PUBLISHER: Aviation & Defense Market Reports (A&D) | PRODUCT CODE: 2009455

PUBLISHER: Aviation & Defense Market Reports (A&D) | PRODUCT CODE: 2009455

Global Defense Aircraft Wings Structure Market 2026-2036

Global Defense Aircraft Wings Structure Market

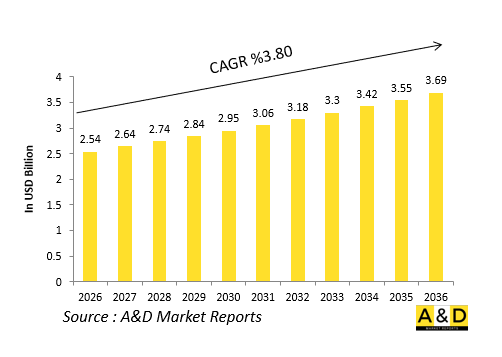

The Global Defense Aircraft Wings Structure Market is estimated at USD 2.54 billion in 2026, projected to grow to USD 3.69 billion by 2036 at a Compound Annual Growth Rate (CAGR) of 3.80% over the forecast period 2026-2036.

Introduction:

The global defense aircraft wings structure market focuses on the engineering and production of high-performance wings critical for military aviation. These structures provide lift, maneuverability, and stability, integrating spars, skins, ribs, and control surfaces to withstand aerodynamic loads, g-forces, and weapon recoil. Advanced materials like carbon composites, titanium alloys, and morphing technologies enable slimmer profiles for stealth, higher speeds, and extended ranges. Suppliers range from tier-one integrators to specialists in variable-sweep mechanisms and foldable designs for carrier operations. Market momentum arises from procurement of fifth- and sixth-generation fighters, unmanned systems, and rotary-wing upgrades. Emphasis on fuel efficiency, payload versatility, and sensor embedding drives innovation. This sector underpins air dominance strategies, with wings evolving into multifunctional platforms housing fuel tanks, electronics, and conformal antennas for modern battlefields.

Technology Impact in Defense Aircraft Wings Structure Market

Technologies are transforming the defense aircraft wings structure market, enhancing performance and adaptability. Carbon fiber composites deliver exceptional stiffness and fatigue resistance, enabling thinner, lighter wings that boost agility without sacrificing strength. Active morphing surfaces, using smart actuators and shape-memory alloys, allow real-time adjustments for optimal lift across flight regimes. Additive manufacturing fabricates intricate internal lattices, reducing weight and enabling rapid iteration. Embedded fiber optics and piezoelectric sensors enable structural health monitoring, predicting cracks from combat stresses. Blended-wing designs integrate propulsion and stealth features, minimizing drag. AI-optimized aerodynamics via computational fluid dynamics refine airfoil shapes for hypersonic and supercruise capabilities. Automation in layup and curing processes scales production for high-volume programs. These breakthroughs address challenges like flutter suppression and ice accretion, positioning wings as dynamic systems that elevate mission effectiveness and aircraft longevity.

Key Drivers in Defense Aircraft Wings Structure Market

Key drivers accelerate the defense aircraft wings structure market amid evolving threats. Modernization of legacy fleets demands upgraded wings with enhanced lift for heavier armaments and extended loiter times. Geostrategic rivalries fuel investments in agile, multirole platforms with variable geometry for diverse missions. Sustainability goals promote recyclable composites and aerodynamic efficiencies to lower lifecycle emissions. Supply chain vulnerabilities spur localized manufacturing and resilient materials sourcing. Proliferation of loyal wingman drones requires compact, foldable wings for mothership integration. Demands for low-observability drive radar-absorbent structures and serrated edges. Digital engineering tools enable virtual testing, compressing development cycles. International partnerships facilitate co-development, sharing wing tech across alliances. Economic factors emphasize affordable scalability through modular designs. Collectively, these propel a market prioritizing survivability, versatility, and rapid deployment in contested airspace.

Regional Trends in Defense Aircraft Wings Structure Market

Regional trends in the defense aircraft wings structure market highlight strategic divergences. North America spearheads innovation in adaptive wings and composites for stealth fighters and strategic bombers. Europe leverages joint ventures for swing-wing transports and eurofighter enhancements, stressing interoperability. Asia-Pacific ramps up indigenous capabilities, developing high-maneuverability wings for regional patrols and carrier-based jets. Middle Eastern nations focus on desert-hardened structures with anti-icing and dust-resistant coatings. In Africa and Latin America, trends favor rugged, cost-effective wings for counter-insurgency and maritime surveillance. Localization efforts build domestic supply chains, reducing foreign dependency. Export-oriented production adapts designs to client specifications, like tropical corrosion resistance. Collaborative R&D hubs emerge, fostering tech transfer. These patterns reflect tailored responses to local threats, budgets, and industrial maturity, shaping a fragmented yet interconnected global ecosystem.

Key Defense Aircraft Wings Structure Market Programs

Landmark programs anchor the defense aircraft wings structure market, pioneering next-era capabilities. Sixth-generation fighter efforts feature folding, adaptive wings with embedded weapons bays for air superiority. Loyal wingman initiatives deploy semi-autonomous drones with lightweight composite spars for teaming with manned jets. Rotary-wing upgrades incorporate rigid rotor blades evolving into advanced wing-like structures for tiltrotor versatility. Hypersonic demonstrator projects test heat-resistant wings using ceramic matrix composites. Multirole bomber refreshes integrate conformal fuel tanks within blended wings for global reach. Carrier aviation programs emphasize reinforced, folding mechanisms for compact storage and high-g launches. These efforts validate morphing tech, digital twins, and automated assembly. Industry teams collaborate on qualification testing for extreme loads. Success metrics include seamless integration with avionics and propulsion, redefining wings as intelligent, mission-reconfigurable components for networked warfare.

Table of Contents

Defense Aircraft Wings Structure Market - Table of Contents

Defense Aircraft Wings Structure Market Report Definition

Defense Aircraft Wings Structure Market Segmentation

By Region

By Platform

By By Material

By Component

By Wing Type

By Technology

Defense Aircraft Wings Structure Market Analysis for next 10 Years

The 10-year Defense Aircraft Wings Structure Market analysis would give a detailed overview of Defense Aircraft Wings Structure Market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Defense Aircraft Wings Structure Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Defense Aircraft Wings Structure Market Forecast

The 10-year Defense Aircraft Wings Structure Market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Defense Aircraft Wings Structure Market Trends & Forecast

The regional counter drone market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Defense Aircraft Wings Structure Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Defense Aircraft Wings Structure Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Defense Aircraft Wings Structure Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports

List of Tables

- Table 1: 10 Year Market Outlook, 2026-2036

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, APAC

- Table 12: Restraints, Impact Analysis, APAC

- Table 13: Challenges, Impact Analysis, APAC

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Region, 2026-2036

- Table 18: Scenario Analysis, Scenario 1, By Platform, 2026-2036

- Table 19: Scenario Analysis, Scenario 1, By Material, 2026-2036

- Table 20: Scenario Analysis, Scenario 2, By Region, 2026-2036

- Table 21: Scenario Analysis, Scenario 2, By Platform, 2026-2036

- Table 22: Scenario Analysis, Scenario 2, By Material, 2026-2036

List of Figures

- Figure 1: Global Defense Aircraft Wings Structure Market Forecast, 2026-2036

- Figure 2: Global Defense Aircraft Wings Structure Market Forecast, By Region, 2026-2036

- Figure 3: Global Defense Aircraft Wings Structure Market Forecast, By Platform, 2026-2036

- Figure 4: Global Defense Aircraft Wings Structure Market Forecast, By Material, 2026-2036

- Figure 5: North America, Defense Aircraft Wings Structure Market, Market Forecast, 2026-2036

- Figure 6: Europe, Defense Aircraft Wings Structure Market, Market Forecast, 2026-2036

- Figure 7: Middle East, Defense Aircraft Wings Structure Market, Market Forecast, 2026-2036

- Figure 8: APAC, Defense Aircraft Wings Structure Market, Market Forecast, 2026-2036

- Figure 9: South America, Defense Aircraft Wings Structure Market, Market Forecast, 2026-2036

- Figure 10: United States, Defense Aircraft Wings Structure Market, Region Maturation, 2026-2036

- Figure 11: United States, Defense Aircraft Wings Structure Market, Market Forecast, 2026-2036

- Figure 12: Canada, Defense Aircraft Wings Structure Market, Region Maturation, 2026-2036

- Figure 13: Canada, Defense Aircraft Wings Structure Market, Market Forecast, 2026-2036

- Figure 14: Italy, Defense Aircraft Wings Structure Market, Region Maturation, 2026-2036

- Figure 15: Italy, Defense Aircraft Wings Structure Market, Market Forecast, 2026-2036

- Figure 16: France, Defense Aircraft Wings Structure Market, Region Maturation, 2026-2036

- Figure 17: France, Defense Aircraft Wings Structure Market, Market Forecast, 2026-2036

- Figure 18: Germany, Defense Aircraft Wings Structure Market, Region Maturation, 2026-2036

- Figure 19: Germany, Defense Aircraft Wings Structure Market, Market Forecast, 2026-2036

- Figure 20: Netherlands, Defense Aircraft Wings Structure Market, Region Maturation, 2026-2036

- Figure 21: Netherlands, Defense Aircraft Wings Structure Market, Market Forecast, 2026-2036

- Figure 22: Belgium, Defense Aircraft Wings Structure Market, Region Maturation, 2026-2036

- Figure 23: Belgium, Defense Aircraft Wings Structure Market, Market Forecast, 2026-2036

- Figure 24: Spain, Defense Aircraft Wings Structure Market, Region Maturation, 2026-2036

- Figure 25: Spain, Defense Aircraft Wings Structure Market, Market Forecast, 2026-2036

- Figure 26: Sweden, Defense Aircraft Wings Structure Market, Region Maturation, 2026-2036

- Figure 27: Sweden, Defense Aircraft Wings Structure Market, Market Forecast, 2026-2036

- Figure 28: Brazil, Defense Aircraft Wings Structure Market, Region Maturation, 2026-2036

- Figure 29: Brazil, Defense Aircraft Wings Structure Market, Market Forecast, 2026-2036

- Figure 30: Australia, Defense Aircraft Wings Structure Market, Region Maturation, 2026-2036

- Figure 31: Australia, Defense Aircraft Wings Structure Market, Market Forecast, 2026-2036

- Figure 32: India, Defense Aircraft Wings Structure Market, Region Maturation, 2026-2036

- Figure 33: India, Defense Aircraft Wings Structure Market, Market Forecast, 2026-2036

- Figure 34: China, Defense Aircraft Wings Structure Market, Region Maturation, 2026-2036

- Figure 35: China, Defense Aircraft Wings Structure Market, Market Forecast, 2026-2036

- Figure 36: Saudi Arabia, Defense Aircraft Wings Structure Market, Region Maturation, 2026-2036

- Figure 37: Saudi Arabia, Defense Aircraft Wings Structure Market, Market Forecast, 2026-2036

- Figure 38: South Korea, Defense Aircraft Wings Structure Market, Region Maturation, 2026-2036

- Figure 39: South Korea, Defense Aircraft Wings Structure Market, Market Forecast, 2026-2036

- Figure 40: Japan, Defense Aircraft Wings Structure Market, Region Maturation, 2026-2036

- Figure 41: Japan, Defense Aircraft Wings Structure Market, Market Forecast, 2026-2036

- Figure 42: Malaysia, Defense Aircraft Wings Structure Market, Region Maturation, 2026-2036

- Figure 43: Malaysia, Defense Aircraft Wings Structure Market, Market Forecast, 2026-2036

- Figure 44: Singapore, Defense Aircraft Wings Structure Market, Region Maturation, 2026-2036

- Figure 45: Singapore, Defense Aircraft Wings Structure Market, Market Forecast, 2026-2036

- Figure 46: United Kingdom, Defense Aircraft Wings Structure Market, Region Maturation, 2026-2036

- Figure 47: United Kingdom, Defense Aircraft Wings Structure Market, Market Forecast, 2026-2036

- Figure 48: Opportunity Analysis, Defense Aircraft Wings Structure Market, By Region (Cumulative Market), 2026-2036

- Figure 49: Opportunity Analysis, Defense Aircraft Wings Structure Market, By Region (CAGR), 2026-2036

- Figure 50: Opportunity Analysis, Defense Aircraft Wings Structure Market, By Platform (Cumulative Market), 2026-2036

- Figure 51: Opportunity Analysis, Defense Aircraft Wings Structure Market, By Platform (CAGR), 2026-2036

- Figure 52: Opportunity Analysis, Defense Aircraft Wings Structure Market, By Material(Cumulative Market), 2026-2036

- Figure 53: Opportunity Analysis, Defense Aircraft Wings Structure Market, By Material(CAGR), 2026-2036

- Figure 54: Scenario Analysis, Defense Aircraft Wings Structure Market, Cumulative Market, 2026-2036

- Figure 55: Scenario Analysis, Defense Aircraft Wings Structure Market, Global Market, 2026-2036

- Figure 56: Scenario 1, Defense Aircraft Wings Structure Market, Total Market, 2026-2036

- Figure 57: Scenario 1, Defense Aircraft Wings Structure Market, By Region, 2026-2036

- Figure 58: Scenario 1, Defense Aircraft Wings Structure Market, By Platform, 2026-2036

- Figure 59: Scenario 1, Defense Aircraft Wings Structure Market, By Material, 2026-2036

- Figure 60: Scenario 2, Defense Aircraft Wings Structure Market, Total Market, 2026-2036

- Figure 61: Scenario 2, Defense Aircraft Wings Structure Market, By Region, 2026-2036

- Figure 62: Scenario 2, Defense Aircraft Wings Structure Market, By Platform, 2026-2036

- Figure 63: Scenario 2, Defense Aircraft Wings Structure Market, By Material, 2026-2036

- Figure 64: Company Benchmark, Defense Aircraft Wings Structure Market, 2026-2036