PUBLISHER: Aviation & Defense Market Reports (A&D) | PRODUCT CODE: 2042634

PUBLISHER: Aviation & Defense Market Reports (A&D) | PRODUCT CODE: 2042634

Global Mortar Ammunition (60mm Market & 81mm) Market 2026-2036

Global Mortar Ammunition (60mm Market & 81mm) Market

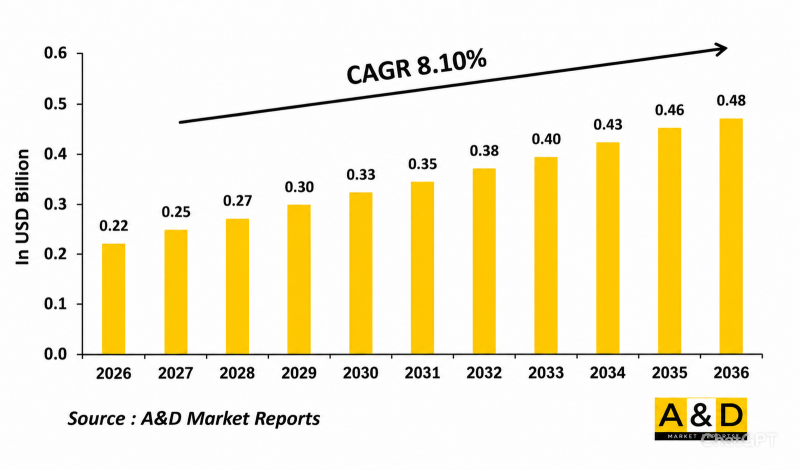

The Global Mortar Ammunition (60mm Market & 81mm) Market is estimated at USD 0.22 billion in 2026, projected to grow to USD 0.48 billion by 2036 at a Compound Annual Growth Rate (CAGR) of 8.10% over the forecast period 2026-2036.

Introduction

The global mortar ammunition market for 60mm and 81mm calibers remains an essential segment of modern infantry warfare, providing armed forces with flexible and highly mobile indirect fire support capabilities. These mortar systems are widely used by infantry battalions, rapid reaction units, special operations forces, and mechanized formations for suppressive fire, area denial, illumination, smoke deployment, and tactical battlefield support. The 60mm mortar ammunition segment is primarily valued for its lightweight portability and rapid deployment advantages, while the 81mm segment offers greater range, explosive power, and operational versatility. Growing geopolitical instability, border security concerns, and increasing military modernization initiatives are driving sustained demand for mortar ammunition worldwide. Modern defense forces continue to rely on mortar systems because of their effectiveness in diverse terrains, urban warfare operations, and expeditionary combat missions. In addition, advancements in precision-guided mortar rounds, fuse systems, and fire control technologies are enhancing the operational effectiveness and battlefield relevance of 60mm and 81mm mortar ammunition in modern combat environments.

Technology Impact in the Global Mortar Ammunition (60mm & 81mm) Market

Technological advancement is significantly transforming the global 60mm and 81mm mortar ammunition market by improving range, targeting precision, lethality, and operational efficiency. Modern mortar rounds increasingly integrate advanced fuse technologies, programmable detonation systems, and precision guidance kits that enable more accurate targeting while minimizing collateral damage. Sensor-enabled and electronically controlled fuses are enhancing operational flexibility by allowing forces to adapt detonation settings according to mission requirements and battlefield conditions.

The integration of digital fire control systems, battlefield communication networks, and drone-assisted targeting is also improving mortar effectiveness and reducing response times during combat operations. Precision-guided mortar munitions equipped with satellite navigation and laser guidance technologies are becoming increasingly important for engaging moving or concealed targets in complex environments. Additionally, advancements in propellant formulations and lightweight ammunition materials are improving firing range, portability, and storage reliability.

Smart mortar systems capable of network-centric battlefield integration are enabling faster coordination between surveillance assets, command units, and infantry formations. Enhanced manufacturing techniques and insensitive munitions technologies are also improving ammunition safety, durability, and operational readiness under extreme environmental conditions. These innovations continue to strengthen the tactical value of 60mm and 81mm mortar ammunition across modern military operations.

Key Drivers in the Global Mortar Ammunition (60mm & 81mm) Market

One of the major drivers of the global mortar ammunition market is the increasing demand for lightweight, rapidly deployable indirect fire systems capable of supporting infantry and expeditionary operations. Mortars remain highly effective due to their portability, operational simplicity, and ability to deliver immediate fire support in diverse combat environments. The 60mm mortar segment is particularly valued for mobility and close-range support, while the 81mm segment offers enhanced firepower and extended range for battalion-level operations.

Rising geopolitical tensions, regional conflicts, and border security concerns are also accelerating procurement of advanced mortar ammunition systems. Governments are modernizing infantry support capabilities to improve battlefield responsiveness, survivability, and tactical flexibility during urban warfare and asymmetric combat operations. Increasing military spending and modernization programs are further encouraging investments in precision-guided mortar munitions and advanced fire support technologies.

Another important growth factor is the growing integration of drones, surveillance systems, and digital targeting platforms into mortar operations. Modern armed forces are adopting network-enabled fire control systems that improve targeting accuracy and mission coordination. In addition, demand for precision-guided mortar rounds, extended-range ammunition, and programmable fuse technologies is rising as military forces seek improved operational efficiency and reduced collateral damage during combat missions.

The expanding focus on rapid reaction forces, special operations units, and mobile infantry formations is also supporting sustained global demand for 60mm and 81mm mortar ammunition systems.

Regional Trends in the Global Mortar Ammunition (60mm & 81mm) Market

North America remains a leading region in the global 60mm and 81mm mortar ammunition market due to strong defense spending, continuous infantry modernization initiatives, and increasing investments in precision-guided indirect fire systems. Military forces in the region are focusing on advanced mortar technologies integrated with digital fire control and network-centric warfare systems to improve battlefield effectiveness.

Europe is witnessing significant growth in mortar ammunition procurement as countries strengthen collective defense capabilities and modernize infantry support systems. NATO standardization initiatives and increasing regional security concerns are encouraging investments in interoperable mortar ammunition platforms and advanced targeting technologies.

The Asia-Pacific region is emerging as a rapidly expanding market driven by rising military expenditure, territorial disputes, and growing emphasis on rapid deployment capabilities. Countries across the region are modernizing ground forces and investing in portable indirect fire systems suitable for mountainous, jungle, and border combat operations.

The Middle East continues to experience strong demand for mortar ammunition due to ongoing regional conflicts and counter-insurgency operations. Military forces in the region increasingly rely on versatile mortar systems for urban warfare and tactical battlefield support. Meanwhile, Latin America and Africa are gradually expanding mortar procurement programs to strengthen border security, peacekeeping operations, and internal defense capabilities.

Key Programs in the Global Mortar Ammunition (60mm & 81mm) Market

Several infantry modernization and indirect fire enhancement programs are driving the growth of the global 60mm and 81mm mortar ammunition market. Governments worldwide are implementing tactical fire support initiatives focused on improving operational mobility, targeting precision, and rapid deployment capabilities for infantry and mechanized units.

Many defense agencies are upgrading conventional mortar systems with precision-guided ammunition, programmable fuse technologies, and digital fire control integration to improve battlefield effectiveness and mission adaptability. Modernization programs are also emphasizing extended-range mortar rounds and lightweight ammunition systems designed for rapid reaction forces and special operations units.

Autonomous targeting and drone-assisted fire adjustment programs are further increasing the effectiveness of mortar operations by enabling real-time battlefield intelligence and improved target acquisition. Several military organizations are also investing in vehicle-mounted and self-propelled mortar systems that combine mobility with enhanced firepower support. Recent developments in mobile mortar carriers and network-enabled mortar platforms demonstrate the growing emphasis on highly responsive and integrated indirect fire systems.

Research and development initiatives focused on smart munitions, advanced propellants, insensitive explosives, and precision guidance technologies continue to shape the future of the market. In addition, collaborative defense programs and indigenous ammunition manufacturing initiatives are supporting long-term innovation and production expansion in the global 60mm and 81mm mortar ammunition industry.

Table of Contents

Mortar Ammunition Market - Table of Contents

Mortar Ammunition Market Report Definition

Mortar Ammunition Market Segmentation

By Guidance

By Type

By Region

Mortar Ammunition Market Analysis for next 10 Years

The 10-year mortar ammunition market analysis would give a detailed overview of mortar ammunition market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Mortar Ammunition Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Mortar Ammunition Market Forecast

The 10-year mortar ammunition market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Mortar Ammunition Market Trends & Forecast

The regional mortar ammunition market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Access Control Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Mortar Ammunition Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Mortar Ammunition Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports

List of Tables

- Table 1: 10 Year Market Outlook, 2026-2036

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, Apac

- Table 12: Restraints, Impact Analysis, Apac

- Table 13: Challenges, Impact Analysis, Apac

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Region, 2026-2036

- Table 18: Scenario Analysis, Scenario 1, By Type 2026-2036

- Table 19: Scenario Analysis, Scenario 1, By Guidance, 2026-2036

- Table 20: Scenario Analysis, Scenario 2, By Region, 2026-2036

- Table 21: Scenario Analysis, Scenario 2, By Type 2026-2036

- Table 22: Scenario Analysis, Scenario 2, By Guidance, 2026-2036

List of Figures

- Figure 1: Global Defense Mortar Ammunition Market Forecast, 2026-2036

- Figure 2: Global Defense Mortar Ammunition Market Forecast, By Region, 2026-2036

- Figure 3: Global Defense Mortar Ammunition Market Forecast, By Type 2026-2036

- Figure 4: Global Defense Mortar Ammunition Market Forecast, By Guidance, 2026-2036

- Figure 5: North America, Defense Mortar Ammunition Market , Market Forecast, 2026-2036

- Figure 6: Europe, Defense Mortar Ammunition Market , Market Forecast, 2026-2036

- Figure 7: Middle East, Defense Mortar Ammunition Market , Market Forecast, 2026-2036

- Figure 8: Apac, Defense Mortar Ammunition Market , Market Forecast, 2026-2036

- Figure 9: South America, Defense Mortar Ammunition Market , Market Forecast, 2026-2036

- Figure 10: United States, Defense Mortar Ammunition Market , Region Maturation, 2026-2036

- Figure 11: United States, Defense Mortar Ammunition Market , Market Forecast, 2026-2036

- Figure 12: Canada, Defense Mortar Ammunition Market , Region Maturation, 2026-2036

- Figure 13: Canada, Defense Mortar Ammunition Market , Market Forecast, 2026-2036

- Figure 14: Italy, Defense Mortar Ammunition Market , Region Maturation, 2026-2036

- Figure 15: Italy, Defense Mortar Ammunition Market , Market Forecast, 2026-2036

- Figure 16: France, Defense Mortar Ammunition Market , Region Maturation, 2026-2036

- Figure 17: France, Defense Mortar Ammunition Market , Market Forecast, 2026-2036

- Figure 18: Germany, Defense Mortar Ammunition Market , Region Maturation, 2026-2036

- Figure 19: Germany, Defense Mortar Ammunition Market , Market Forecast, 2026-2036

- Figure 20: Netherlands, Defense Mortar Ammunition Market , Region Maturation, 2026-2036

- Figure 21: Netherlands, Defense Mortar Ammunition Market , Market Forecast, 2026-2036

- Figure 22: Belgium, Defense Mortar Ammunition Market , Region Maturation, 2026-2036

- Figure 23: Belgium, Defense Mortar Ammunition Market , Market Forecast, 2026-2036

- Figure 24: Spain, Defense Mortar Ammunition Market , Region Maturation, 2026-2036

- Figure 25: Spain, Defense Mortar Ammunition Market , Market Forecast, 2026-2036

- Figure 26: Sweden, Defense Mortar Ammunition Market , Region Maturation, 2026-2036

- Figure 27: Sweden, Defense Mortar Ammunition Market , Market Forecast, 2026-2036

- Figure 28: Brazil, Defense Mortar Ammunition Market , Region Maturation, 2026-2036

- Figure 29: Brazil, Defense Mortar Ammunition Market , Market Forecast, 2026-2036

- Figure 30: Australia, Defense Mortar Ammunition Market , Region Maturation, 2026-2036

- Figure 31: Australia, Defense Mortar Ammunition Market , Market Forecast, 2026-2036

- Figure 32: India, Defense Mortar Ammunition Market , Region Maturation, 2026-2036

- Figure 33: India, Defense Mortar Ammunition Market , Market Forecast, 2026-2036

- Figure 34: China, Defense Mortar Ammunition Market , Region Maturation, 2026-2036

- Figure 35: China, Defense Mortar Ammunition Market , Market Forecast, 2026-2036

- Figure 36: Saudi Arabia, Defense Mortar Ammunition Market , Region Maturation, 2026-2036

- Figure 37: Saudi Arabia, Defense Mortar Ammunition Market , Market Forecast, 2026-2036

- Figure 38: South Korea, Defense Mortar Ammunition Market , Region Maturation, 2026-2036

- Figure 39: South Korea, Defense Mortar Ammunition Market , Market Forecast, 2026-2036

- Figure 40: Japan, Defense Mortar Ammunition Market , Region Maturation, 2026-2036

- Figure 41: Japan, Defense Mortar Ammunition Market , Market Forecast, 2026-2036

- Figure 42: Malaysia, Defense Mortar Ammunition Market , Region Maturation, 2026-2036

- Figure 43: Malaysia, Defense Mortar Ammunition Market , Market Forecast, 2026-2036

- Figure 44: Singapore, Defense Mortar Ammunition Market , Region Maturation, 2026-2036

- Figure 45: Singapore, Defense Mortar Ammunition Market , Market Forecast, 2026-2036

- Figure 46: United Kingdom, Defense Mortar Ammunition Market , Region Maturation, 2026-2036

- Figure 47: United Kingdom, Defense Mortar Ammunition Market , Market Forecast, 2026-2036

- Figure 48: Opportunity Analysis, Defense Mortar Ammunition Market , By Region (Cumulative Market), 2026-2036

- Figure 49: Opportunity Analysis, Defense Mortar Ammunition Market , By Region (Cagr), 2026-2036

- Figure 50: Opportunity Analysis, Defense Mortar Ammunition Market , By Type Cumulative Market), 2026-2036

- Figure 51: Opportunity Analysis, Defense Mortar Ammunition Market , By Type (Cagr), 2026-2036

- Figure 52: Opportunity Analysis, Defense Mortar Ammunition Market , By Guidance(Cumulative Market), 2026-2036

- Figure 53: Opportunity Analysis, Defense Mortar Ammunition Market , By Guidance (Cagr), 2026-2036

- Figure 54: Scenario Analysis, Defense Mortar Ammunition Market , Cumulative Market, 2026-2036

- Figure 55: Scenario Analysis, Defense Mortar Ammunition Market , Global Market, 2026-2036

- Figure 56: Scenario 1, Defense Mortar Ammunition Market , Total Market, 2026-2036

- Figure 57: Scenario 1, Defense Mortar Ammunition Market , By Region, 2026-2036

- Figure 58: Scenario 1, Defense Mortar Ammunition Market , By Type 2026-2036

- Figure 59: Scenario 1, Defense Mortar Ammunition Market , By Guidance, 2026-2036

- Figure 60: Scenario 2, Defense Mortar Ammunition Market , Total Market, 2026-2036

- Figure 61: Scenario 2, Defense Mortar Ammunition Market , By Region, 2026-2036

- Figure 62: Scenario 2, Defense Mortar Ammunition Market , By Type 2026-2036

- Figure 63: Scenario 2, Defense Mortar Ammunition Market , By Guidance, 2026-2036

- Figure 64: Company Benchmark, Defense Mortar Ammunition Market , 2026-2036