Market (CAM)

- 3.3. Forecasting Tools and Techniques

- 3.3.1. Qualitative Forecasting

- 3.3.2. Correlation

- 3.3.3. Regression

- 3.3.4. Time Series Analysis

- 3.3.5. Extrapolation

- 3.3.6. Convergence

- 3.3.7. Forecast Error Analysis

- 3.3.8. Data Visualization

- 3.3.9. Scenario Planning

- 3.3.10. Sensitivity Analysis

- 3.4. Key Considerations

- 3.4.1. Demographics

- 3.4.2. Market Access

- 3.4.3. Reimbursement Scenarios

- 3.4.4. Industry Consolidation

- 3.5. Robust Quality Control

- 3.6. Key Market Segmentations

- 3.7. Limitations

4. MACRO-ECONOMIC INDICATORS

- 4.1. Chapter Overview

- 4.2. Market Dynamics

- 4.2.1. Time Period

- 4.2.1.1. Historical Trends

- 4.2.1.2. Current and Forecasted Estimates

- 4.2.2. Currency Coverage

- 4.2.2.1. Overview of Major Currencies Affecting the Market

- 4.2.2.2. Impact of Currency Fluctuations on the Industry

- 4.2.3. Foreign Exchange Impact

- 4.2.3.1. Evaluation of Foreign Exchange Rates and Their Impact on Market

- 4.2.3.2. Strategies for Mitigating Foreign Exchange Risk

- 4.2.4. Recession

- 4.2.4.1. Historical Analysis of Past Recessions and Lessons Learnt

- 4.2.4.2. Assessment of Current Economic Conditions and Potential Impact on the Market

- 4.2.5. Inflation

- 4.2.5.1. Measurement and Analysis of Inflationary Pressures in the Economy

- 4.2.5.2. Potential Impact of Inflation on the Market Evolution

- 4.2.6. Interest Rates

- 4.2.6.1. Overview of Interest Rates and Their Impact on the Market

- 4.2.6.2. Strategies for Managing Interest Rate Risk

- 4.2.7. Commodity Flow Analysis

- 4.2.7.1. Type of Commodity

- 4.2.7.2. Origins and Destinations

- 4.2.7.3. Values and Weights

- 4.2.7.4. Modes of Transportation

- 4.2.8. Global Trade Dynamics

- 4.2.8.1. Import Scenario

- 4.2.8.2. Export Scenario

- 4.2.9. War Impact Analysis

- 4.2.9.1. Russian-Ukraine War

- 4.2.9.2. Israel-Hamas War

- 4.2.10. COVID Impact / Related Factors

- 4.2.10.1. Global Economic Impact

- 4.2.10.2. Industry-specific Impact

- 4.2.10.3. Government Response and Stimulus Measures

- 4.2.10.4. Future Outlook and Adaptation Strategies

- 4.2.11. Other Indicators

- 4.2.11.1. Fiscal Policy

- 4.2.11.2. Consumer Spending

- 4.2.11.3. Gross Domestic Product (GDP)

- 4.2.11.4. Employment

- 4.2.11.5. Taxes

- 4.2.11.6. R&D Innovation

- 4.2.11.7. Stock Market Performance

- 4.2.11.8. Supply Chain

- 4.2.11.9. Cross-Border Dynamics

- 4.2.1. Time Period

- 4.3. Concluding Remarks

5. EXECUTIVE SUMMARY

6. INTRODUCTION

- 6.1. Chapter Overview

- 6.2. Overview of Hyperscale Data Center

- 6.2.1. Type of Component

- 6.2.2. Type of Deployment

- 6.2.3. Type of Data Center Size

- 6.2.4. End User Industry

- 6.2.5. Type of Workload

- 6.2.6. Type of Cooling Technology

- 6.3. Future Perspective

7. REGULATORY SCENARIO

8. COMPREHENSIVE DATABASE OF LEADING PLAYERS

9. COMPETITIVE LANDSCAPE

- 9.1. Chapter Overview

- 9.2. Hyperscale Data Center Market: Overall Landscape

- 9.2.1. Analysis by Year of Establishment

- 9.2.2. Analysis by Company Size

- 9.2.3. Analysis by Location of Headquarters

- 9.2.4. Analysis by Type of Company

- 9.3. Key Findings

10. WHITE SPACE ANALYSIS

11. COMPANY COMPETITIVENESS ANALYSIS

12. STARTUP ECOSYSTEM ANALYSIS

- 12.1. Hyperscale Data Center Market: Startup Ecosystem Analysis

- 12.1.1. Analysis by Year of Establishment

- 12.1.2. Analysis by Company Size

- 12.1.3. Analysis by Location of Headquarters

- 12.1.4. Analysis by Ownership Type

- 12.2. Key Findings

13. COMPANY PROFILES

- 13.1. Chapter Overview

- 13.2. Amazon Web Services (AWS)

- 13.2.1. Company Overview

- 13.2.2. Company Mission

- 13.2.3. Company Footprint

- 13.2.4. Management Team

- 13.2.5. Contact Details

- 13.2.6. Financial Performance

- 13.2.7. Operating Business Segments

- 13.2.8. Service / Product Portfolio (project specific)

- 13.2.9. MOAT Analysis

- 13.2.10. Recent Developments and Future Outlook

- Similar details are presented for other companies mentioned below (based on information in the public domain)

- 13.3. AirTrunk

- 13.4. Alibaba Cloud

- 13.5. Apple

- 13.6. Baidu

- 13.7. CoreWeave

- 13.8. CyrusOne

- 13.9. Digital Realty

- 13.10. Equinix

- 13.11. Google Cloud Platform (GCP)

- 13.12. IBM Cloud

- 13.13. Iron Mountain

- 13.14. Meta

- 13.15. Microsoft (Azure)

- 13.16. NTT Global Data Centers

- 13.17. NVIDIA

- 13.18. Nxtra (by Bharti Airtel)

- 13.19. Oracle Cloud (OCI)

- 13.20. QTS (Quality Technology Services)

- 13.21. Tencent

14. MEGA TRENDS ANALYSIS

15. UNMET NEED ANALYSIS

16. PATENT ANALYSIS

17. RECENT DEVELOPMENTS

- 17.1. Chapter Overview

- 17.2. Recent Funding

- 17.3. Recent Partnerships

- 17.4. Other Recent Initiatives

18. GLOBAL HYPERSCALE DATA CENTER MARKET

- 18.1. Chapter Overview

- 18.2. Key Assumptions and Methodology

- 18.3. Trends Disruption Impacting Market

- 18.4. Demand Side Trends

- 18.5. Supply Side Trends

- 18.6. Global Hyperscale Data Center Market: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 18.7. Multivariate Scenario Analysis

- 18.7.1. Conservative Scenario

- 18.7.2. Optimistic Scenario

- 18.8. Investment Feasibility Index

- 18.9. Key Market Segmentations

19. MARKET OPPORTUNITIES BASED ON TYPE OF COMPONENT

- 19.1. Chapter Overview

- 19.2. Key Assumptions and Methodology

- 19.3. Revenue Shift Analysis

- 19.4. Market Movement Analysis

- 19.5. Penetration-Growth (P-G) Matrix

- 19.6. Hyperscale Data Center Market for IT Infrastructure: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 19.7. Hyperscale Data Center Market for Servers: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 19.8. Hyperscale Data Center Market for Storage Systems: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 19.9. Hyperscale Data Center Market for Network Equipment: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 19.10. Hyperscale Data Center Market for Power Infrastructure: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 19.11. Hyperscale Data Center Market for UPS Systems: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 19.12. Hyperscale Data Center Market for PDUs: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 19.13. Hyperscale Data Center Market for Generators: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 19.14. Hyperscale Data Center Market for UPS Systems: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 19.15. Hyperscale Data Center Market for Cooling Infrastructure: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 19.16. Hyperscale Data Center Market for Liquid Cooling Systems: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 19.17. Hyperscale Data Center Market for Air-Based Cooling Systems: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 19.18. Hyperscale Data Center Market for Construction and Facility Infrastructure: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 19.19. Hyperscale Data Center Market for Security and Monitoring Solutions: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 19.20. Data Triangulation and Validation

- 19.20.1. Secondary Sources

- 19.20.2. Primary Sources

- 19.20.3. Statistical Modeling

20. MARKET OPPORTUNITIES BASED ON TYPE OF DEPLOYMENT

- 20.1. Chapter Overview

- 20.2. Key Assumptions and Methodology

- 20.3. Revenue Shift Analysis

- 20.4. Market Movement Analysis

- 20.5. Penetration-Growth (P-G) Matrix

- 20.6. Hyperscale Data Center Market for Cloud: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 20.7. Hyperscale Data Center Market for Colocation: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 20.8. Hyperscale Data Center Market for On-Premises: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 20.9. Hyperscale Data Center Market for Hybrid: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 20.10. Hyperscale Data Center Market for Multi-Cloud: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 20.11. Data Triangulation and Validation

- 20.11.1. Secondary Sources

- 20.11.2. Primary Sources

- 20.11.3. Statistical Modeling

21. MARKET OPPORTUNITIES BASED ON DATA CENTER SIZE

- 21.1. Chapter Overview

- 21.2. Key Assumptions and Methodology

- 21.3. Revenue Shift Analysis

- 21.4. Market Movement Analysis

- 21.5. Penetration-Growth (P-G) Matrix

- 21.6. Hyperscale Data Center Market for Small and Medium Facilities: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 21.7. Hyperscale Data Center Market for Large Facilities: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 21.8. Hyperscale Data Center Market for Massive Hyperscale Facilities: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 21.9. Data Triangulation and Validation

- 21.9.1. Secondary Sources

- 21.9.2. Primary Sources

- 21.9.3. Statistical Modeling

22. MARKET OPPORTUNITIES BASED ON END USER

- 22.1. Chapter Overview

- 22.2. Key Assumptions and Methodology

- 22.3. Revenue Shift Analysis

- 22.4. Market Movement Analysis

- 22.5. Penetration-Growth (P-G) Matrix

- 22.6. Hyperscale Data Center Market for Cloud Service Providers: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 22.7. Hyperscale Data Center Market for Colocation Providers: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 22.8. Hyperscale Data Center Market for Enterprises: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 22.9. Hyperscale Data Center Market for Government and Public Sector: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 22.10. Hyperscale Data Center Market for Telecommunication Providers: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 22.11. Hyperscale Data Center Market for Social Media and Digital Platforms: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 22.12. Hyperscale Data Center Market for BFSI: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 22.13. Hyperscale Data Center Market for Healthcare and Life Sciences: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 22.14. Hyperscale Data Center Market for Retail and E-Commerce: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 22.15. Data Triangulation and Validation

- 22.15.1. Secondary Sources

- 22.15.2. Primary Sources

- 22.15.3. Statistical Modeling

23. MARKET OPPORTUNITIES BASED ON TYPE OF WORKLOAD

- 23.1. Chapter Overview

- 23.2. Key Assumptions and Methodology

- 23.3. Revenue Shift Analysis

- 23.4. Market Movement Analysis

- 23.5. Penetration-Growth (P-G) Matrix

- 23.6. Hyperscale Data Center Market for AI and Machine Learning: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 23.7. Hyperscale Data Center Market for Big Data Analytics: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 23.8. Hyperscale Data Center Market for Cloud Computing: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 23.9. Hyperscale Data Center Market for Content Delivery and Streaming: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 23.10. Hyperscale Data Center Market for Enterprise Applications: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 23.11. Hyperscale Data Center Market for High-Performance Computing: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 23.12. Hyperscale Data Center Market for IoT and Edge Processing: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 23.13. Data Triangulation and Validation

- 23.13.1. Secondary Sources

- 23.13.2. Primary Sources

- 23.13.3. Statistical Modeling

24. MARKET OPPORTUNITIES BASED ON COOLING TECHNOLOGY

- 24.1. Chapter Overview

- 24.2. Key Assumptions and Methodology

- 24.3. Revenue Shift Analysis

- 24.4. Market Movement Analysis

- 24.5. Penetration-Growth (P-G) Matrix

- 24.6. Hyperscale Data Center Market for Air Cooling: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 24.7. Hyperscale Data Center Market for Direct-to-Chip Liquid Cooling: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 24.8. Hyperscale Data Center Market for Immersion Cooling: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 24.9. Hyperscale Data Center Market for Hybrid Cooling: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 24.10. Hyperscale Data Center Market for Free Cooling Systems: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 24.11. Data Triangulation and Validation

- 24.11.1. Secondary Sources

- 24.11.2. Primary Sources

- 24.11.3. Statistical Modeling

25. MARKET OPPORTUNITIES FOR HYPERSCALE DATA CENTER IN NORTH AMERICA

- 25.1. Chapter Overview

- 25.2. Key Assumptions and Methodology

- 25.3. Revenue Shift Analysis

- 25.4. Market Movement Analysis

- 25.5. Penetration-Growth (P-G) Matrix

- 25.6. Hyperscale Data Center Market in North America: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 25.6.1. Hyperscale Data Center Market in the US: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 25.6.2. Hyperscale Data Center Market in Canada: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 25.6.3. Hyperscale Data Center Market in Mexico: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 25.6.4. Hyperscale Data Center Market in Other North American Countries: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 25.7. Data Triangulation and Validation

26. MARKET OPPORTUNITIES FOR HYPERSCALE DATA CENTER IN EUROPE

- 26.1. Chapter Overview

- 26.2. Key Assumptions and Methodology

- 26.3. Revenue Shift Analysis

- 26.4. Market Movement Analysis

- 26.5. Penetration-Growth (P-G) Matrix

- 26.6. Hyperscale Data Center Market in Europe: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 26.6.1. Hyperscale Data Center Market in Austria: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 26.6.2. Hyperscale Data Center Market in Belgium: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 26.6.3. Hyperscale Data Center Market in Denmark: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 26.6.4. Hyperscale Data Center Market in France: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 26.6.5. Hyperscale Data Center Market in Germany: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 26.6.6. Hyperscale Data Center Market in Ireland: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 26.6.7. Hyperscale Data Center Market in Italy: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 26.6.8. Hyperscale Data Center Market in the Netherlands: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 26.6.9. Hyperscale Data Center Market in Norway: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 26.6.10. Hyperscale Data Center Market in Russia: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 26.6.11. Hyperscale Data Center Market in Spain: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 26.6.12. Hyperscale Data Center Market in Sweden: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 26.6.13. Hyperscale Data Center Market in Switzerland: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 26.6.14. Hyperscale Data Center Market in the UK: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 26.6.15. Hyperscale Data Center Market in Other European Countries: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 26.7. Data Triangulation and Validation

27. MARKET OPPORTUNITIES FOR HYPERSCALE DATA CENTER IN ASIA-PACIFIC

- 27.1. Chapter Overview

- 27.2. Key Assumptions and Methodology

- 27.3. Revenue Shift Analysis

- 27.4. Market Movement Analysis

- 27.5. Penetration-Growth (P-G) Matrix

- 27.6. Hyperscale Data Center Market in Asia-Pacific: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 27.6.1. Hyperscale Data Center Market in China: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 27.6.2. Hyperscale Data Center Market in India: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 27.6.3. Hyperscale Data Center Market in Japan: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 27.6.4. Hyperscale Data Center Market in Singapore: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 27.6.5. Hyperscale Data Center Market in South Korea: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 27.6.6. Hyperscale Data Center Market in Other Asian Countries: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 27.7. Data Triangulation and Validation

28. MARKET OPPORTUNITIES FOR HYPERSCALE DATA CENTER IN LATIN AMERICA

- 28.1. Chapter Overview

- 28.2. Key Assumptions and Methodology

- 28.3. Revenue Shift Analysis

- 28.4. Market Movement Analysis

- 28.5. Penetration-Growth (P-G) Matrix

- 28.6. Hyperscale Data Center Market in Latin America: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 28.6.1. Hyperscale Data Center Market in Argentina: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 28.6.2. Hyperscale Data Center Market in Brazil: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 28.6.3. Hyperscale Data Center Market in Chile: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 28.6.4. Hyperscale Data Center Market in Colombia Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 28.6.5. Hyperscale Data Center Market in Venezuela: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 28.6.6. Hyperscale Data Center Market in Other Latin American Countries: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 28.7. Data Triangulation and Validation

29. MARKET OPPORTUNITIES FOR HYPERSCALE DATA CENTER IN MIDDLE EAST AND AFRICA (MEA)

- 29.1. Chapter Overview

- 29.2. Key Assumptions and Methodology

- 29.3. Revenue Shift Analysis

- 29.4. Market Movement Analysis

- 29.5. Penetration-Growth (P-G) Matrix

- 29.6. Hyperscale Data Center Market in Middle East and Africa (MEA): Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 29.6.1. Hyperscale Data Center Market in Egypt: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 29.6.2. Hyperscale Data Center Market in Iran: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 29.6.3. Hyperscale Data Center Market in Iraq: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 29.6.4. Hyperscale Data Center Market in Israel: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 29.6.5. Hyperscale Data Center Market in Kuwait: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 29.6.6. Hyperscale Data Center Market in Saudi Arabia: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 29.6.7. Hyperscale Data Center Market in United Arab Emirates (UAE): Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 29.6.8. Hyperscale Data Center Market in Other MEA Countries: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 29.7. Data Triangulation and Validation

30. MARKET OPPORTUNITIES FOR HYPERSCALE DATA CENTER IN REST OF THE WORLD

31. MARKET CONCENTRATION ANALYSIS: DISTRIBUTION BY LEADING PLAYERS

32. ADJACENT MARKET ANALYSIS

33. KEY WINNING STRATEGIES

34. PORTER'S FIVE FORCES ANALYSIS

35. SWOT ANALYSIS

36. VALUE CHAIN ANALYSIS

37. ROOTS STRATEGIC RECOMMENDATIONS

- 37.1. Chapter Overview

- 37.2. Key Business-related Strategies

- 37.2.1. Research & Development

- 37.2.2. Product Manufacturing

- 37.2.3. Commercialization / Go-to-Market

- 37.2.4. Sales and Marketing

- 37.3. Key Operations-related Strategies

- 37.3.1. Risk Management

- 37.3.2. Workforce

- 37.3.3. Finance

- 37.3.4. Others

38. INSIGHTS FROM PRIMARY RESEARCH

39. REPORT CONCLUSION

40. TABULATED DATA

41. LIST OF COMPANIES AND ORGANIZATIONS