PUBLISHER: Aviation & Defense Market Reports (A&D) | PRODUCT CODE: 1996982

PUBLISHER: Aviation & Defense Market Reports (A&D) | PRODUCT CODE: 1996982

Global Defense Up-Front Control Panels (UFC) Market 2026-2036

Global Defense Up-Front Control Panels (UFC) Market

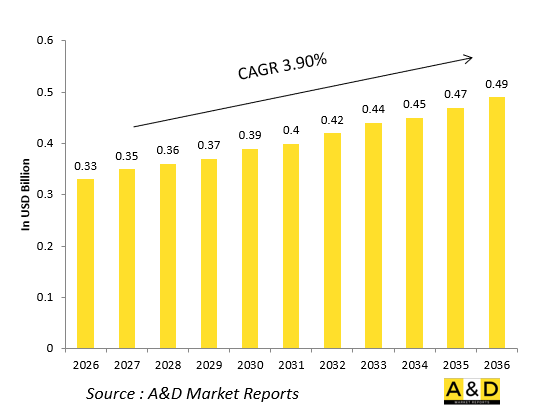

The Global Defense Up-Front Control Panels (UFC) Market is estimated at USD 0.33 billion in 2026, projected to grow to USD 0.49 billion by 2036 at a Compound Annual Growth Rate (CAGR) of 3.90% over the forecast period 2026-2036.

Introduction:

Up-Front Control Panels (UFC) represent a critical interface in modern defense platforms, serving as the primary human-machine interaction hub for aircraft cockpits, naval command centers, and ground vehicles. These panels integrate multifunction displays, tactile switches, and intuitive controls to enable pilots and operators to manage complex avionics, weapons systems, and mission data seamlessly. Evolving from legacy analog designs, contemporary UFCs leverage ruggedized touchscreens, customizable layouts, and voice-activated interfaces to enhance situational awareness amid high-threat environments.

The market for defense UFCs is propelled by the global push toward next-generation fighter jets, unmanned aerial systems, and multi-domain operations. Manufacturers focus on modularity to support rapid upgrades, ensuring compatibility with evolving sensor fusion and augmented reality overlays. Emphasis on cybersecurity fortifies these panels against electronic warfare threats, while lightweight composites reduce platform payloads. As defense forces prioritize operator efficiency and reduced cognitive load, UFCs emerge as pivotal enablers of networked warfare, bridging human decision-making with autonomous systems in contested battlespaces.

Technology Impact in Defense Up-Front Control Panels (UFC) Market

Advancements in display technologies profoundly shape the Defense UFC market, with high-resolution active-matrix liquid crystal displays (AMLCD) and organic light-emitting diode (OLED) screens delivering superior brightness, contrast, and wide viewing angles essential for daylight readability in dynamic cockpits. Touch-enabled surfaces, augmented by haptic feedback and gesture recognition, minimize glove-compatible interactions, accelerating command execution during high-G maneuvers.

Integration of artificial intelligence algorithms enables predictive interfaces that anticipate operator needs, auto-populating critical data from fused sensor feeds. Fiber-optic backplanes and gallium nitride (GaN)-based processors boost data throughput and thermal resilience, supporting real-time processing of hyperspectral imagery and electronic warfare signals. Meanwhile, open-system architectures like Future Airborne Capability Environment (FACE) promote software portability, slashing integration costs across platforms.

These innovations not only elevate mission effectiveness but also drive lifecycle extensibility, allowing legacy aircraft to incorporate cutting-edge capabilities without full overhauls. Cybersecurity enhancements, including zero-trust models and quantum-resistant encryption, safeguard against adversarial intrusions, ensuring UFCs remain reliable nodes in joint all-domain command structures.

Key Drivers in Defense Up-Front Control Panels (UFC) Market

Several forces propel the Defense UFC market forward. Foremost is the imperative for enhanced pilot ergonomics and reduced workload, as modern multi-role platforms demand intuitive controls to manage simultaneous air-to-air, air-to-ground, and electronic attack missions. This spurs demand for reconfigurable panels that adapt to diverse roles via software-defined interfaces.

Geopolitical tensions and the rise of peer adversaries accelerate procurement of advanced fighters and loyal wingman drones, necessitating UFCs with seamless integration into tactical data links and collaborative combat aircraft ecosystems. Budgetary pressures favor modular, upgradeable designs that extend platform service life, minimizing sustainment costs through commercial-off-the-shelf components hardened for military specs.

Sustainability mandates push for low-power electronics and recyclable materials, aligning with green procurement policies. Supply chain resilience, bolstered by domestic manufacturing incentives, counters vulnerabilities exposed by recent disruptions. Finally, interoperability standards from allied coalitions drive commonality, enabling shared logistics and training across NATO and Indo-Pacific partners, solidifying UFCs as linchpins of coalition operations.

Regional Trends in Defense Up-Front Control Panels (UFC) Market

North America dominates through sustained investments in fifth-generation fighters and next-gen air dominance programs, emphasizing UFCs with AI-driven interfaces and open mission systems for rapid capability insertion. Europe follows, with collaborative initiatives fostering standardized panels across multinational combat aircraft, prioritizing electromagnetic pulse hardening and augmented reality overlays.

The Asia-Pacific region surges amid territorial disputes, as nations indigenize production to outfit regional fighters and unmanned systems with domestically sourced, cyber-secure UFCs tailored for littoral operations. Middle Eastern markets focus on retrofit programs for legacy fleets, integrating touch-enabled panels to bridge generational gaps while enhancing beyond-visual-range engagement.

Emerging trends highlight supply chain diversification, with secondary suppliers in India and South Korea gaining traction via offset agreements. Export controls shape dynamics, favoring allies with aligned standards. Overall, regional priorities converge on resilience against electronic warfare, driving innovations in self-healing displays and mesh-networked redundancies to sustain command in denied environments.

Key Defense Up-Front Control Panels (UFC) Market Programs

Prominent programs underscore the Defense UFC market's vitality. Leading efforts center on advanced fighter jets, where next-generation cockpits feature glass-panel architectures with fully integrated UFCs, consolidating navigation, communication, and fire control into unified touch interfaces for pilot-centric operations.

Naval aviation initiatives equip carrier-based strike platforms with maritime-hardened UFCs, incorporating saltwater-resistant enclosures and night-vision compatible displays to support carrier air wing integration. Unmanned systems programs embed miniaturized UFC variants in ground control stations, enabling remote operators to orchestrate swarms via intuitive multi-touch gestures.

Army rotary-wing upgrades retrofit tactical helicopters with helmet-mounted cueing-linked panels, enhancing nap-of-the-earth missions through predictive symbology. International collaborations, such as trilateral fighter developments, standardize UFC profiles for interoperability, incorporating voice commands and biometric authentication.

These programs emphasize digital engineering for accelerated prototyping, with virtual twinning simulating human factors pre-hardware. Industry primes partner with specialists to deliver scalable solutions, cementing UFCs as foundational to future force designs.

Table of Contents

Defense Up-Front Control Panels (UFC) Market - Table of Contents

Defense Up-Front Control Panels (UFC) Market Report Definition

Defense Up-Front Control Panels (UFC) Market Segmentation

By Platform

By Interface Type

By Primary Function

Defense Up-Front Control Panels (UFC) Market Analysis for next 10 Years

The 10-year Defense Up-Front Control Panels (UFC) Market analysis would give a detailed overview of Defense Up-Front Control Panels (UFC) Market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Defense Up-Front Control Panels (UFC) Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Defense Up-Front Control Panels (UFC) Market Forecast

The 10-year Defense Up-Front Control Panels (UFC) Market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Defense Up-Front Control Panels (UFC) Market Trends & Forecast

The regional counter drone market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Defense Up-Front Control Panels (UFC) Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Defense Up-Front Control Panels (UFC) Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Defense Up-Front Control Panels (UFC) Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports

List of Tables

- Table 1: 10 Year Market Outlook, 2026-2036

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, APAC

- Table 12: Restraints, Impact Analysis, APAC

- Table 13: Challenges, Impact Analysis, APAC

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Region, 2026-2036

- Table 18: Scenario Analysis, Scenario 1, By Platform, 2026-2036

- Table 19: Scenario Analysis, Scenario 1, By Control Type, 2026-2036

- Table 20: Scenario Analysis, Scenario 2, By Region, 2026-2036

- Table 21: Scenario Analysis, Scenario 2, By Platform, 2026-2036

- Table 22: Scenario Analysis, Scenario 2, By Control Type, 2026-2036

List of Figures

- Figure 1: Global Defense Up-Front Control Panels (UFC) Market Forecast, 2026-2036

- Figure 2: Global Defense Up-Front Control Panels (UFC) Market Forecast, By Region, 2026-2036

- Figure 3: Global Defense Up-Front Control Panels (UFC) Market Forecast, By Platform, 2026-2036

- Figure 4: Global Defense Up-Front Control Panels (UFC) Market Forecast, By Control Type, 2026-2036

- Figure 5: North America, Defense Up-Front Control Panels (UFC) Market, Market Forecast, 2026-2036

- Figure 6: Europe, Defense Up-Front Control Panels (UFC) Market, Market Forecast, 2026-2036

- Figure 7: Middle East, Defense Up-Front Control Panels (UFC) Market, Market Forecast, 2026-2036

- Figure 8: APAC, Defense Up-Front Control Panels (UFC) Market, Market Forecast, 2026-2036

- Figure 9: South America, Defense Up-Front Control Panels (UFC) Market, Market Forecast, 2026-2036

- Figure 10: United States, Defense Up-Front Control Panels (UFC) Market, Region Maturation, 2026-2036

- Figure 11: United States, Defense Up-Front Control Panels (UFC) Market, Market Forecast, 2026-2036

- Figure 12: Canada, Defense Up-Front Control Panels (UFC) Market, Region Maturation, 2026-2036

- Figure 13: Canada, Defense Up-Front Control Panels (UFC) Market, Market Forecast, 2026-2036

- Figure 14: Italy, Defense Up-Front Control Panels (UFC) Market, Region Maturation, 2026-2036

- Figure 15: Italy, Defense Up-Front Control Panels (UFC) Market, Market Forecast, 2026-2036

- Figure 16: France, Defense Up-Front Control Panels (UFC) Market, Region Maturation, 2026-2036

- Figure 17: France, Defense Up-Front Control Panels (UFC) Market, Market Forecast, 2026-2036

- Figure 18: Germany, Defense Up-Front Control Panels (UFC) Market, Region Maturation, 2026-2036

- Figure 19: Germany, Defense Up-Front Control Panels (UFC) Market, Market Forecast, 2026-2036

- Figure 20: Netherlands, Defense Up-Front Control Panels (UFC) Market, Region Maturation, 2026-2036

- Figure 21: Netherlands, Defense Up-Front Control Panels (UFC) Market, Market Forecast, 2026-2036

- Figure 22: Belgium, Defense Up-Front Control Panels (UFC) Market, Region Maturation, 2026-2036

- Figure 23: Belgium, Defense Up-Front Control Panels (UFC) Market, Market Forecast, 2026-2036

- Figure 24: Spain, Defense Up-Front Control Panels (UFC) Market, Region Maturation, 2026-2036

- Figure 25: Spain, Defense Up-Front Control Panels (UFC) Market, Market Forecast, 2026-2036

- Figure 26: Sweden, Defense Up-Front Control Panels (UFC) Market, Region Maturation, 2026-2036

- Figure 27: Sweden, Defense Up-Front Control Panels (UFC) Market, Market Forecast, 2026-2036

- Figure 28: Brazil, Defense Up-Front Control Panels (UFC) Market, Region Maturation, 2026-2036

- Figure 29: Brazil, Defense Up-Front Control Panels (UFC) Market, Market Forecast, 2026-2036

- Figure 30: Australia, Defense Up-Front Control Panels (UFC) Market, Region Maturation, 2026-2036

- Figure 31: Australia, Defense Up-Front Control Panels (UFC) Market, Market Forecast, 2026-2036

- Figure 32: India, Defense Up-Front Control Panels (UFC) Market, Region Maturation, 2026-2036

- Figure 33: India, Defense Up-Front Control Panels (UFC) Market, Market Forecast, 2026-2036

- Figure 34: China, Defense Up-Front Control Panels (UFC) Market, Region Maturation, 2026-2036

- Figure 35: China, Defense Up-Front Control Panels (UFC) Market, Market Forecast, 2026-2036

- Figure 36: Saudi Arabia, Defense Up-Front Control Panels (UFC) Market, Region Maturation, 2026-2036

- Figure 37: Saudi Arabia, Defense Up-Front Control Panels (UFC) Market, Market Forecast, 2026-2036

- Figure 38: South Korea, Defense Up-Front Control Panels (UFC) Market, Region Maturation, 2026-2036

- Figure 39: South Korea, Defense Up-Front Control Panels (UFC) Market, Market Forecast, 2026-2036

- Figure 40: Japan, Defense Up-Front Control Panels (UFC) Market, Region Maturation, 2026-2036

- Figure 41: Japan, Defense Up-Front Control Panels (UFC) Market, Market Forecast, 2026-2036

- Figure 42: Malaysia, Defense Up-Front Control Panels (UFC) Market, Region Maturation, 2026-2036

- Figure 43: Malaysia, Defense Up-Front Control Panels (UFC) Market, Market Forecast, 2026-2036

- Figure 44: Singapore, Defense Up-Front Control Panels (UFC) Market, Region Maturation, 2026-2036

- Figure 45: Singapore, Defense Up-Front Control Panels (UFC) Market, Market Forecast, 2026-2036

- Figure 46: United Kingdom, Defense Up-Front Control Panels (UFC) Market, Region Maturation, 2026-2036

- Figure 47: United Kingdom, Defense Up-Front Control Panels (UFC) Market, Market Forecast, 2026-2036

- Figure 48: Opportunity Analysis, Defense Up-Front Control Panels (UFC) Market, By Region (Cumulative Market), 2026-2036

- Figure 49: Opportunity Analysis, Defense Up-Front Control Panels (UFC) Market, By Region (CAGR), 2026-2036

- Figure 50: Opportunity Analysis, Defense Up-Front Control Panels (UFC) Market, By Platform (Cumulative Market), 2026-2036

- Figure 51: Opportunity Analysis, Defense Up-Front Control Panels (UFC) Market, By Platform (CAGR), 2026-2036

- Figure 52: Opportunity Analysis, Defense Up-Front Control Panels (UFC) Market, By Control Type (Cumulative Market), 2026-2036

- Figure 53: Opportunity Analysis, Defense Up-Front Control Panels (UFC) Market, By Control Type (CAGR), 2026-2036

- Figure 54: Scenario Analysis, Defense Up-Front Control Panels (UFC) Market, Cumulative Market, 2026-2036

- Figure 55: Scenario Analysis, Defense Up-Front Control Panels (UFC) Market, Global Market, 2026-2036

- Figure 56: Scenario 1, Defense Up-Front Control Panels (UFC) Market, Total Market, 2026-2036

- Figure 57: Scenario 1, Defense Up-Front Control Panels (UFC) Market, By Region, 2026-2036

- Figure 58: Scenario 1, Defense Up-Front Control Panels (UFC) Market, By Platform, 2026-2036

- Figure 59: Scenario 1, Defense Up-Front Control Panels (UFC) Market, By Control Type, 2026-2036

- Figure 60: Scenario 2, Defense Up-Front Control Panels (UFC) Market, Total Market, 2026-2036

- Figure 61: Scenario 2, Defense Up-Front Control Panels (UFC) Market, By Region, 2026-2036

- Figure 62: Scenario 2, Defense Up-Front Control Panels (UFC) Market, By Platform, 2026-2036

- Figure 63: Scenario 2, Defense Up-Front Control Panels (UFC) Market, By Control Type, 2026-2036

- Figure 64: Company Benchmark, Defense Up-Front Control Panels (UFC) Market, 2026-2036