PUBLISHER: Aviation & Defense Market Reports (A&D) | PRODUCT CODE: 1951131

PUBLISHER: Aviation & Defense Market Reports (A&D) | PRODUCT CODE: 1951131

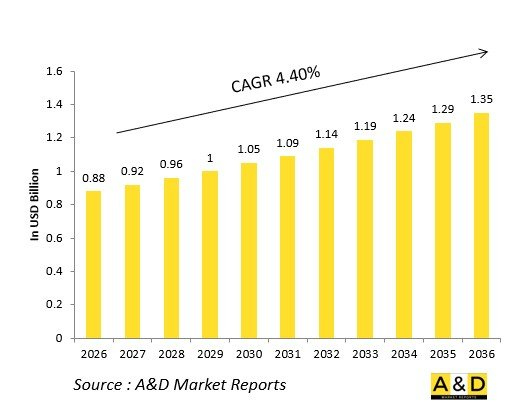

Global Defense Towed Array Sonars Market 2026-2036

The Global defense towed array sonar market is estimated at USD 0.88 billion in 2026, projected to grow to USD 1.35 billion by 2036 at a Compound Annual Growth Rate (CAGR) of 4.40% over the forecast period 2026-2036.

Introduction:

The global defense towed array sonar market is experiencing strong momentum driven by the increasing complexity of undersea warfare and the strategic importance of anti-submarine operations. Towed array sonars, mounted on surface vessels and submarines, play a vital role in long-range acoustic detection, threat tracking, and tactical situational awareness. As maritime powers expand their naval fleets, the demand for flexible and high-performance sonar systems continues to rise. Advances in digital signal processing, fiber-optic technology, and low-noise transducer arrays have significantly enhanced detection ranges and reliability. Integration of these systems with combat management networks enables real-time data sharing across platforms, reinforcing the concept of networked naval operations. With nations prioritizing maritime domain awareness and underwater security, the towed array sonar market is set to expand steadily, supported by extensive defense modernization programs and increasing focus on acoustic intelligence collection and undersea deterrence.

Technology Impact in Defense Towed Array Sonars

Emerging technologies are reshaping the design and functionality of defense towed array sonar systems. Modern systems employ advanced hydrophone arrays, digital beamforming, and machine learning algorithms for enhanced detection precision and reduced false alarms. Fiber-optic sensing and improved connectivity allow real-time data transmission with minimal signal loss, strengthening surveillance capabilities in deep and shallow waters alike. Miniaturization and modular design trends have improved deployment flexibility, allowing integration across multiple ship classes and unmanned surface vessels. The adoption of open architecture frameworks simplifies system upgrades and enhances interoperability with other naval sensors and acoustic platforms. Noise reduction technologies and adaptive signal filtering enable sustained performance in high-traffic maritime environments. As defense organizations push for multi-static and distributed sensing networks, the role of towed array sonars as core underwater awareness assets continues to expand in next-generation naval architectures.

Key Drivers in Defense Towed Array Sonars

Several strategic and operational drivers are fueling growth in the global towed array sonar market. Rising submarine proliferation and the increasing stealth capabilities of adversarial navies necessitate advanced detection systems capable of operating across extended ranges. Modern naval doctrines emphasize persistent undersea surveillance and rapid response, encouraging investment in high-sensitivity acoustic arrays. Ongoing modernization of surface fleets and submarines also supports steady adoption of towed sonar technology. The growing importance of data fusion and network-centric warfare drives integration between sonar arrays, combat systems, and autonomous underwater vehicles. Additionally, government initiatives promoting indigenous sensor production and technology transfer agreements are expanding industrial participation across emerging markets. The increasing need for maritime domain awareness, combined with the development of quieter, more capable sonar designs, ensures continued demand for towed array solutions across global naval defense strategies.

Regional Trends in Defense Towed Array Sonars

Regional market patterns in towed array sonars reflect varying defense postures, industrial capabilities, and maritime challenges. In North America, advanced anti-submarine warfare programs emphasize integration of towed array sensors with surface ship and submarine fleets. Europe's focus lies in collaborative research projects aimed at enhancing acoustic detection efficiency and modular interoperability among allied naval forces. The Asia-Pacific region demonstrates strong demand as nations expand their undersea surveillance networks amid rising territorial tensions and naval modernization efforts. In the Middle East, investment centers on coastal and deep-water security, supported by partnerships with global system providers. Emerging markets in Latin America and Africa are gradually adopting towed sonar technologies through foreign assistance and fleet enhancement programs. Across all regions, the emphasis on integrated undersea defense ecosystems continues to shape procurement strategies, highlighting towed array systems as essential components of modern maritime security.

Key Defense Towed Array Sonars Programs

Key defense programs worldwide are advancing the design, production, and deployment of next-generation towed array sonar systems. Major naval forces and industry leaders are collaborating to develop long-range, high-sensitivity arrays integrated with combat management and anti-submarine warfare frameworks. Several upgrade initiatives focus on retrofitting existing vessels with digital processing modules, fiber-optic links, and enhanced hydrophone configurations to improve performance and maintain interoperability. International cooperative programs emphasize shared research and development to reduce costs and accelerate delivery timelines. Many emerging defense nations are pursuing indigenous sonar production capabilities through technology transfer agreements and local manufacturing partnerships. These programs collectively signify a global trend toward resilient, low-drag, and energy-efficient arrays optimized for both manned and unmanned naval platforms. The continuous evolution of these systems underscores their pivotal role in sustaining undersea dominance and maritime strategic deterrence.

Table of Contents

Defense Towed Array Sonars Market - Table of Contents

Defense Towed Array Sonars Market Report Definition

Defense Towed Array Sonars Market Segmentation

By Region

By Platform

By Deployment

By Array Type

Defense Towed Array Sonars Market Analysis for next 10 Years

The 10-year Defense Towed Array Sonars Market analysis would give a detailed overview of Defense Towed Array Sonars Market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Defense Towed Array Sonars Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Defense Towed Array Sonars Market Forecast

The 10-year Defense Towed Array Sonars Market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Defense Towed Array Sonars Market Trends & Forecast

The regional counter drone market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Defense Towed Array Sonars Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Defense Towed Array Sonars Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Defense Towed Array Sonars Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports

List of Tables

- Table 1: 10 Year Market Outlook, 2026-2036

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, APAC

- Table 12: Restraints, Impact Analysis, APAC

- Table 13: Challenges, Impact Analysis, APAC

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Array Type, 2026-2036

- Table 18: Scenario Analysis, Scenario 1, By Platform, 2026-2036

- Table 19: Scenario Analysis, Scenario 1, By Region, 2026-2036

- Table 20: Scenario Analysis, Scenario 2, By Array Type, 2026-2036

- Table 21: Scenario Analysis, Scenario 2, By Platform, 2026-2036

- Table 22: Scenario Analysis, Scenario 2, By Region, 2026-2036

List of Figures

- Figure 1: Global Defense Towed Array Sonars Market Forecast, 2026-2036

- Figure 2: Global Defense Towed Array Sonars Market Forecast, By Array Type, 2026-2036

- Figure 3: Global Defense Towed Array Sonars Market Forecast, By Platform, 2026-2036

- Figure 4: Global Defense Towed Array Sonars Market Forecast, By Region, 2026-2036

- Figure 5: North America, Defense Towed Array Sonars Market, Forecast, 2026-2036

- Figure 6: Europe, Defense Towed Array Sonars Market, Forecast, 2026-2036

- Figure 7: Middle East, Defense Towed Array Sonars Market, Forecast, 2026-2036

- Figure 8: APAC, Defense Towed Array Sonars Market, Forecast, 2026-2036

- Figure 9: South America, Defense Towed Array Sonars Market, Forecast, 2026-2036

- Figure 10: United States, Defense Towed Array Sonars Market, Technology Maturation, 2026-2036

- Figure 11: United States, Defense Towed Array Sonars Market, Forecast, 2026-2036

- Figure 12: Canada, Defense Towed Array Sonars Market, Technology Maturation, 2026-2036

- Figure 13: Canada, Defense Towed Array Sonars Market, Forecast, 2026-2036

- Figure 14: Italy, Defense Towed Array Sonars Market, Technology Maturation, 2026-2036

- Figure 15: Italy, Defense Towed Array Sonars Market, Market Forecast, 2026-2036

- Figure 16: France, Defense Towed Array Sonars Market, Technology Maturation, 2026-2036

- Figure 17: France, Defense Towed Array Sonars Market, Market Forecast, 2026-2036

- Figure 18: Germany, Defense Towed Array Sonars Market, Technology Maturation, 2026-2036

- Figure 19: Germany, Defense Towed Array Sonars Market, Market Forecast, 2026-2036

- Figure 20: Netherlands, Defense Towed Array Sonars Market, Technology Maturation, 2026-2036

- Figure 21: Netherlands, Defense Towed Array Sonars Market, Market Forecast, 2026-2036

- Figure 22: Belgium, Defense Towed Array Sonars Market, Technology Maturation, 2026-2036

- Figure 23: Belgium, Defense Towed Array Sonars Market, Market Forecast, 2026-2036

- Figure 24: Spain, Defense Towed Array Sonars Market, Technology Maturation, 2026-2036

- Figure 25: Spain, Defense Towed Array Sonars Market, Market Forecast, 2026-2036

- Figure 26: Sweden, Defense Towed Array Sonars Market, Technology Maturation, 2026-2036

- Figure 27: Sweden, Defense Towed Array Sonars Market, Forecast, 2026-2036

- Figure 28: Brazil, Defense Towed Array Sonars Market, Technology Maturation, 2026-2036

- Figure 29: Brazil, Defense Towed Array Sonars Market, Market Forecast, 2026-2036

- Figure 30: Australia, Defense Towed Array Sonars Market, Technology Maturation, 2026-2036

- Figure 31: Australia, Defense Towed Array Sonars Market, Market Forecast, 2026-2036

- Figure 32: India, Defense Towed Array Sonars Market, Technology Maturation, 2026-2036

- Figure 33: India, Defense Towed Array Sonars Market, Market Forecast, 2026-2036

- Figure 34: China, Defense Towed Array Sonars Market, Technology Maturation, 2026-2036

- Figure 35: China, Defense Towed Array Sonars Market, Market Forecast, 2026-2036

- Figure 36: Saudi Arabia, Defense Towed Array Sonars Market, Technology Maturation, 2026-2036

- Figure 37: Saudi Arabia, Defense Towed Array Sonars Market, Market Forecast, 2026-2036

- Figure 38: South Korea, Defense Towed Array Sonars Market, Technology Maturation, 2026-2036

- Figure 39: South Korea, Defense Towed Array Sonars Market, Market Forecast, 2026-2036

- Figure 40: Japan, Defense Towed Array Sonars Market, Technology Maturation, 2026-2036

- Figure 41: Japan, Defense Towed Array Sonars Market, Market Forecast, 2026-2036

- Figure 42: Malaysia, Defense Towed Array Sonars Market, Technology Maturation, 2026-2036

- Figure 43: Malaysia, Defense Towed Array Sonars Market, Market Forecast, 2026-2036

- Figure 44: Singapore, Defense Towed Array Sonars Market, Technology Maturation, 2026-2036

- Figure 45: Singapore, Defense Towed Array Sonars Market, Market Forecast, 2026-2036

- Figure 46: United Kingdom, Defense Towed Array Sonars Market, Technology Maturation, 2026-2036

- Figure 47: United Kingdom, Defense Towed Array Sonars Market, Market Forecast, 2026-2036

- Figure 48: Opportunity Analysis, Defense Towed Array Sonars Market, By Array Type (Cumulative Market), 2026-2036

- Figure 49: Opportunity Analysis, Defense Towed Array Sonars Market, By Array Type (CAGR), 2026-2036

- Figure 50: Opportunity Analysis, Defense Towed Array Sonars Market, By (Cumulative Market), 2026-2036

- Figure 51: Opportunity Analysis, Defense Towed Array Sonars Market, By Platform(CAGR), 2026-2036

- Figure 52: Opportunity Analysis, Defense Towed Array Sonars Market, By Region (Cumulative Market), 2026-2036

- Figure 53: Opportunity Analysis, Defense Towed Array Sonars Market, By Region (CAGR), 2026-2036

- Figure 54: Scenario Analysis, Defense Towed Array Sonars Market, Cumulative Market, 2026-2036

- Figure 55: Scenario Analysis, Defense Towed Array Sonars Market, Global Market, 2026-2036

- Figure 56: Scenario 1, Defense Towed Array Sonars Market, Total Market, 2026-2036

- Figure 57: Scenario 1, Defense Towed Array Sonars Market, By Array Type, 2026-2036

- Figure 58: Scenario 1, Defense Towed Array Sonars Market, By Platform, 2026-2036

- Figure 59: Scenario 1, Defense Towed Array Sonars Market, By Region, 2026-2036

- Figure 60: Scenario 2, Defense Towed Array Sonars Market, Total Market, 2026-2036

- Figure 61: Scenario 2, Defense Towed Array Sonars Market, By Array Type, 2026-2036

- Figure 62: Scenario 2, Defense Towed Array Sonars Market, By Platform, 2026-2036

- Figure 63: Scenario 2, Defense Towed Array Sonars Market, By Region, 2026-2036

- Figure 64: Company Benchmark, Defense Towed Array Sonars Market, 2026-2036