PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1721470

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1721470

Automotive Plastic Ignition Holders Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

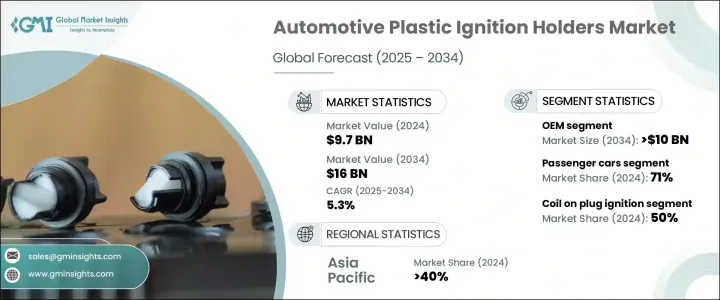

The Global Automotive Plastic Ignition Holders Market was valued at USD 9.7 billion in 2024 and is estimated to grow at a CAGR of 5.3% to reach USD 16 billion by 2034. This growth trajectory is attributed to a robust surge in global automobile production and vehicle ownership, especially in emerging economies where automotive infrastructure is rapidly advancing. Consumers are leaning toward vehicles that are not only fuel-efficient and cost-effective but also equipped with components that support longer engine life and lower emissions. As a result, automakers are increasingly adopting high-performance plastic components that reduce overall vehicle weight and meet evolving regulatory standards for emissions and fuel economy.

Automotive plastic ignition holders have become a vital component in modern vehicle designs due to their excellent heat resistance, cost-efficiency, and durability. These holders are helping original equipment manufacturers (OEMs) achieve critical goals, including reduced engine weight, better thermal management, and overall enhanced vehicle efficiency. The market is also witnessing strong investment in material innovation, with major industry players accelerating R&D activities to improve the structural integrity and performance of these components. Growth is further supported by increasing demand for compact vehicles, adoption of advanced combustion technologies, and a steady rise in global consumer preference for environmentally responsible mobility solutions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $9.7 Billion |

| Forecast Value | $16 Billion |

| CAGR | 5.3% |

Advanced composite materials and high-performance thermoplastics are key enablers of innovation in this space. Materials such as polyamide (PA), polyphenylene sulfide (PPS), and reinforced thermoplastics are being widely used to manufacture ignition holders that can withstand high temperatures and mechanical stress. These materials help reduce component weight, enhance fuel efficiency, and minimize emissions-making them ideal for use in both entry-level and premium vehicle segments. Their cost-effectiveness and reliability have made plastic ignition holders a preferred choice across global automotive platforms.

In terms of engine types, the market is segmented into gasoline, diesel, and alternative fuel categories. The gasoline engine segment led the market in 2024, capturing over 60% of the total share and is projected to reach USD 9 billion by 2034. The growing preference for low-emission and fuel-efficient gasoline vehicles is fueling the demand for lightweight ignition components. Plastic ignition holders play a critical role in ensuring precise ignition timing, which is essential for optimal combustion and engine performance-especially in modern direct-injection gasoline engines.

Passenger cars represented the dominant vehicle type, accounting for 71% of the market share in 2024. Rising production of compact and fuel-efficient cars continues to propel demand for lightweight, affordable ignition holders. The increasing integration of turbocharged engines in passenger cars has intensified the need for thermally stable, durable ignition components to support high-performance output.

The U.S. automotive plastic ignition holders market is forecast to experience notable growth from 2025 to 2034, spurred by strict fuel efficiency standards and rising adoption of advanced ignition systems. Automakers in the region are prioritizing lightweight designs and innovative materials to meet environmental regulations and enhance fuel economy, thereby accelerating the uptake of plastic ignition holders in both OEM and aftermarket applications.

Leading market players include Bosch, Mitsubishi Electric, Valeo, BorgWarner, Hitachi, NGK Spark Plug, Standard Motor Products, Diamond Electric, Denso, and HELLA. These companies are advancing their market strategies by expanding R&D capabilities, introducing innovative ignition solutions, and forming collaborations with automakers to create vehicle-specific designs. The deployment of modern manufacturing techniques and enhanced materials is also helping these firms improve product performance, while partnerships with regulatory agencies ensure compliance with evolving safety and environmental standards.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Raw material suppliers

- 3.2.2 Manufacturers

- 3.2.3 Service providers

- 3.2.4 Distributors

- 3.2.5 End users

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Price trends

- 3.9 Cost breakdown analysis

- 3.10 Impact forces

- 3.10.1 Growth drivers

- 3.10.1.1 Increasing demand for lightweight automotive components to enhance fuel efficiency

- 3.10.1.2 Advancements in high-performance thermoplastics improving durability and heat resistance

- 3.10.1.3 Growing automotive production in emerging markets driving mass adoption

- 3.10.1.4 Rising aftermarket demand for cost-effective replacement ignition system components

- 3.10.2 Industry pitfalls & challenges

- 3.10.2.1 Durability concerns compared to metal ignition holders in extreme conditions

- 3.10.2.2 Limited adoption in high-performance and heavy-duty vehicles requiring higher strength materials

- 3.10.1 Growth drivers

- 3.11 Growth potential analysis

- 3.12 Porter’s analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Material, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Polyamide (PA)

- 5.3 Polypropylene (PP)

- 5.4 Polybutylene Terephthalate (PBT)

- 5.5 Polyphenylene Sulfide (PPS)

- 5.6 Polyethylene Terephthalate (PET)

- 5.7 Others

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.2.1 SUV

- 6.2.2 Sedan

- 6.2.3 Hatchback

- 6.3 Commercial vehicles

- 6.3.1 Light Commercial Vehicles (LCV)

- 6.3.2 Medium Commercial Vehicle (MCV)

- 6.3.3 Heavy Commercial Vehicles (HCV)

- 6.4 Off-highway vehicles

Chapter 7 Market Estimates & Forecast, By Engine, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Gasoline

- 7.3 Diesel

- 7.4 Alternative fuels

Chapter 8 Market Estimates & Forecast, By Ignition, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Coil on plug ignition

- 8.3 Simultaneous ignition

- 8.4 Compression ignition

Chapter 9 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 Ignition switch

- 9.3 Spark plug

- 9.4 Glow plug

- 9.5 Ignition coil

- 9.6 Others

Chapter 10 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 OEM

- 10.3 Aftermarket

Chapter 11 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Russia

- 11.3.7 Nordics

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 ANZ

- 11.4.6 Southeast Asia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 UAE

- 11.6.2 South Africa

- 11.6.3 Saudi Arabia

Chapter 12 Company Profiles

- 12.1 BorgWarner

- 12.2 Bosch

- 12.3 Continental

- 12.4 Denso

- 12.5 Diamond Electric

- 12.6 DuPont

- 12.7 HELLA

- 12.8 Hitachi

- 12.9 Magna

- 12.10 Mitsubishi Electric

- 12.11 NGK Spark Plug

- 12.12 Polyplastics

- 12.13 Samvardhana

- 12.14 Sensata

- 12.15 Standard Motor Products

- 12.16 Sumitomo

- 12.17 Toyoda Gosei

- 12.18 Valeo

- 12.19 Visteon

- 12.20 Yazaki