PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1666573

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1666573

Dry Type Distribution Transformer Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

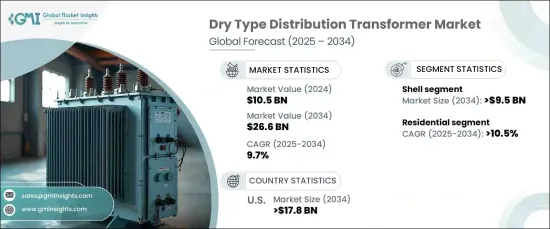

The Global Dry Type Distribution Transformer Market was valued at USD 10.5 billion in 2024, with expectations to grow at an impressive CAGR of 9.7% between 2025 and 2034. The market's expansion is primarily driven by technological innovations, increasing environmental regulations, and the evolving needs of modern power systems. Dry-type transformers are becoming the preferred choice due to their enhanced safety features, eco-friendly design, and operational efficiency. Unlike oil-filled transformers, dry-type transformers do not use flammable liquids, making them a safer and more sustainable option.

As urbanization accelerates and industrial growth increases, the demand for efficient, environmentally friendly electrical distribution solutions continues to rise. Technological advancements, such as integration with renewable energy sources and smart grids, are further boosting their adoption. Additionally, stricter global environmental regulations, which emphasize reducing carbon footprints, are making dry-type transformers an essential part of the power infrastructure landscape. With a strong focus on sustainability and energy efficiency, this market is poised for significant growth over the next decade.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $10.5 Billion |

| Forecast Value | $26.6 Billion |

| CAGR | 9.7% |

In particular, the shell-core segment is expected to dominate the market, projected to reach USD 9.5 billion by 2034. The superior performance and compact design of shell-core transformers make them ideal for sectors where space optimization and energy efficiency are critical. These transformers are increasingly utilized in industries such as renewable energy, smart grids, and urban infrastructure. Their efficiency and safety features align perfectly with the growing demand for sustainable and modern power distribution systems. As the global shift toward smart grids and renewable energy solutions continues, the adoption of shell-core transformers is expected to rise substantially.

The residential sector is also experiencing robust growth, with a projected CAGR of 10.5% through 2034. The increasing deployment of dry-type transformers in urban and residential applications is driven by the need for safer, space-efficient solutions. As urban areas become more densely populated, these transformers provide an ideal solution for power distribution in smaller spaces. Moreover, the integration of renewable energy sources like solar power and smart grids is driving their adoption in residential areas. With more consumers opting for energy-efficient homes, dry-type transformers are essential for maintaining reliable power distribution while meeting sustainability goals.

In the U.S., the dry-type distribution transformer market is forecasted to generate USD 17.8 billion by 2034. The growing focus on renewable energy, coupled with strict energy efficiency regulations, is significantly driving the adoption of dry-type transformers. They are increasingly used in applications such as urban infrastructure, electric vehicle charging stations, and smart grid systems. As the demand for cleaner and more reliable power solutions rises, dry-type transformers are becoming an indispensable part of the energy landscape. With continued urbanization and industrial development, these transformers are playing a crucial role in ensuring sustainable and efficient power distribution across the U.S.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 – 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Strategic dashboard

- 4.2 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Core, 2021 – 2034 (‘000 Units, USD Million)

- 5.1 Key trends

- 5.2 Closed

- 5.3 Shell

- 5.4 Berry

Chapter 6 Market Size and Forecast, By Product, 2021 – 2034 (‘000 Units, USD Million)

- 6.1 Key trends

- 6.2 Open wound

- 6.3 Cast resin

- 6.4 Vacuum pressure impregnated

- 6.5 Vacuum pressure encapsulated

Chapter 7 Market Size and Forecast, By Winding, 2021 – 2034 (‘000 Units, USD Million)

- 7.1 Key trends

- 7.2 Two winding

- 7.3 Auto transformer

Chapter 8 Market Size and Forecast, By Rating, 2021 – 2034 (‘000 Units, USD Million)

- 8.1 Key trends

- 8.2 ≤ 250 kVA

- 8.3 >250 kVA to ≤ 1 MVA

- 8.4 > 1 MVA

Chapter 9 Market Size and Forecast, By Application, 2021 – 2034 (‘000 Units, USD Million)

- 9.1 Key trends

- 9.2 Residential

- 9.3 Commercial & industrial

- 9.4 Utility

Chapter 10 Market Size and Forecast, By Region, 2021 – 2034 (‘000 Units, USD million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.2.3 Mexico

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 France

- 10.3.3 Germany

- 10.3.4 Italy

- 10.3.5 Russia

- 10.3.6 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Australia

- 10.4.3 India

- 10.4.4 Japan

- 10.4.5 South Korea

- 10.5 Middle East & Africa

- 10.5.1 Saudi Arabia

- 10.5.2 UAE

- 10.5.3 Turkey

- 10.5.4 South Africa

- 10.5.5 Egypt

- 10.6 Latin America

- 10.6.1 Brazil

- 10.6.2 Argentina

Chapter 11 Company Profiles

- 11.1 ABB

- 11.2 Bharat Heavy Electricals

- 11.3 CG Power and Industrial Solutions

- 11.4 Eaton

- 11.5 Fuji Electric

- 11.6 GE

- 11.7 Hitachi Energy

- 11.8 Instrument Transformer Equipment

- 11.9 Raychem RPG

- 11.10 Schneider Electric

- 11.11 SGB SMIT

- 11.12 Siemens Energy

- 11.13 TMC Transformers

- 11.14 Toshiba Energy Systems and Solutions

- 11.15 URJA Techniques

- 11.16 WEG