PUBLISHER: Aviation & Defense Market Reports (A&D) | PRODUCT CODE: 1744371

PUBLISHER: Aviation & Defense Market Reports (A&D) | PRODUCT CODE: 1744371

Global Tank Ammunition (120mm & 125mm) Market 2025-2035

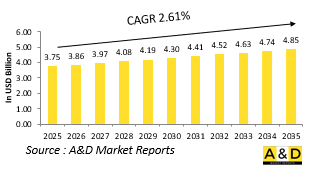

The Global Tank Ammunition (120mm & 125mm) market is estimated at USD 3.75 billion in 2025, projected to grow to USD 4.85 billion by 2035 at a Compound Annual Growth Rate (CAGR) of 2.61% over the forecast period 2025-2035.

Introduction to Tank Ammunition (120mm & 125mm) Market:

Tank ammunition in the 120mm and 125mm calibers serves as the primary armament for main battle tanks around the world. These rounds are specifically designed to defeat heavily armored threats, reinforce fire superiority, and support mechanized forces in both offensive and defensive operations. The 120mm caliber is widely used by NATO-aligned forces, while the 125mm variant is more common among countries that follow Russian or Soviet-style armor doctrines. Both calibers are tailored for high-energy delivery, offering a balance between destructive power, range, and versatility. Ammunition types include armor-piercing fin-stabilized discarding sabot (APFSDS), high-explosive anti-tank (HEAT), and multi-purpose rounds capable of engaging various battlefield targets. The global demand for such ammunition remains steady, driven by tank modernization programs, increased armored engagements, and the continued relevance of land combat vehicles in hybrid warfare. These rounds are integral not only for traditional battlefield dominance but also for maintaining deterrent capabilities in contested regions. As geopolitical dynamics shift and land warfare regains strategic prominence, 120mm and 125mm tank ammunition remain essential for maintaining tactical parity and preparing for potential high-intensity conflicts involving armored units and fortified positions.

Technology Impact in Tank Ammunition (120mm & 125mm) Market:

Recent technological advancements have significantly enhanced the performance and tactical value of 120mm and 125mm tank ammunition. One of the most notable developments is the improvement in kinetic energy penetrators, where new materials such as depleted uranium alloys and advanced tungsten composites offer greater armor-piercing efficiency. Precision engineering has also contributed to increased muzzle velocity and more consistent ballistic performance, which in turn improves accuracy and penetration at longer ranges. Smart munitions are beginning to emerge in this domain, featuring programmable fuses that allow crews to tailor explosive effects for specific mission profiles, such as airburst over infantry or delayed detonation inside structures. Additionally, fire control integration now enables ammunition to interface seamlessly with advanced targeting systems, improving first-shot lethality. The development of insensitive munitions has increased battlefield survivability by reducing the likelihood of accidental detonation under fire. Thermal and electronic shielding technologies are also being explored to counter active protection systems deployed on opposing armor platforms. The result is a new generation of tank rounds that are not only more lethal but also more adaptable and safer to use. These innovations are shaping the future of armored warfare by extending tank relevance against both conventional and asymmetric threats.

Key Drivers in Tank Ammunition (120mm & 125mm) market:

Several underlying factors are shaping the sustained importance and development of 120mm and 125mm tank ammunition across global defense sectors. Foremost among these is the modernization of armored fleets, as many nations seek to enhance their main battle tanks with more effective firepower. As newer tank designs enter service or older platforms undergo upgrades, there is a parallel demand for ammunition that matches enhanced gun systems and fire control capabilities. Evolving threat environments also necessitate greater anti-armor effectiveness, particularly against fortified vehicles equipped with reactive armor and advanced defensive measures. Urban and hybrid warfare scenarios drive interest in multi-role ammunition capable of operating effectively in complex terrains, from open battlefields to confined cityscapes. Training and readiness further contribute to demand, with militaries seeking cost-effective yet realistic practice rounds that simulate combat conditions. Industrial base concerns-such as the need to maintain domestic production capabilities or reduce reliance on foreign suppliers-also push investment in ammunition manufacturing and innovation. Moreover, as geopolitical tensions escalate in various regions, strategic stockpiling and rapid replenishment capabilities become essential. Collectively, these drivers reflect a blend of operational, strategic, and logistical considerations that make 120mm and 125mm ammunition a critical component of ground force preparedness.

Regional Trends in Tank Ammunition (120mm & 125mm) Market:

Regional defense dynamics play a major role in shaping the production, deployment, and evolution of 120mm and 125mm tank ammunition. In Europe, the resurgence of conventional deterrence and increased focus on territorial defense have prompted renewed investment in 120mm ammunition, particularly among NATO members standardizing across platforms like the Leopard and Abrams tanks. Countries in Eastern Europe, some of which still operate legacy Soviet-era tanks, continue to maintain and modernize 125mm stockpiles while integrating newer manufacturing techniques. In Asia, rising land-based tensions and border security priorities drive robust demand for both calibers, with major regional powers investing in domestic production to ensure strategic independence. The Middle East, characterized by high operational tempo and diverse armored fleets, has seen ongoing procurement of both 120mm and 125mm rounds, often tailored for combat environments involving a mix of urban and open terrain. North America emphasizes quality and innovation, focusing on advanced 120mm munitions to match the capabilities of next-generation tank platforms. Meanwhile, regions like Africa and Latin America often operate mixed fleets, balancing procurement between surplus supplies and local partnerships. Across all regions, strategic needs and battlefield experiences shape how these tank munitions are sourced, improved, and deployed.

Key Defense Tank Ammunition (120mm & 125mm) Program:

Elbit Systems Ltd. announced today that it has secured a contract valued at approximately $115 million to supply tank ammunition to a NATO member state. The contract will be executed over a three-year period, with options for extension. Elbit Systems Land's range of tank ammunition meets both NATO and MIL-STD standards and significantly enhances the firepower and operational capabilities of armored units. The 105mm ammunition series is certified for use with all NATO-standard 105mm guns, including the M68, L7, F1, and similar systems. The 120mm series is approved for NATO 120mm smoothbore guns used on platforms such as the Merkava 3 and 4, Leopard 2A4/A5/A6, M1A1/A2 Abrams, K1A1/A2, K2, ARIETE, and M60A3 tanks, and is compatible with L44/L55 smoothbore gun systems. Additionally, the 125mm ammunition is certified for use with T-72 and T-90 main battle tanks, while the 100mm series is designed for T-54, T-54B, and T-55 platforms. Elbit Systems Land emphasizes the high safety, reliability, and quality standards of its ammunition offerings.

Table of Contents

Tank Ammunition Market Report Definition

Tank Ammunition Market Segmentation

By Guidance

By Type

By Region

Tank Ammunition Market Analysis for next 10 Years

The 10-year tank ammunition market analysis would give a detailed overview of tank ammunition market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Access Control Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Access Control Market Forecast

The 10-year access control market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Access Control Market Trends & Forecast

The regional access control market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Access Control Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Access Control Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Access Control Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports

List of Tables

- Table 1: 10 Year Market Outlook, 2025-2035

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, APAC

- Table 12: Restraints, Impact Analysis, APAC

- Table 13: Challenges, Impact Analysis, APAC

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Region, 2025-2035

- Table 18: Scenario Analysis, Scenario 1, By Guidance, 2025-2035

- Table 19: Scenario Analysis, Scenario 1, By Type, 2025-2035

- Table 20: Scenario Analysis, Scenario 2, By Region, 2025-2035

- Table 21: Scenario Analysis, Scenario 2, By Guidance, 2025-2035

- Table 22: Scenario Analysis, Scenario 2, By Type, 2025-2035

List of Figures

- Figure 1: Global Tank Ammunition Market Forecast, 2025-2035

- Figure 2: Global Tank Ammunition Market Forecast, By Region, 2025-2035

- Figure 3: Global Tank Ammunition Market Forecast, By Guidance, 2025-2035

- Figure 4: Global Tank Ammunition Market Forecast, By Type, 2025-2035

- Figure 5: North America, Tank Ammunition Market, Market Forecast, 2025-2035

- Figure 6: Europe, Tank Ammunition Market, Market Forecast, 2025-2035

- Figure 7: Middle East, Tank Ammunition Market, Market Forecast, 2025-2035

- Figure 8: APAC, Tank Ammunition Market, Market Forecast, 2025-2035

- Figure 9: South America, Tank Ammunition Market, Market Forecast, 2025-2035

- Figure 10: United States, Tank Ammunition Market, Technology Maturation, 2025-2035

- Figure 11: United States, Tank Ammunition Market, Market Forecast, 2025-2035

- Figure 12: Canada, Tank Ammunition Market, Technology Maturation, 2025-2035

- Figure 13: Canada, Tank Ammunition Market, Market Forecast, 2025-2035

- Figure 14: Italy, Tank Ammunition Market, Technology Maturation, 2025-2035

- Figure 15: Italy, Tank Ammunition Market, Market Forecast, 2025-2035

- Figure 16: France, Tank Ammunition Market, Technology Maturation, 2025-2035

- Figure 17: France, Tank Ammunition Market, Market Forecast, 2025-2035

- Figure 18: Germany, Tank Ammunition Market, Technology Maturation, 2025-2035

- Figure 19: Germany, Tank Ammunition Market, Market Forecast, 2025-2035

- Figure 20: Netherlands, Tank Ammunition Market, Technology Maturation, 2025-2035

- Figure 21: Netherlands, Tank Ammunition Market, Market Forecast, 2025-2035

- Figure 22: Belgium, Tank Ammunition Market, Technology Maturation, 2025-2035

- Figure 23: Belgium, Tank Ammunition Market, Market Forecast, 2025-2035

- Figure 24: Spain, Tank Ammunition Market, Technology Maturation, 2025-2035

- Figure 25: Spain, Tank Ammunition Market, Market Forecast, 2025-2035

- Figure 26: Sweden, Tank Ammunition Market, Technology Maturation, 2025-2035

- Figure 27: Sweden, Tank Ammunition Market, Market Forecast, 2025-2035

- Figure 28: Brazil, Tank Ammunition Market, Technology Maturation, 2025-2035

- Figure 29: Brazil, Tank Ammunition Market, Market Forecast, 2025-2035

- Figure 30: Australia, Tank Ammunition Market, Technology Maturation, 2025-2035

- Figure 31: Australia, Tank Ammunition Market, Market Forecast, 2025-2035

- Figure 32: India, Tank Ammunition Market, Technology Maturation, 2025-2035

- Figure 33: India, Tank Ammunition Market, Market Forecast, 2025-2035

- Figure 34: China, Tank Ammunition Market, Technology Maturation, 2025-2035

- Figure 35: China, Tank Ammunition Market, Market Forecast, 2025-2035

- Figure 36: Saudi Arabia, Tank Ammunition Market, Technology Maturation, 2025-2035

- Figure 37: Saudi Arabia, Tank Ammunition Market, Market Forecast, 2025-2035

- Figure 38: South Korea, Tank Ammunition Market, Technology Maturation, 2025-2035

- Figure 39: South Korea, Tank Ammunition Market, Market Forecast, 2025-2035

- Figure 40: Japan, Tank Ammunition Market, Technology Maturation, 2025-2035

- Figure 41: Japan, Tank Ammunition Market, Market Forecast, 2025-2035

- Figure 42: Malaysia, Tank Ammunition Market, Technology Maturation, 2025-2035

- Figure 43: Malaysia, Tank Ammunition Market, Market Forecast, 2025-2035

- Figure 44: Singapore, Tank Ammunition Market, Technology Maturation, 2025-2035

- Figure 45: Singapore, Tank Ammunition Market, Market Forecast, 2025-2035

- Figure 46: United Kingdom, Tank Ammunition Market, Technology Maturation, 2025-2035

- Figure 47: United Kingdom, Tank Ammunition Market, Market Forecast, 2025-2035

- Figure 48: Opportunity Analysis, Tank Ammunition Market, By Region (Cumulative Market), 2025-2035

- Figure 49: Opportunity Analysis, Tank Ammunition Market, By Region (CAGR), 2025-2035

- Figure 50: Opportunity Analysis, Tank Ammunition Market, By Guidance (Cumulative Market), 2025-2035

- Figure 51: Opportunity Analysis, Tank Ammunition Market, By Guidance (CAGR), 2025-2035

- Figure 52: Opportunity Analysis, Tank Ammunition Market, By Type (Cumulative Market), 2025-2035

- Figure 53: Opportunity Analysis, Tank Ammunition Market, By Type (CAGR), 2025-2035

- Figure 54: Scenario Analysis, Tank Ammunition Market, Cumulative Market, 2025-2035

- Figure 55: Scenario Analysis, Tank Ammunition Market, Global Market, 2025-2035

- Figure 56: Scenario 1, Tank Ammunition Market, Total Market, 2025-2035

- Figure 57: Scenario 1, Tank Ammunition Market, By Region, 2025-2035

- Figure 58: Scenario 1, Tank Ammunition Market, By Guidance, 2025-2035

- Figure 59: Scenario 1, Tank Ammunition Market, By Type, 2025-2035

- Figure 60: Scenario 2, Tank Ammunition Market, Total Market, 2025-2035

- Figure 61: Scenario 2, Tank Ammunition Market, By Region, 2025-2035

- Figure 62: Scenario 2, Tank Ammunition Market, By Guidance, 2025-2035

- Figure 63: Scenario 2, Tank Ammunition Market, By Type, 2025-2035

- Figure 64: Company Benchmark, Tank Ammunition Market, 2025-2035