PUBLISHER: Aviation & Defense Market Reports (A&D) | PRODUCT CODE: 2009456

PUBLISHER: Aviation & Defense Market Reports (A&D) | PRODUCT CODE: 2009456

Global Defense Fighter Aircraft Cockpit Canopy Market 2026-2036

Global Defense Fighter Aircraft Cockpit Canopy Market

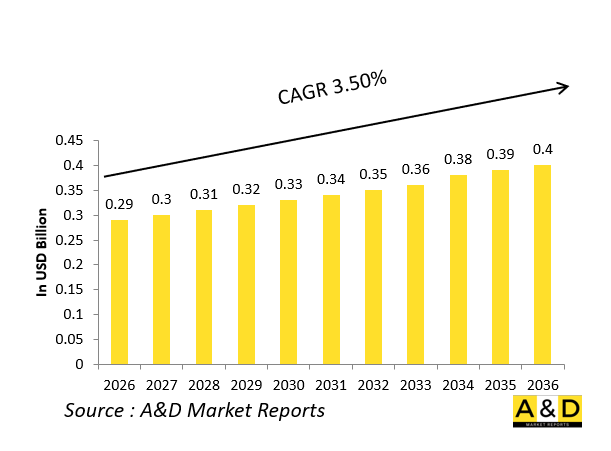

The Global Defense Fighter Aircraft Cockpit Canopy Market is estimated at USD 0.29 billion in 2026, projected to grow to USD 0.4 billion by 2036 at a Compound Annual Growth Rate (CAGR) of 3.50% over the forecast period 2026-2036.

Introduction:

The global defense fighter aircraft cockpit canopy market involves specialized transparent enclosures that shield pilots while enabling unobstructed visibility for combat missions. Crafted from advanced polycarbonate, acrylics, and glass laminates, these structures resist bird strikes, ballistic impacts, and extreme pressures at high altitudes. Integrated features like gold coatings for infrared reflection, heads-up displays, and anti-glare treatments enhance situational awareness. Suppliers specialize in molding, coating, and ejection-compatible designs for supersonic jets and advanced trainers. Market expansion ties to new fighter procurements, fleet upgrades, and pilot survivability mandates. Canopies evolve into multifunctional elements, embedding sensors, HUD projectors, and solar cells. This niche sector balances optical clarity, durability, and stealth, proving essential for air-to-air superiority and precision strikes in contested environments.

Technology Impact in Defense Aircraft Fighter Cockpit Canopy Market

Technologies revolutionize the defense fighter aircraft cockpit canopy market, prioritizing pilot protection and performance. Self-healing polymers repair micro-cracks from sand abrasion or laser threats autonomously. Nanocoatings provide hydrophobic, anti-fog, and scratch-resistant surfaces, maintaining clarity in harsh conditions. Embedded electrochromic layers enable variable tinting for glare control and signature management. Fiber-reinforced composites boost impact resistance without added weight, supporting high-speed ejections. Additive manufacturing allows custom curvatures and integrated mounting points for helmet-mounted displays. Multispectral transparency accommodates IR and NVG compatibility. Acoustic damping layers reduce cockpit noise for sustained pilot focus. Digital twins simulate bird-strike dynamics and thermal stresses during design. These innovations extend canopy lifespan, integrate with augmented reality visors, and minimize radar reflectivity, transforming canopies into smart interfaces that amplify fighter lethality and endurance.

Key Drivers in Defense Fighter Aircraft Cockpit Canopy Market

Primary drivers energize the defense fighter aircraft cockpit canopy market. Surge in fifth- and sixth-generation fighter programs demands low-observability canopies with radar-absorbent edges. Pilot safety regulations mandate enhanced bird-strike and fragmentation resistance amid denser air traffic. High-intensity training exposes canopies to repeated stress, spurring durable replacements. Stealth imperatives require IR-suppressing coatings to evade heat-seekers. Supply chain localization counters vulnerabilities in specialty polymers. Augmented reality cockpits integrate canopy-projected symbology, necessitating precise optical substrates. Export demands adapt designs for diverse climates, from arctic icing to desert sandblasting. Sustainment contracts favor recyclable materials aligning with green procurement. Cybersecurity for embedded electronics prevents spoofing vulnerabilities. These catalysts focus on blending transparency with armor-like resilience, ensuring canopies support extended missions in peer-level conflicts.

Regional Trends in Defense Fighter Aircraft Cockpit Canopy Market

Regional trends in the defense fighter aircraft cockpit canopy market align with fighter modernization agendas. North America leads in polycarbonate innovations and HUD-integrated designs for stealth platforms. Europe advances multilayer laminates through collaborative upgrades for multirole jets. Asia-Pacific emphasizes cost-effective molding for indigenous fifth-gen fighters and export variants. Middle East prioritizes solar-reflective coatings for high-heat operations. In Eastern Europe and South Asia, trends favor retrofit kits enhancing legacy canopy durability. Domestic production ramps up to secure strategic supplies amid trade tensions. Customization for helmet cueing systems gains traction in allied training programs. Harsh environment adaptations-like UV protection for equatorial bases-shape specifications. Tech transfer partnerships build local expertise. This geography reflects a push toward resilient, mission-tailored canopies supporting regional airpower projections.

Key Defense Fighter Aircraft Cockpit Canopy Market Programs

Pivotal programs define the defense fighter aircraft cockpit canopy market's trajectory. Next-generation air superiority fighters deploy frameless, bird-safe canopies with electrochromic dimming for sensor fusion. Light combat aircraft initiatives integrate wide-angle transparency for drone teaming. Trainer jet overhauls feature impact-resistant replacements with NVG-friendly tints. Export-oriented multirole upgrades embed canopy HUDs for global customers. Hypersonic test platforms pioneer heat-mirror coatings enduring plasma sheaths. Legacy fourth-gen sustainment contracts supply modular canopies for rapid field swaps. These efforts rigorously test under live-fire, high-G, and environmental extremes. Collaborations validate ejection sequencing and optical fidelity. Emphasis on modularity allows seamless avionics upgrades. Such programs position canopies as critical enablers of pilot-centric cockpits, fusing visibility, protection, and digital augmentation for dominance in networked aerial warfare.

Table of Contents

Defense Fighter Aircraft Cockpit Canopy Market - Table of Contents

Defense Fighter Aircraft Cockpit Canopy Market Report Definition

Defense Fighter Aircraft Cockpit Canopy Market Segmentation

By Region

By Platform

By Material

By Canopy Type

By Technology

By Aircraft Generation

Defense Fighter Aircraft Cockpit Canopy Market Analysis for next 10 Years

The 10-year Defense Fighter Aircraft Cockpit Canopy Market analysis would give a detailed overview of Defense Fighter Aircraft Cockpit Canopy Market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Defense Fighter Aircraft Cockpit Canopy Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Defense Fighter Aircraft Cockpit Canopy Market Forecast

The 10-year Defense Fighter Aircraft Cockpit Canopy Market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Defense Fighter Aircraft Cockpit Canopy Market Trends & Forecast

The regional counter drone market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Defense Fighter Aircraft Cockpit Canopy Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Defense Fighter Aircraft Cockpit Canopy Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Defense Fighter Aircraft Cockpit Canopy Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports

List of Tables

- Table 1: 10 Year Market Outlook, 2026-2036

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, APAC

- Table 12: Restraints, Impact Analysis, APAC

- Table 13: Challenges, Impact Analysis, APAC

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Region, 2026-2036

- Table 18: Scenario Analysis, Scenario 1, By Platform, 2026-2036

- Table 19: Scenario Analysis, Scenario 1, By Material, 2026-2036

- Table 20: Scenario Analysis, Scenario 2, By Region, 2026-2036

- Table 21: Scenario Analysis, Scenario 2, By Platform, 2026-2036

- Table 22: Scenario Analysis, Scenario 2, By Material, 2026-2036

List of Figures

- Figure 1: Global Defense Fighter Aircraft Cockpit Canopy Market Forecast, 2026-2036

- Figure 2: Global Defense Fighter Aircraft Cockpit Canopy Market Forecast, By Region, 2026-2036

- Figure 3: Global Defense Fighter Aircraft Cockpit Canopy Market Forecast, By Platform, 2026-2036

- Figure 4: Global Defense Fighter Aircraft Cockpit Canopy Market Forecast, By Material, 2026-2036

- Figure 5: North America, Defense Fighter Aircraft Cockpit Canopy Market, Market Forecast, 2026-2036

- Figure 6: Europe, Defense Fighter Aircraft Cockpit Canopy Market, Market Forecast, 2026-2036

- Figure 7: Middle East, Defense Fighter Aircraft Cockpit Canopy Market, Market Forecast, 2026-2036

- Figure 8: APAC, Defense Fighter Aircraft Cockpit Canopy Market, Market Forecast, 2026-2036

- Figure 9: South America, Defense Fighter Aircraft Cockpit Canopy Market, Market Forecast, 2026-2036

- Figure 10: United States, Defense Fighter Aircraft Cockpit Canopy Market, Region Maturation, 2026-2036

- Figure 11: United States, Defense Fighter Aircraft Cockpit Canopy Market, Market Forecast, 2026-2036

- Figure 12: Canada, Defense Fighter Aircraft Cockpit Canopy Market, Region Maturation, 2026-2036

- Figure 13: Canada, Defense Fighter Aircraft Cockpit Canopy Market, Market Forecast, 2026-2036

- Figure 14: Italy, Defense Fighter Aircraft Cockpit Canopy Market, Region Maturation, 2026-2036

- Figure 15: Italy, Defense Fighter Aircraft Cockpit Canopy Market, Market Forecast, 2026-2036

- Figure 16: France, Defense Fighter Aircraft Cockpit Canopy Market, Region Maturation, 2026-2036

- Figure 17: France, Defense Fighter Aircraft Cockpit Canopy Market, Market Forecast, 2026-2036

- Figure 18: Germany, Defense Fighter Aircraft Cockpit Canopy Market, Region Maturation, 2026-2036

- Figure 19: Germany, Defense Fighter Aircraft Cockpit Canopy Market, Market Forecast, 2026-2036

- Figure 20: Netherlands, Defense Fighter Aircraft Cockpit Canopy Market, Region Maturation, 2026-2036

- Figure 21: Netherlands, Defense Fighter Aircraft Cockpit Canopy Market, Market Forecast, 2026-2036

- Figure 22: Belgium, Defense Fighter Aircraft Cockpit Canopy Market, Region Maturation, 2026-2036

- Figure 23: Belgium, Defense Fighter Aircraft Cockpit Canopy Market, Market Forecast, 2026-2036

- Figure 24: Spain, Defense Fighter Aircraft Cockpit Canopy Market, Region Maturation, 2026-2036

- Figure 25: Spain, Defense Fighter Aircraft Cockpit Canopy Market, Market Forecast, 2026-2036

- Figure 26: Sweden, Defense Fighter Aircraft Cockpit Canopy Market, Region Maturation, 2026-2036

- Figure 27: Sweden, Defense Fighter Aircraft Cockpit Canopy Market, Market Forecast, 2026-2036

- Figure 28: Brazil, Defense Fighter Aircraft Cockpit Canopy Market, Region Maturation, 2026-2036

- Figure 29: Brazil, Defense Fighter Aircraft Cockpit Canopy Market, Market Forecast, 2026-2036

- Figure 30: Australia, Defense Fighter Aircraft Cockpit Canopy Market, Region Maturation, 2026-2036

- Figure 31: Australia, Defense Fighter Aircraft Cockpit Canopy Market, Market Forecast, 2026-2036

- Figure 32: India, Defense Fighter Aircraft Cockpit Canopy Market, Region Maturation, 2026-2036

- Figure 33: India, Defense Fighter Aircraft Cockpit Canopy Market, Market Forecast, 2026-2036

- Figure 34: China, Defense Fighter Aircraft Cockpit Canopy Market, Region Maturation, 2026-2036

- Figure 35: China, Defense Fighter Aircraft Cockpit Canopy Market, Market Forecast, 2026-2036

- Figure 36: Saudi Arabia, Defense Fighter Aircraft Cockpit Canopy Market, Region Maturation, 2026-2036

- Figure 37: Saudi Arabia, Defense Fighter Aircraft Cockpit Canopy Market, Market Forecast, 2026-2036

- Figure 38: South Korea, Defense Fighter Aircraft Cockpit Canopy Market, Region Maturation, 2026-2036

- Figure 39: South Korea, Defense Fighter Aircraft Cockpit Canopy Market, Market Forecast, 2026-2036

- Figure 40: Japan, Defense Fighter Aircraft Cockpit Canopy Market, Region Maturation, 2026-2036

- Figure 41: Japan, Defense Fighter Aircraft Cockpit Canopy Market, Market Forecast, 2026-2036

- Figure 42: Malaysia, Defense Fighter Aircraft Cockpit Canopy Market, Region Maturation, 2026-2036

- Figure 43: Malaysia, Defense Fighter Aircraft Cockpit Canopy Market, Market Forecast, 2026-2036

- Figure 44: Singapore, Defense Fighter Aircraft Cockpit Canopy Market, Region Maturation, 2026-2036

- Figure 45: Singapore, Defense Fighter Aircraft Cockpit Canopy Market, Market Forecast, 2026-2036

- Figure 46: United Kingdom, Defense Fighter Aircraft Cockpit Canopy Market, Region Maturation, 2026-2036

- Figure 47: United Kingdom, Defense Fighter Aircraft Cockpit Canopy Market, Market Forecast, 2026-2036

- Figure 48: Opportunity Analysis, Defense Fighter Aircraft Cockpit Canopy Market, By Region (Cumulative Market), 2026-2036

- Figure 49: Opportunity Analysis, Defense Fighter Aircraft Cockpit Canopy Market, By Region (CAGR), 2026-2036

- Figure 50: Opportunity Analysis, Defense Fighter Aircraft Cockpit Canopy Market, By Platform (Cumulative Market), 2026-2036

- Figure 51: Opportunity Analysis, Defense Fighter Aircraft Cockpit Canopy Market, By Platform (CAGR), 2026-2036

- Figure 52: Opportunity Analysis, Defense Fighter Aircraft Cockpit Canopy Market, By Material(Cumulative Market), 2026-2036

- Figure 53: Opportunity Analysis, Defense Fighter Aircraft Cockpit Canopy Market, By Material(CAGR), 2026-2036

- Figure 54: Scenario Analysis, Defense Fighter Aircraft Cockpit Canopy Market, Cumulative Market, 2026-2036

- Figure 55: Scenario Analysis, Defense Fighter Aircraft Cockpit Canopy Market, Global Market, 2026-2036

- Figure 56: Scenario 1, Defense Fighter Aircraft Cockpit Canopy Market, Total Market, 2026-2036

- Figure 57: Scenario 1, Defense Fighter Aircraft Cockpit Canopy Market, By Region, 2026-2036

- Figure 58: Scenario 1, Defense Fighter Aircraft Cockpit Canopy Market, By Platform, 2026-2036

- Figure 59: Scenario 1, Defense Fighter Aircraft Cockpit Canopy Market, By Material, 2026-2036

- Figure 60: Scenario 2, Defense Fighter Aircraft Cockpit Canopy Market, Total Market, 2026-2036

- Figure 61: Scenario 2, Defense Fighter Aircraft Cockpit Canopy Market, By Region, 2026-2036

- Figure 62: Scenario 2, Defense Fighter Aircraft Cockpit Canopy Market, By Platform, 2026-2036

- Figure 63: Scenario 2, Defense Fighter Aircraft Cockpit Canopy Market, By Material, 2026-2036

- Figure 64: Company Benchmark, Defense Fighter Aircraft Cockpit Canopy Market, 2026-2036