PUBLISHER: Aviation & Defense Market Reports (A&D) | PRODUCT CODE: 2037794

PUBLISHER: Aviation & Defense Market Reports (A&D) | PRODUCT CODE: 2037794

Global Main Battle Tank Market 2026-2036

Global Main Battle Tank Market

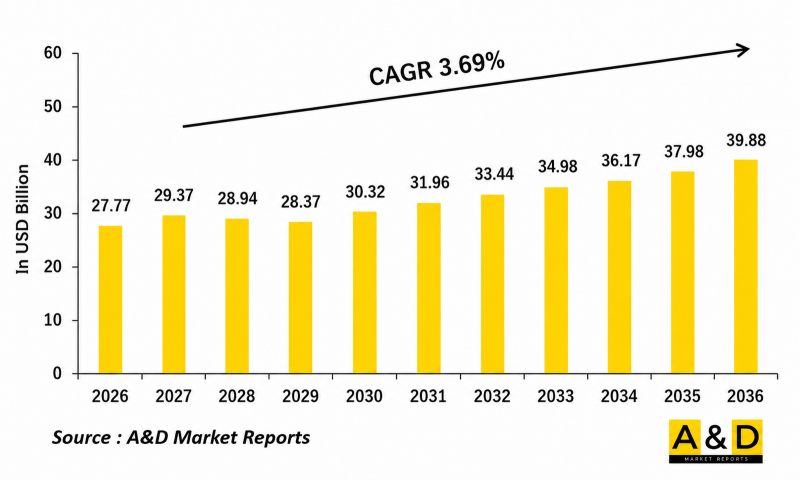

The Global Main Battle Tank Market is estimated at USD 27.77 billion in 2026, projected to grow to USD 39.88 billion by 2036 at a Compound Annual Growth Rate (CAGR) of 3.69% over the forecast period 2026-2036.

Introduction

The global main battle tank market continues to evolve as defense forces worldwide strengthen armored warfare capabilities to address emerging battlefield threats and high-intensity combat scenarios. Main battle tanks remain essential assets for land-based military operations due to their firepower, mobility, survivability, and battlefield versatility. Modern defense strategies increasingly emphasize advanced armored platforms capable of operating in complex multi-domain combat environments. Countries are investing in tank modernization programs, fleet upgrades, and next-generation armored vehicle development to enhance operational readiness and deterrence capabilities. Contemporary main battle tanks are being equipped with advanced targeting systems, digital battlefield management technologies, active protection systems, and improved armor solutions. The growing importance of survivability against anti-tank missiles, drones, and precision-guided munitions is accelerating technological transformation across the market. Rising geopolitical tensions and the need for rapid military response capabilities are also contributing to increased procurement and modernization initiatives in the global main battle tank sector.

Technology Impact in Global Main Battle Tank Market

Technological innovation is reshaping the global main battle tank market by improving battlefield survivability, operational efficiency, and combat effectiveness. Advanced active protection systems are becoming a critical component of modern tanks, enabling vehicles to detect and neutralize incoming threats such as anti-tank guided missiles and drones. Artificial intelligence and digital command systems are also improving situational awareness, target acquisition, and real-time battlefield coordination.

Modern tanks are increasingly incorporating hybrid propulsion systems, advanced sensor fusion technologies, and autonomous support capabilities. Enhanced armor materials and modular protection systems are improving adaptability against evolving threats. In addition, remote weapon stations and integrated communication systems are supporting network-centric warfare operations. The use of predictive maintenance technologies and digital architectures is helping defense forces improve lifecycle management and operational reliability.

Unmanned systems integration is another important technological development, with tanks increasingly operating alongside drones and autonomous reconnaissance platforms. These technologies are enhancing reconnaissance, targeting accuracy, and battlefield intelligence gathering. As military operations become more digitally connected and threat environments more complex, technological advancement remains a key factor shaping the future of the global main battle tank market.

Key Drivers in Global Main Battle Tank Market

The global main battle tank market is driven by rising geopolitical instability, military modernization initiatives, and increasing focus on armored warfare readiness. Many nations are reinforcing land combat capabilities to address evolving regional security challenges and strengthen national defense strategies. The growing importance of armored mobility in contested battlefield environments has accelerated investments in advanced tank platforms and modernization programs.

Another major driver is the increasing threat posed by anti-tank missiles, loitering munitions, and armed drones. Defense forces are therefore prioritizing tanks equipped with advanced protection systems, digital battlefield management technologies, and enhanced survivability solutions. The integration of active protection systems and modern sensor technologies has become essential for maintaining battlefield effectiveness.

The demand for interoperability within multi-domain operations is also contributing to market growth. Modern military doctrines increasingly require tanks to operate seamlessly with infantry units, unmanned systems, and networked command platforms. Furthermore, many countries are upgrading legacy tank fleets instead of replacing them entirely, creating opportunities for retrofit programs involving digital systems, armor upgrades, and propulsion enhancements.

Industrial collaboration and domestic defense manufacturing initiatives are further strengthening market expansion. Governments are encouraging indigenous tank production and technology transfer agreements to reduce dependency on foreign suppliers. As armored warfare continues to play a crucial role in modern military operations, the global main battle tank market is expected to experience sustained technological and strategic development.

Regional Trends in Global Main Battle Tank Market

Regional trends in the global main battle tank market vary according to defense priorities, geopolitical conditions, and military modernization strategies. North America remains a significant market due to ongoing armored modernization programs and investments in advanced battlefield technologies. The region focuses on integrating digital architectures, active protection systems, and improved mobility solutions into next-generation tank platforms.

Europe is witnessing substantial market activity driven by rising regional security concerns and collaborative armored vehicle development programs. Several European nations are upgrading legacy fleets while also participating in future armored combat system initiatives designed to improve interoperability and battlefield resilience. Asia-Pacific is emerging as a rapidly expanding market due to increasing defense budgets, border security concerns, and indigenous armored vehicle production efforts. Countries in the region are strengthening armored capabilities through modernization and domestic manufacturing initiatives.

The Middle East continues to invest heavily in armored warfare platforms due to regional security challenges and the need for high-intensity combat readiness. Modernization of tank fleets and procurement of advanced protection technologies remain major priorities across the region. Meanwhile, Latin America and Africa are gradually modernizing armored forces through selective upgrades and procurement programs focused on improving operational mobility and survivability. Across all regions, the demand for technologically advanced and highly survivable armored platforms continues to drive innovation in the main battle tank market.

Key Global Main Battle Tank Market Program

Key programs in the global main battle tank market focus on modernization, survivability enhancement, digital integration, and next-generation armored combat systems. Defense organizations worldwide are upgrading existing tank fleets with active protection systems, modern fire-control systems, digital communications, and enhanced armor technologies. These modernization initiatives are intended to improve battlefield effectiveness against evolving threats such as drones and precision-guided munitions.

Several countries are also pursuing next-generation tank development programs designed to integrate artificial intelligence, autonomous support capabilities, and advanced propulsion systems. Collaborative international programs are becoming increasingly important as governments seek cost-effective approaches to armored vehicle development. Research initiatives related to hybrid power systems, modular armor designs, and battlefield networking are shaping the future of tank warfare.

In addition, defense industries are focusing on integrating unmanned systems with armored platforms to improve reconnaissance and operational coordination. Digital battlefield management systems are enabling real-time data sharing and enhanced situational awareness during combat operations. Many modernization programs are also emphasizing sustainability, maintainability, and lifecycle efficiency to reduce long-term operational costs.

As military strategies continue evolving toward network-centric and multi-domain warfare, key tank programs worldwide are expected to prioritize survivability, mobility, and technological adaptability to maintain armored superiority in future combat environments.

Table of Contents

Main Battle Tank Market - Table of Contents

Main Battle Tank Market Report Definition

Main Battle Tank Market Segmentation

By Region

By Type

Main Battle Tank Market Analysis for next 10 Years

The 10-year Main Battle Tank Market analysis would give a detailed overview of Main Battle Tank Market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Main Battle Tank Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Main Battle Tank Market Forecast

The 10-year Main Battle Tank Market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Main Battle Tank Market Trends & Forecast

The regional Main Battle Tank Market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Main Battle Tank Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Main Battle Tank Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Main Battle Tank Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports

List of Tables

- Table 1: 10 Year Market Outlook, 2026-2036

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, Apac

- Table 12: Restraints, Impact Analysis, Apac

- Table 13: Challenges, Impact Analysis, Apac

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Region, 2026-2036

- Table 18: Scenario Analysis, Scenario 1, By Process 2026-2036

- Table 19: Scenario Analysis, Scenario 1, By Component, 2026-2036

- Table 20: Scenario Analysis, Scenario 2, By Region, 2026-2036

- Table 21: Scenario Analysis, Scenario 2, By Process 2026-2036

- Table 22: Scenario Analysis, Scenario 2, By Component, 2026-2036

List of Figures

- Figure 1: Global Defense Main Battle Tank Market Forecast, 2026-2036

- Figure 2: Global Defense Main Battle Tank Market Forecast, By Region, 2026-2036

- Figure 3: Global Defense Main Battle Tank Market Forecast, By Process 2026-2036

- Figure 4: Global Defense Main Battle Tank Market Forecast, By Component, 2026-2036

- Figure 5: North America, Defense Main Battle Tank Market , Market Forecast, 2026-2036

- Figure 6: Europe, Defense Main Battle Tank Market , Market Forecast, 2026-2036

- Figure 7: Middle East, Defense Main Battle Tank Market , Market Forecast, 2026-2036

- Figure 8: Apac, Defense Main Battle Tank Market , Market Forecast, 2026-2036

- Figure 9: South America, Defense Main Battle Tank Market , Market Forecast, 2026-2036

- Figure 10: United States, Defense Main Battle Tank Market , Region Maturation, 2026-2036

- Figure 11: United States, Defense Main Battle Tank Market , Market Forecast, 2026-2036

- Figure 12: Canada, Defense Main Battle Tank Market , Region Maturation, 2026-2036

- Figure 13: Canada, Defense Main Battle Tank Market , Market Forecast, 2026-2036

- Figure 14: Italy, Defense Main Battle Tank Market , Region Maturation, 2026-2036

- Figure 15: Italy, Defense Main Battle Tank Market , Market Forecast, 2026-2036

- Figure 16: France, Defense Main Battle Tank Market , Region Maturation, 2026-2036

- Figure 17: France, Defense Main Battle Tank Market , Market Forecast, 2026-2036

- Figure 18: Germany, Defense Main Battle Tank Market , Region Maturation, 2026-2036

- Figure 19: Germany, Defense Main Battle Tank Market , Market Forecast, 2026-2036

- Figure 20: Netherlands, Defense Main Battle Tank Market , Region Maturation, 2026-2036

- Figure 21: Netherlands, Defense Main Battle Tank Market , Market Forecast, 2026-2036

- Figure 22: Belgium, Defense Main Battle Tank Market , Region Maturation, 2026-2036

- Figure 23: Belgium, Defense Main Battle Tank Market , Market Forecast, 2026-2036

- Figure 24: Spain, Defense Main Battle Tank Market , Region Maturation, 2026-2036

- Figure 25: Spain, Defense Main Battle Tank Market , Market Forecast, 2026-2036

- Figure 26: Sweden, Defense Main Battle Tank Market , Region Maturation, 2026-2036

- Figure 27: Sweden, Defense Main Battle Tank Market , Market Forecast, 2026-2036

- Figure 28: Brazil, Defense Main Battle Tank Market , Region Maturation, 2026-2036

- Figure 29: Brazil, Defense Main Battle Tank Market , Market Forecast, 2026-2036

- Figure 30: Australia, Defense Main Battle Tank Market , Region Maturation, 2026-2036

- Figure 31: Australia, Defense Main Battle Tank Market , Market Forecast, 2026-2036

- Figure 32: India, Defense Main Battle Tank Market , Region Maturation, 2026-2036

- Figure 33: India, Defense Main Battle Tank Market , Market Forecast, 2026-2036

- Figure 34: China, Defense Main Battle Tank Market , Region Maturation, 2026-2036

- Figure 35: China, Defense Main Battle Tank Market , Market Forecast, 2026-2036

- Figure 36: Saudi Arabia, Defense Main Battle Tank Market , Region Maturation, 2026-2036

- Figure 37: Saudi Arabia, Defense Main Battle Tank Market , Market Forecast, 2026-2036

- Figure 38: South Korea, Defense Main Battle Tank Market , Region Maturation, 2026-2036

- Figure 39: South Korea, Defense Main Battle Tank Market , Market Forecast, 2026-2036

- Figure 40: Japan, Defense Main Battle Tank Market , Region Maturation, 2026-2036

- Figure 41: Japan, Defense Main Battle Tank Market , Market Forecast, 2026-2036

- Figure 42: Malaysia, Defense Main Battle Tank Market , Region Maturation, 2026-2036

- Figure 43: Malaysia, Defense Main Battle Tank Market , Market Forecast, 2026-2036

- Figure 44: Singapore, Defense Main Battle Tank Market , Region Maturation, 2026-2036

- Figure 45: Singapore, Defense Main Battle Tank Market , Market Forecast, 2026-2036

- Figure 46: United Kingdom, Defense Main Battle Tank Market , Region Maturation, 2026-2036

- Figure 47: United Kingdom, Defense Main Battle Tank Market , Market Forecast, 2026-2036

- Figure 48: Opportunity Analysis, Defense Main Battle Tank Market , By Region (Cumulative Market), 2026-2036

- Figure 49: Opportunity Analysis, Defense Main Battle Tank Market , By Region (Cagr), 2026-2036

- Figure 50: Opportunity Analysis, Defense Main Battle Tank Market , By Process Cumulative Market), 2026-2036

- Figure 51: Opportunity Analysis, Defense Main Battle Tank Market , By Process (Cagr), 2026-2036

- Figure 52: Opportunity Analysis, Defense Main Battle Tank Market , By Component(Cumulative Market), 2026-2036

- Figure 53: Opportunity Analysis, Defense Main Battle Tank Market , By Component (Cagr), 2026-2036

- Figure 54: Scenario Analysis, Defense Main Battle Tank Market , Cumulative Market, 2026-2036

- Figure 55: Scenario Analysis, Defense Main Battle Tank Market , Global Market, 2026-2036

- Figure 56: Scenario 1, Defense Main Battle Tank Market , Total Market, 2026-2036

- Figure 57: Scenario 1, Defense Main Battle Tank Market , By Region, 2026-2036

- Figure 58: Scenario 1, Defense Main Battle Tank Market , By Process 2026-2036

- Figure 59: Scenario 1, Defense Main Battle Tank Market , By Component, 2026-2036

- Figure 60: Scenario 2, Defense Main Battle Tank Market , Total Market, 2026-2036

- Figure 61: Scenario 2, Defense Main Battle Tank Market , By Region, 2026-2036

- Figure 62: Scenario 2, Defense Main Battle Tank Market , By Process 2026-2036

- Figure 63: Scenario 2, Defense Main Battle Tank Market , By Component, 2026-2036

- Figure 64: Company Benchmark, Defense Main Battle Tank Market , 2026-2036