PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1685079

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1685079

Bottled Water Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

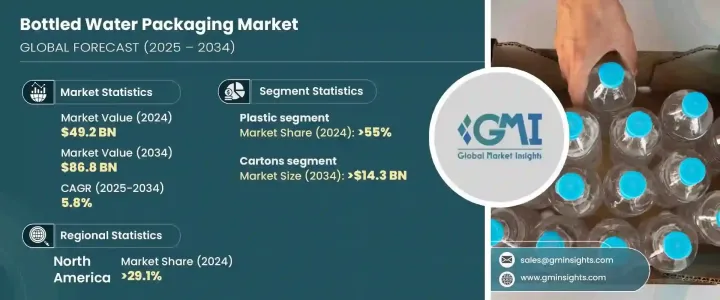

The Global Bottled Water Packaging Market reached USD 49.2 billion in 2024 and is expected to exhibit a CAGR of 5.8% from 2025 to 2034. This impressive growth is primarily driven by the increasing consumer demand for convenient, portable, and sustainable packaging solutions in the beverage industry. As the world's consumption of bottled water continues to expand, there's a significant shift in consumer preferences toward products that offer both convenience and environmental responsibility.

Manufacturers are keenly aware of these evolving demands and are responding by innovating their packaging solutions to meet both functional and sustainability requirements. These innovations are not just limited to packaging design but also encompass material choices and production processes that reduce the environmental footprint. Sustainability has become a central focus for both producers and consumers alike as the industry adapts to shifting regulations and eco-conscious buyer behavior. As consumer awareness about environmental issues continues to rise, packaging plays a critical role in influencing purchasing decisions, making it a key area of focus for businesses looking to stay ahead in the market.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $49.2 Billion |

| Forecast Value | $86.8 Billion |

| CAGR | 5.8% |

By packaging material, the bottled water packaging market is segmented into plastic, glass, metal, and other materials, with plastic dominating the market, holding a 55% share in 2024. The plastic segment is undergoing a notable transformation, with a growing trend toward lightweight and thinner bottle designs. These innovations aim to reduce material usage without compromising on durability or convenience. Furthermore, the emphasis on sustainability has led many companies to incorporate higher percentages of recycled PET (rPET) in their products, effectively minimizing environmental impact while still providing a high-quality, convenient solution for consumers.

In terms of packaging type, the market includes bottles, cans, cartons, pouches, and others. The cartons segment is projected to grow at a robust CAGR of 6.5% and generate USD 14.3 billion by 2034. Cartons have garnered increasing popularity due to their renewable, recyclable, and sustainable nature. Often made from paperboard with a thin plastic lining, cartons provide a more eco-friendly alternative to traditional plastic bottles, addressing concerns over plastic waste. Consumers are leaning more towards these solutions for their reduced carbon footprint and the environmentally responsible processes involved in their production.

North America holds a substantial share of the bottled water packaging market, with a 29.1% share in 2024. The region's demand is largely driven by a preference for convenient, innovative packaging options. In response, manufacturers are introducing cutting-edge solutions, including biodegradable materials and lightweight bottles made from recycled plastics. With growing consumer awareness about sustainability, the demand for packaging that aligns with eco-conscious values is expected to continue driving the market expansion. Moreover, the rising interest in premium and functional water products is pushing the boundaries of packaging design as brands seek to appeal to health-conscious and eco-aware consumers.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Disruptions

- 3.1.3 Future outlook

- 3.1.4 Manufacturers

- 3.1.5 Distributors

- 3.2 Profit margin analysis

- 3.3 Key news & initiatives

- 3.4 Regulatory landscape

- 3.5 Impact forces

- 3.5.1 Growth drivers

- 3.5.1.1 Growth in private label bottled water brands

- 3.5.1.2 Expansion of premium functional hydration in aluminum cans

- 3.5.1.3 Increasing health consciousness among consumers

- 3.5.1.4 Rising demand for convenience and on-the-go packaging

- 3.5.1.5 Rising awareness about clean drinking water

- 3.5.2 Industry pitfalls & challenges

- 3.5.2.1 Global variation in waste management practices and policies

- 3.5.2.2 Environmental impact of plastic waste

- 3.5.1 Growth drivers

- 3.6 Growth potential analysis

- 3.7 Porter’s analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Packaging Material, 2021-2034 (USD Billion & Kilo Tons)

- 5.1 Key trends

- 5.2 Plastic

- 5.3 Glass

- 5.4 Metal

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Packaging Type, 2021-2034 (USD Billion & Kilo Tons)

- 6.1 Key trends

- 6.2 Bottles

- 6.3 Cans

- 6.4 Cartons

- 6.5 Pouches

- 6.6 Others

Chapter 7 Market Estimates & Forecast, By Capacity, 2021-2034 (USD Billion & Kilo Tons)

- 7.1 Key trends

- 7.2 Below 500 ml

- 7.3 500 ml to 1 liter

- 7.4 1 liter to 2.5 liters

- 7.5 Above 2.5 liters

Chapter 8 Market Estimates & Forecast, By Application, 2021-2034 (USD Billion & Kilo Tons)

- 8.1 Key trends

- 8.2 Still water

- 8.3 Carbonated water

- 8.4 Flavored water

- 8.5 Functional water

- 8.6 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion & Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Alpla

- 10.2 Amcor

- 10.3 Aquafina

- 10.4 Ball

- 10.5 Crystal Geyser

- 10.6 Gerolsteiner

- 10.7 Graham Packaging

- 10.8 Greif

- 10.9 Ice Mountain

- 10.10 Kinley

- 10.11 Nestle Waters

- 10.12 O-I Glass

- 10.13 Sabic

- 10.14 Sidel

- 10.15 Tetra Pak

- 10.16 Vetropack

- 10.17 Vidrala

- 10.18 Westrock