PUBLISHER: Bluefield Research | PRODUCT CODE: 1834222

PUBLISHER: Bluefield Research | PRODUCT CODE: 1834222

U.S. Midstream Water for Hydraulic Fracturing: Market Trends, Opportunities, and Forecasts, 2025-2030

Over the last decade, hydraulic fracturing has transformed the U.S. energy landscape, establishing the country as the world's largest producer of oil and gas. By tapping into shale reserves across regions from Pennsylvania to Texas, fracking has become a cornerstone of global energy security. The U.S. now contributes nearly 40% of global oil production and 37% of natural gas production.

Midstream water management, which involves the supply, treatment, recycling, reuse, and disposal of water, is critical to this transformation. Horizontal well completions can extend up to five miles and require over 12 million gallons of water, resulting in unprecedented volumes of produced water. By 2030, the volume of produced water at wellheads is projected to reach 50 million barrels per day, placing additional stress on disposal facilities and fueling regulatory scrutiny, particularly in high-activity regions like the Permian Basin, which spans Texas and New Mexico.

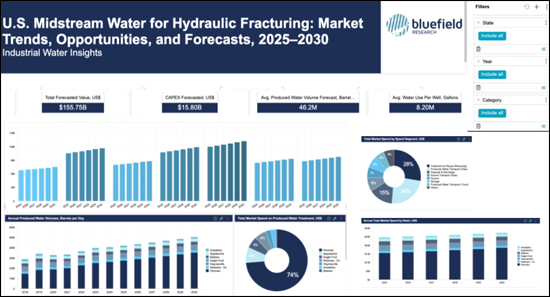

In this evolving context, exploration and production companies and midstream water management players are pursuing more integrated water solutions. Water supply and produced water pipelines are becoming viable alternatives to trucking and produced water recycling is on track to meet over 77% of fracking water demand by 2030. These shifts, accompanied by consolidation efforts such as mergers and acquisitions and partnerships across the water value chain, are reshaping the competitive landscape.

This Insight Report provides a comprehensive analysis of U.S. midstream water management, encompassing market drivers and forecasts, basin-level dynamics, and the strategies of leading players that are influencing the future of oilfield water management.

Report+Data Option

SAMPLE DATA DASHBOARD

Data is a key component to this analysis. Our team has compiled relevant data dashboards.

Industrial Water Market Corporate Subscription seat holders can access related dashboards.

Companies Mentioned:

|

|

Table of Contents

Section 1 - Defining the Oil & Gas Landscape

- Research Methodology and Data Sources

- Key Factors Influencing Midstream Water Management

- Water-Intensive Fracking Makes U.S. the Leading Global Oil Producer

- U.S. Secures Role as Global Supplier of Natural Gas

- Swings in Oil & Gas Prices Shape Strategies

- Horizontal Drilling and Hydraulic Fracturing

- Horizontal Rig Capabilities: Depths and Lengths

- Horizontal Wellbore Lengths Increase Water Intensity

- Rig Counts Decline, Production Continues to Climb

- Mapping the Key U.S. Shale Basins and Plays

- Permian Basin Underpins Drill Rig Counts and Activity

- Permian Basin Surges in Unconventional Gas Production

- New Well Completions Decline Slightly With Drilling Efficiencies

- Increase in U.S. LNG Exports Drives Water Demand

Section 2 - Midstream Water Market Drivers, Trends, and Challenges

- Midstream Water Drivers and Impacts

- Hydraulic Fracturing Water Use per Well

- Total Water Use for Well Completions Grew Steadily

- Total Well Water Supply Volumes Continue to Grow Across Top Basins

- Water Stress to Increase Most Acutely in Western and Southern U.S.

- Seismic Events from Disposal Push Policy for Expanded Water Reuse

- Federal Policy Remains Largely Unchanged

- State & Local Policy Overview

Section 3 - Midstream Water Market Size and Forecasts

- Market Forecast Methodology Overview

- The Midstream Water Value Chain

- Midstream Water Trends Across the Value Chain

- Forecasted Segments

- Oil & Gas Sector Spend on Water Management Services by Basin

- Increasing Water Usage per Well Continues Through 2030

- Water Demand Increasingly Supplied by Recycled Produced Water

- Produced Water Volumes Set to Increase Across U.S. Basins

- Basin Recycling Rates Projected to Grow Modestly, Offset Disposal

- CAPEX Growth Signals Infrastructure Expansion

- Segmenting Capital Expenditures for Midstream Water

- CAPEX Recycling Facility Growth by Type and Size

- Drivers of Innovation and Investment for Future Water Solutions & Services

- Top Opportunities by Basin and State (2025-2030)

Section 4 - Basin & Shale Play Profiles

- Anadarko

- Appalachia

- Bakken

- Eagle Ford

- Haynesville

- Niobrara-DJ (Denver-Julesburg)

- Permian

Section 5 - Competitive Landscape

- Midstream Water Competitive Set

- Midstream Water Competitive Positioning

- M&A Trends by Competitive Segment (2020-2025)

- Water Pure-Play M&A Activity by Ownership Type

- Market Share: Pipeline Infrastructure Expansion to Continue

- Water-Related Acquisitions (2020-2025)

- Antero Midstream Corporation

- Aqua Terra Water Management

- Bison Water Midstream

- Blackbuck Resources

- Bosque Systems

- CNX Water

- Dalbo Holdings Inc

- Deep Blue Midland Basin

- Delek Logistics Partners, LP

- Dresser Utility Solutions

- EQT Corporation

- Freestone Midstream

- Goodnight Midstream

- Hess Midstream

- NGL Water Solutions

- Layne Water Midstream

- Martin Water Midstream

- Pilot Water Solutions

- RRIG Water Solutions

- Select Water Solutions

- Stonehill Environmental Partners

- Tallgrass Water

- Texas Pacific Land Corporation

- WaterBridge

- Western Midstream

- XRI Water