PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1721603

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1721603

Eyewear Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

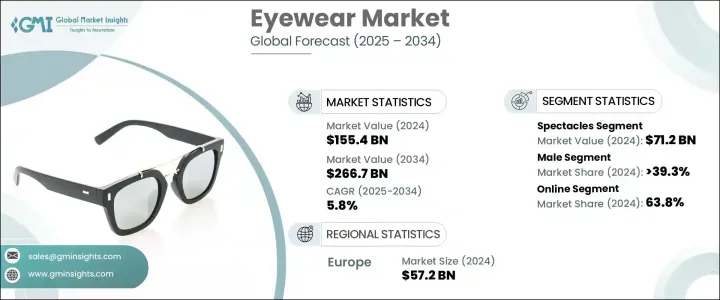

The Global Eyewear Market was valued at USD 155.4 billion in 2024 and is estimated to grow at a CAGR of 5.8% to reach USD 266.7 billion by 2034. One of the key factors fueling this growth is the rising appeal of eyewear as a status-enhancing accessory. Consumers today no longer view eyeglasses and sunglasses as mere vision aids but rather as premium lifestyle products. The shift toward high-end eyewear is creating strong momentum as people look for designs that match their personal style, offer durability, and reflect a certain social identity. This trend is particularly strong among buyers who prefer exclusive, well-crafted pieces made from advanced materials and featuring enhanced lens technologies. These preferences are driving demand for products that blend function and fashion. On top of that, celebrity influence and brand partnerships are amplifying the appeal of luxury eyewear, helping create a sense of exclusivity that resonates with consumers across demographics. Limited-edition releases and designer collaborations further enhance this market by generating excitement and urgency to purchase. As a result, the market is experiencing a transformation where value is defined not only by vision correction but also by personal image, comfort, and brand experience.

The product segment includes spectacles, contact lenses, and sunglasses. In 2024, the spectacles category led the market with revenue of USD 71.2 billion and is estimated to register a CAGR of 5.3% during the forecast period. One major contributor to this growth is the widespread incidence of digital eye strain, commonly known as computer vision syndrome (CVS). As screen time increases across all age groups, especially with prolonged exposure to smartphones, computers, and tablets, more individuals are turning to glasses designed to reduce glare and fatigue. The pandemic accelerated this trend as remote learning and online activities spiked, especially among younger users. The growing popularity of protective eyewear equipped with anti-glare and anti-fatigue coatings has led to increased adoption of such products. Additionally, there is a visible trend toward clear and tinted lens glasses that serve both protective and fashion purposes, further boosting market demand.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $155.4 Billion |

| Forecast Value | $266.7 Billion |

| CAGR | 5.8% |

From the end-user perspective, the eyewear market is divided into male, female, unisex, and kids segments. In 2024, the male demographic dominated the landscape, holding more than 39.3% of the total market share. This group is expected to grow at a CAGR of 5.4% through 2034. Several factors are contributing to the strong demand from male consumers, including a higher prevalence of vision issues like myopia and presbyopia, as well as greater interest in premium-grade products. Men are increasingly leaning toward eyewear that offers both advanced functionality and refined style. Their preference for durable, long-lasting items over trend-based purchases is shaping the product portfolios of many brands. Additionally, growing interest in technologically enhanced products, including smart eyewear, is opening new opportunities. Whether for professional settings or personal use, eyewear that combines performance, protection, and polished aesthetics is resonating with this segment.

The market is also segmented by distribution channel into online and offline platforms. In 2024, online sales are projected to account for 63.8% of the global market share. The convenience of e-commerce, paired with increasing smartphone penetration and better digital interfaces, has redefined how consumers shop for eyewear. A seamless online shopping experience - from browsing to virtual try-ons - has empowered consumers to make informed choices from the comfort of their homes. The availability of detailed product reviews, recommendations, and customization options adds to the appeal. Moreover, digital platforms help brands tailor offerings for various buyer groups, making the experience more inclusive and efficient. Collaborations between eyewear brands and major online retailers have also enhanced market penetration and visibility. The speed and reach of online distribution have turned it into the primary choice for consumers, and this trend is expected to gain further traction over the coming years.

Geographically, Europe led the global eyewear market in 2024, contributing approximately USD 57.2 billion in revenue and accounting for around 36.8% of the overall market. The region's dominance is attributed to several factors, including its deep-rooted heritage in luxury fashion, a robust presence of renowned optical manufacturers, and a growing need for vision correction in an aging population. Europe's leadership in premium eyewear is reinforced by its advanced lens technologies and skilled craftsmanship. The region continues to set global design standards, making it a stronghold for both innovation and high-end appeal.

Leading players in the eyewear industry include Hoya Corporation, Carl Zeiss AG, Rodenstock GmbH, Luxottica Group SpA, Safilo Group, Marchon Eyewear Inc., De Rigo Vision S.p.A, Johnson & Johnson Vision Care Inc., and The Cooper Companies. These companies are at the forefront of lens innovation, premium frame design, and personalized solutions. Their efforts to combine aesthetics, quality, and optical performance continue to shape the competitive landscape and elevate consumer expectations worldwide.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.3 Pricing analysis

- 3.4 Technology & innovation landscape

- 3.5 Key news & initiatives

- 3.6 Regulatory landscape

- 3.7 Manufacturers

- 3.8 Distributors

- 3.9 Retailers

- 3.10 Impact on forces

- 3.10.1 Growth drivers

- 3.10.1.1 Rising preference for luxury brands eyewear

- 3.10.1.2 Increasing popularity of contact lens

- 3.10.1.3 Increasing awareness of eye safety

- 3.10.2 Industry pitfalls & challenges

- 3.10.2.1 Growing popularity of eye corrective surgeries

- 3.10.2.2 Price differentiation between branded and unbranded

- 3.10.1 Growth drivers

- 3.11 Growth potential analysis

- 3.12 Consumer behavior analysis

- 3.12.1 Demographic trends

- 3.12.2 Factors affecting buying decisions

- 3.12.3 Product Preference

- 3.12.4 Preferred price range

- 3.12.5 Preferred distribution channel

- 3.13 Porter’s analysis

- 3.14 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product, 2021 - 2034 ($Bn) (Thousand Units)

- 5.1 Key trends

- 5.2 Spectacles

- 5.2.1 Single vision

- 5.2.2 Multifocal

- 5.2.3 Bifocal

- 5.2.4 Progressive

- 5.2.5 Reading glasses

- 5.2.6 Safety glasses

- 5.2.7 Others (blue light glasses, etc.)

- 5.3 Contact lens

- 5.3.1 Soft contact lens

- 5.3.2 Rigid contact lens

- 5.3.3 Others (toric contact lens)

- 5.4 Sunglasses

- 5.4.1 Polarized

- 5.4.2 Non-polarized

Chapter 6 Market Estimates & Forecast, By Type, 2021 - 2034 ($Bn) (Thousand Units)

- 6.1 Key trends

- 6.2 Prescription

- 6.3 Non-prescription

Chapter 7 Market Estimates & Forecast, By Frame Material, 2021 - 2034 ($Bn) (Thousand Units)

- 7.1 Key trends

- 7.2 Metal

- 7.3 Plastic

- 7.4 Polycarbonate

- 7.5 Rubbers

- 7.6 Others (wooden, nylon, etc.)

Chapter 8 Market Estimates & Forecast, By Shape, 2021 - 2034 ($Bn) (Thousand Units)

- 8.1 Key trends

- 8.2 Oval & aviator

- 8.3 Rectangular

- 8.4 Round

- 8.5 Square

- 8.6 Others (oversized, shield, etc.)

Chapter 9 Market Estimates & Forecast, By Price, 2021 - 2034 ($Bn) (Thousand Units)

- 9.1 Key trends

- 9.2 Low

- 9.3 Medium

- 9.4 High

Chapter 10 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn) (Thousand Units)

- 10.1 Key trends

- 10.2 Male

- 10.3 Female

- 10.4 Unisex

- 10.5 Kids

Chapter 11 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034 ($Bn) (Thousand Units)

- 11.1 Key trends

- 11.2 Online

- 11.2.1 E-commerce

- 11.2.2 Company site

- 11.3 Offline

- 11.3.1 Specialty stores

- 11.3.2 Mega retail stores

- 11.3.3 Others (optical camps, ophthalmic centers, etc.)

Chapter 12 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn) (Thousand Units)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 U.S.

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 UK

- 12.3.2 Germany

- 12.3.3 France

- 12.3.4 Italy

- 12.3.5 Spain

- 12.3.6 Russia

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 India

- 12.4.3 Japan

- 12.4.4 Australia

- 12.4.5 South Korea

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.5.3 Argentina

- 12.6 MAMEA

- 12.6.1 UAE

- 12.6.2 South Africa

- 12.6.3 Saudi Arabia

Chapter 13 Company Profiles

- 13.1 Carl Zeiss AG

- 13.2 Luxottica Group SpA

- 13.3 Safilo

- 13.4 Hoya Corporation

- 13.5 The Cooper Companies

- 13.6 Johnson & Johnson Vision Care, Inc.

- 13.7 Bausch & Lomb Inc.

- 13.8 Charmant Group

- 13.9 CIBA VISION

- 13.10 De Rigo Vision S.p.A

- 13.11 Fielmann AG

- 13.12 JINS, Inc.

- 13.13 Marchon Eyewear, Inc.

- 13.14 QSpex Technologies

- 13.15 Rodenstock GmbH