PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1433846

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1433846

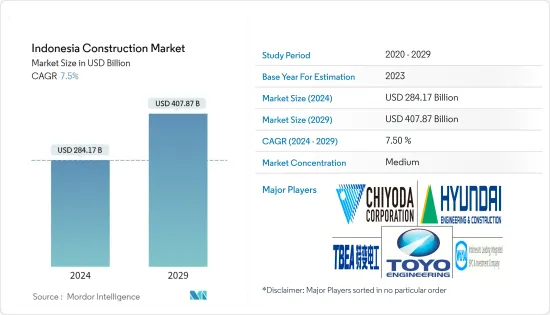

Indonesia Construction - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

The Indonesia Construction Market size is estimated at USD 284.17 billion in 2024, and is expected to reach USD 407.87 billion by 2029, growing at a CAGR of 7.5% during the forecast period (2024-2029).

While market experts continue to expect a broad recovery in Indonesia's infrastructure sector from 2022, the resurgence in COVID-19 cases in recent months and corresponding movement restrictions caused some operational disruptions. However, the impact will not be as severe as in 2020 or in some other industries, as construction was still classified as an essential activity and was allowed to continue.

Construction value for building projects is estimated to reach IDR 157.47 trillion (USD 10.97 billion) in 2022, driven by growth in the housing and industrial sectors. Trends in other categories, such as hotel, retail, and office, are starting to show positive growth compared to 2021, which may boost the construction market in the coming years.

In the residential market, the market size of apartments is expected to increase while landed houses will decrease slightly compared to 2021. Overall, the market size of landed houses is larger than apartments. The houses are dominated by the Greater Jakarta area, with suburbs in Bekasi, Bogor, and Tangerang as the dominant areas. Meanwhile, apartments will be dominated in DKI Jakarta Province. These findings indicate that landed houses continue the development trend in the suburbs, and apartments are starting to move toward recovery.

The retail category trend is expected to grow in 2022. The construction of shopping centers is expected to increase slightly. Shophouses and retail outlets may continue the upward trend in 2022. Retail is estimated to reach IDR 17.17 trillion (USD 1.19 billion) in 2022.

Office projects also show an increasing trend, although slightly. Thus, the total construction projects in 2022 are estimated to reach IDR 15.14 trillion (USD 1.05 billion). The development of data centers may increase its share significantly in 2022, i.e., IDR 4.59 trillion (USD 32.02 million) of the total value of office construction.

The industry has been impacted by delays in project implementation and the re-allocation of part of the government's budget toward COVID-19. The government re-allocated 20.4% of its 2020 budget (USD 1.7 billion) to COVID-19 relief measures.

Indonesia is the second most productive and profitable construction market in Asia, where many construction projects are underway in residential and non-residential sectors. There is a huge demand for residential properties, and the property sector is growing in major cities across the country. The public works investment is a key point in the government's plan to provide water resources, roads, and human settlement infrastructure for long-term development.

Indonesia's receptive stance toward China's Belt and Road Initiative (BRI) will be a boon to its construction industry over the next decade and help sustain the current rapid pace of development. Private and foreign capital is crucial in bridging the country's widening infrastructure gap.

Indonesia Construction Market Trends

Growing Infrastructural Development Plans

Data across the first half of 2021 showed some signs of recovery, albeit at a much lower rate than the initial expectations. There remains a mixed picture for the remainder of the year. Since its peak in July, the caseload has improved, and restrictions have started to ease in Jakarta and some parts of Java. However, cases have continued to surge outside these regions.

The government initially allocated a substantial proportion (slightly under 50%) of the 2021 budget toward infrastructure development, although it had to renegotiate and reallocate funds for healthcare. As such, projects in the pre-construction phases may come under heavy pressure, particularly state-funded projects, impacting the growth for the remaining months of the year.

Increased Involvement of SOEs

roles are awarded to established Indonesian state-owned enterprises (SOEs) and companies such as Wijaya Karya, Adhi Karya Waskita Karya, and Pembangunan Perumahan. These SOEs are involved in major infrastructure projects across the market, such as the Patimban Deep-Sea Port in West Java or works relating to the Jakarta Mass Rapid Transit System.

Under the National Medium-Term Development Plan (2020-2024 RPJMN), the government plans to invest IDR6 quadrillion (USD 412 billion) in developing transport, industrial, energy, and housing infrastructure projects by 2024. In November 2020, the government announced to provide IDR 42.38 trillion (USD 2.6 billion) for state-owned enterprises (SOEs) in 2021 to help boost their role in supporting the country's economic recovery by creating more jobs and conducting business activities.

Indonesia Construction Industry Overview

The Indonesian construction market is less competitive, with the presence of major local and international players. The Indonesian construction market presents opportunities for growth during the forecast period, which is expected to drive market competition. The market is fragmented, as many new entrants are focusing on bagging projects to strengthen their positions among top players.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS AND DYNAMICS

- 4.1 Current Economic and Construction Market Scenario

- 4.2 Technological Innovations in the Construction Sector

- 4.3 Impact of Government Regulations and Initiatives on the Industry

- 4.4 Review and Commentary on the Extent of China's Belt and Road Initiative

- 4.5 Comparison of Key Industry Metrics of Indonesia with Other ASEAN Member Countries (Analyst View)

- 4.6 Comparison of Construction Cost Metrics of Indonesia with Other ASEAN Member Countries (Analyst View)

- 4.7 Impact of COVID-19 on the market

5 MARKET DYNAMICS

- 5.1 Drivers

- 5.2 Restraints

- 5.3 Opportunities

- 5.4 Porter's Five Forces Analysis

- 5.4.1 Bargaining Power of Suppliers

- 5.4.2 Bargaining Power of Consumers/Buyers

- 5.4.3 Threat of New Entrants

- 5.4.4 Threat of Substitute Products

- 5.4.5 Intensity of Competitive Rivalry

6 MARKET SEGMENTATION (Market Size by Value)

- 6.1 By Sector

- 6.1.1 Commercial Construction

- 6.1.2 Residential Construction

- 6.1.3 Industrial Construction

- 6.1.4 Infrastructure (Transportation) Construction

- 6.1.5 Energy and Utilities Construction

7 COMPETITIVE LANDSCAPE

- 7.1 Overview (Market Concentration and Major Players)

- 7.2 Company Profiles

- 7.2.1 Chiyoda Corp.

- 7.2.2 Toyo Construction Co. Ltd

- 7.2.3 TBEA Co. Ltd

- 7.2.4 Hyundai Engineering & Construction Co. Ltd

- 7.2.5 Samsung C&T and Corporation

- 7.2.6 McConnell Dowell

- 7.2.7 Adhi Karya

- 7.2.8 PT PP (Persero)

- 7.2.9 Wijaya Karya

- 7.2.10 Waskita Karya

- 7.2.11 PT Jaya Konstruksi Manggala Pratama*

8 MAJOR INFRASTRUCTURE DEVELOPMENT PROJECTS (PROJECT DESCRIPTION, VALUE, LOCATION, SECTOR, AND CONTRACTORS)

- 8.1 Existing Infrastructure

- 8.2 Ongoing Projects

- 8.3 Upcoming Projects

9 FUTURE OF THE CONSTRUCTION SECTOR IN INDONESIA

10 APPENDIX