PUBLISHER: Aviation & Defense Market Reports (A&D) | PRODUCT CODE: 2004303

PUBLISHER: Aviation & Defense Market Reports (A&D) | PRODUCT CODE: 2004303

Global Defense Aircraft Turbines and Compressors Market 2026-2036

Global Defense Aircraft Turbines and Compressors Market

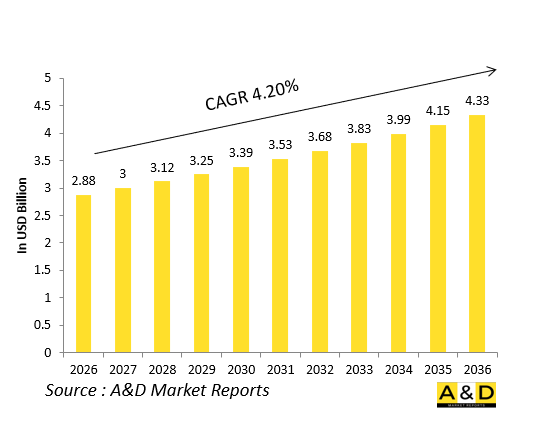

The Global Defense Aircraft Turbines and Compressors Market is estimated at USD 2.88 billion in 2026, projected to grow to USD 4.33 billion by 2036 at a Compound Annual Growth Rate (CAGR) of 4.20% over the forecast period 2026-2036.

Introduction:

The global defense aircraft turbines and compressors market forms the core of military aircraft propulsion systems, enabling thrust generation, fuel efficiency, and overall engine performance. Compressors increase the pressure of incoming air before combustion, while turbines extract energy from exhaust gases to power the engine and drive compressor stages. These components are essential in turbofan, turbojet, and turboshaft engines used across fighter jets, transport aircraft, helicopters, and unmanned aerial systems.

Between 2026 and 2036, the market is expected to grow steadily, supported by increasing defense budgets and next-generation aircraft development programs. Compressors and turbines are central to improving thrust-to-weight ratios, operational efficiency, and mission endurance. The rising complexity of modern aircraft engines and the shift toward adaptive and high-efficiency propulsion systems are further reinforcing the importance of these components in defense aviation.

Technology Impact in Global Defense Aircraft Turbines and Compressors Market

Technological advancements are significantly transforming turbines and compressors, particularly through innovations in materials, aerodynamics, and digitalization. The adoption of advanced materials such as ceramic matrix composites (CMCs) and titanium alloys is enabling higher temperature tolerance, reduced weight, and improved durability.

Additive manufacturing (3D printing) is revolutionizing the production of compressor blades and turbine components, allowing complex geometries and improved performance efficiency. Additionally, variable-geometry compressors and adaptive-cycle engine technologies are enhancing operational flexibility, enabling aircraft to optimize performance across different mission profiles.

Digital twin technology and IoT-based monitoring systems are also being integrated, enabling predictive maintenance and real-time performance optimization. These advancements are reducing lifecycle costs and improving reliability, making turbines and compressors more efficient and adaptable for modern defense aviation requirements.

Key Drivers in Global Defense Aircraft Turbines and Compressors Market

The primary driver of the market is the increasing global defense expenditure and the procurement of advanced military aircraft. Rising investments in next-generation fighter jets and UAVs are creating strong demand for high-performance propulsion systems.

Another key driver is the emphasis on fuel efficiency and performance optimization. Compressors play a critical role in increasing air pressure and improving combustion efficiency, while turbines enhance energy extraction and thrust generation.

Additionally, fleet modernization and the replacement of aging aircraft are boosting demand for advanced turbine and compressor technologies. The growing importance of maintenance, repair, and overhaul (MRO) services is also contributing to market expansion, as these components require regular servicing due to high operational stress.

The increasing adoption of UAVs and advanced propulsion systems further expands the application scope, ensuring sustained growth in the defense segment.

Regional Trends in Global Defense Aircraft Turbines and Compressors Market

North America dominates the global market, supported by strong defense spending, advanced aerospace infrastructure, and significant investments in next-generation propulsion technologies. The region benefits from ongoing fighter aircraft and engine development programs.

Europe holds a substantial market share, driven by collaborative defense initiatives and modernization efforts among NATO countries. The region emphasizes innovation in propulsion technologies and sustainable aviation solutions.

The Asia-Pacific region is expected to witness the fastest growth during the forecast period, fueled by rising defense budgets and expanding indigenous aircraft manufacturing capabilities in countries such as India, China, and Japan. Increasing procurement of advanced fighter jets and UAVs is a key growth factor.

The Middle East is also emerging as a significant market due to ongoing investments in military aviation and the acquisition of high-performance aircraft. These regional dynamics reflect a global shift toward modernization and self-reliance in defense capabilities.

Key Global Defense Aircraft Turbines and Compressors Market Program

Key defense programs and engine development initiatives are driving innovation in turbines and compressors. Advanced fighter aircraft programs are increasingly adopting adaptive-cycle engines, which utilize variable-geometry compressors to enhance efficiency and range.

Additionally, military engine programs focusing on turbofan and turboshaft technologies are expanding, particularly for fighter jets, helicopters, and UAVs. These programs emphasize improved thermal efficiency, durability, and performance under extreme conditions.

Collaborations between defense agencies and aerospace manufacturers are accelerating the development of next-generation propulsion systems. Investments in R&D, including hybrid-electric and sustainable propulsion technologies, are further shaping the market landscape.

These programs highlight the strategic importance of turbines and compressors in enhancing aircraft performance, mission capability, and operational efficiency in modern defense aviation.

Table of Contents

Defense Aircraft Turbines and Compressors Market - Table of Contents

Defense Aircraft Turbines and Compressors Market Report Definition

Defense Aircraft Turbines and Compressors Market Segmentation

-By Platform

-By Application

-By Technology

-By Material

Defense Aircraft Turbines and Compressors Market Analysis for next 10 Years

The 10-year Defense Aircraft Turbines and Compressors Market analysis would give a detailed overview of Defense Aircraft Turbines and Compressors Market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Defense Aircraft Turbines and Compressors Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Defense Aircraft Turbines and Compressors Market Forecast

The 10-year Defense Aircraft Turbines and Compressors Market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Defense Aircraft Turbines and Compressors Market Trends & Forecast

The regional counter drone market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Defense Aircraft Turbines and Compressors Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Defense Aircraft Turbines and Compressors Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Defense Aircraft Turbines and Compressors Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports

List of Tables

- Table 1: 10 Year Market Outlook, 2026-2036

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, APAC

- Table 12: Restraints, Impact Analysis, APAC

- Table 13: Challenges, Impact Analysis, APAC

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Application, 2026-2036

- Table 18: Scenario Analysis, Scenario 1, By Platform, 2026-2036

- Table 19: Scenario Analysis, Scenario 1,By Technology, 2026-2036

- Table 20: Scenario Analysis, Scenario 2, By Application, 2026-2036

- Table 21: Scenario Analysis, Scenario 2, By Platform, 2026-2036

- Table 22: Scenario Analysis, Scenario 2,By Technology, 2026-2036

List of Figures

- Figure 1: Global Defense Aircraft Turbines and Compressors Market Forecast, 2026-2036

- Figure 2: Global Defense Aircraft Turbines and Compressors Market Forecast, By Application, 2026-2036

- Figure 3: Global Defense Aircraft Turbines and Compressors Market Forecast, By Platform, 2026-2036

- Figure 4: Global Defense Aircraft Turbines and Compressors Market Forecast, By Technology, 2026-2036

- Figure 5: North America, Defense Aircraft Turbines and Compressors Market Forecast, 2026-2036

- Figure 6: Europe, Defense Aircraft Turbines and Compressors Market Forecast, 2026-2036

- Figure 7: Middle East, Defense Aircraft Turbines and Compressors Market Forecast, 2026-2036

- Figure 8: APAC, Defense Aircraft Turbines and Compressors Market, Market Forecast, 2026-2036

- Figure 9: South America, Defense Aircraft Turbines and Compressors Market Forecast, 2026-2036

- Figure 10: United States, Defense Aircraft Turbines and Compressors Market, Region Maturation, 2026-2036

- Figure 11: United States, Defense Aircraft Turbines and Compressors Market Forecast, 2026-2036

- Figure 12: Canada, Defense Aircraft Turbines and Compressors Market, Region Maturation, 2026-2036

- Figure 13: Canada, Defense Aircraft Turbines and Compressors Market Forecast, 2026-2036

- Figure 14: Italy, Defense Aircraft Turbines and Compressors Market , Region Maturation, 2026-2036

- Figure 15: Italy, Defense Aircraft Turbines and Compressors Market Forecast, 2026-2036

- Figure 16: France, Defense Aircraft Turbines and Compressors Market , Region Maturation, 2026-2036

- Figure 17: France, Defense Aircraft Turbines and Compressors Market Forecast, 2026-2036

- Figure 18: Germany, Defense Aircraft Turbines and Compressors Market , Region Maturation, 2026-2036

- Figure 19: Germany, Defense Aircraft Turbines and Compressors Market Forecast, 2026-2036

- Figure 20: Netherlands, Defense Aircraft Turbines and Compressors Market , Region Maturation, 2026-2036

- Figure 21: Netherlands, Defense Aircraft Turbines and Compressors Market Forecast, 2026-2036

- Figure 22: Belgium, Defense Aircraft Turbines and Compressors Market , Region Maturation, 2026-2036

- Figure 23: Belgium, Defense Aircraft Turbines and Compressors Market Forecast, 2026-2036

- Figure 24: Spain, Defense Aircraft Turbines and Compressors Market , Region Maturation, 2026-2036

- Figure 25: Spain, Defense Aircraft Turbines and Compressors Market Forecast, 2026-2036

- Figure 26: Sweden, Defense Aircraft Turbines and Compressors Market , Region Maturation, 2026-2036

- Figure 27: Sweden, Defense Aircraft Turbines and Compressors Market Forecast, 2026-2036

- Figure 28: Brazil, Defense Aircraft Turbines and Compressors Market , Region Maturation, 2026-2036

- Figure 29: Brazil, Defense Aircraft Turbines and Compressors Market Forecast, 2026-2036

- Figure 30: Australia, Defense Aircraft Turbines and Compressors Market , Region Maturation, 2026-2036

- Figure 31: Australia, Defense Aircraft Turbines and Compressors Market Forecast, 2026-2036

- Figure 32: India, Defense Aircraft Turbines and Compressors Market , Region Maturation, 2026-2036

- Figure 33: India, Defense Aircraft Turbines and Compressors Market Forecast, 2026-2036

- Figure 34: China, Defense Aircraft Turbines and Compressors Market , Region Maturation, 2026-2036

- Figure 35: China, Defense Aircraft Turbines and Compressors Market Forecast, 2026-2036

- Figure 36: Saudi Arabia, Defense Aircraft Turbines and Compressors Market , Region Maturation, 2026-2036

- Figure 37: Saudi Arabia, Defense Aircraft Turbines and Compressors Market Forecast, 2026-2036

- Figure 38: South Korea, Defense Aircraft Turbines and Compressors Market , Region Maturation, 2026-2036

- Figure 39: South Korea, Defense Aircraft Turbines and Compressors Market Forecast, 2026-2036

- Figure 40: Japan, Defense Aircraft Turbines and Compressors Market , Region Maturation, 2026-2036

- Figure 41: Japan, Defense Aircraft Turbines and Compressors Market Forecast, 2026-2036

- Figure 42: Malaysia, Defense Aircraft Turbines and Compressors Market , Region Maturation, 2026-2036

- Figure 43: Malaysia, Defense Aircraft Turbines and Compressors Market Forecast, 2026-2036

- Figure 44: Singapore, Defense Aircraft Turbines and Compressors Market , Region Maturation, 2026-2036

- Figure 45: Singapore, Defense Aircraft Turbines and Compressors Market Forecast, 2026-2036

- Figure 46: United Kingdom, Defense Aircraft Turbines and Compressors Market , Region Maturation, 2026-2036

- Figure 47: United Kingdom, Defense Aircraft Turbines and Compressors Market Forecast, 2026-2036

- Figure 48: Opportunity Analysis, Defense Aircraft Turbines and Compressors Market , By Application (Cumulative Market), 2026-2036

- Figure 49: Opportunity Analysis, Defense Aircraft Turbines and Compressors Market , By Application (CAGR), 2026-2036

- Figure 50: Opportunity Analysis, Defense Aircraft Turbines and Compressors Market , By Platform (Cumulative Market), 2026-2036

- Figure 51: Opportunity Analysis, Defense Aircraft Turbines and Compressors Market , By Platform (CAGR), 2026-2036

- Figure 52: Opportunity Analysis, Defense Aircraft Turbines and Compressors Market ,By Technology(Cumulative Market), 2026-2036

- Figure 53: Opportunity Analysis, Defense Aircraft Turbines and Compressors Market ,By Technology(CAGR), 2026-2036

- Figure 54: Scenario Analysis, Defense Aircraft Turbines and Compressors Market , Cumulative Market, 2026-2036

- Figure 55: Scenario Analysis, Defense Aircraft Turbines and Compressors Market , Global Market, 2026-2036

- Figure 56: Scenario 1, Defense Aircraft Turbines and Compressors Market , Total Market, 2026-2036

- Figure 57: Scenario 1, Defense Aircraft Turbines and Compressors Market , Region, 2026-2036

- Figure 58: Scenario 1, Defense Aircraft Turbines and Compressors Market , By Platform, 2026-2036

- Figure 59: Scenario 1, Defense Aircraft Turbines and Compressors Market ,By Technology, 2026-2036

- Figure 60: Scenario 2, Defense Aircraft Turbines and Compressors Market , Total Market, 2026-2036

- Figure 61: Scenario 2, Defense Aircraft Turbines and Compressors Market , By Application, 2026-2036

- Figure 62: Scenario 2, Defense Aircraft Turbines and Compressors Market , By Platform, 2026-2036

- Figure 63: Scenario 2, Defense Aircraft Turbines and Compressors Market ,By Technology, 2026-2036

- Figure 64: Company Benchmark, Defense Aircraft Turbines and Compressors Market , 2026-2036