PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1721610

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1721610

North America Residential Unitary HVAC Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

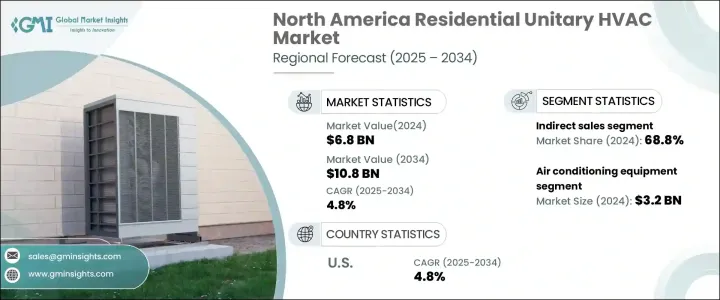

North America Residential Unitary HVAC Market was valued at USD 6.8 billion in 2024 and is estimated to grow at a CAGR of 4.8% to reach USD 10.8 billion by 2034. The market continues to expand due to a growing focus on comfort, energy efficiency, and advanced climate control technologies. Rising consumer awareness about the long-term benefits of energy-efficient systems is fueling product upgrades and replacements across the region. With homes being increasingly designed or retrofitted to support sustainable living, HVAC systems with high Seasonal Energy Efficiency Ratio (SEER) ratings are now in higher demand than ever. Additionally, homeowners are prioritizing cost-effective solutions that reduce energy bills while enhancing comfort levels year-round.

This push toward smart, connected HVAC solutions is driving technological innovation across the market. Regulatory mandates and government incentives for energy-efficient systems are further reinforcing consumer interest. Manufacturers are responding by launching products that align with Energy Star and other eco-certifications, creating an ecosystem where both environmental sustainability and energy cost savings go hand in hand. The ongoing urbanization, rise in home improvement projects, and changing climate conditions are also reshaping HVAC buying trends, making the residential sector a hotbed for innovation and growth.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $6.8 Billion |

| Forecast Value | $10.8 Billion |

| CAGR | 4.8% |

The air conditioning equipment segment alone generated USD 3.2 billion in 2024. Consumers are showing a growing preference for split air conditioning systems, which include both ducted and ductless models. Ductless mini-split systems, in particular, are becoming increasingly popular in urban areas and during home remodeling projects. Their easy installation process, high energy efficiency, and ability to provide zoned comfort make them an ideal fit for modern residential settings. These systems are well-suited for homes that lack traditional ductwork, allowing for personalized temperature control in individual rooms. As energy-conscious homeowners continue to prioritize both performance and convenience, the air conditioning segment maintains a stronghold in the broader residential HVAC landscape.

In terms of distribution, the North America residential unitary HVAC market is largely dominated by indirect sales, which accounted for 68.8% of the total in 2024. This model relies on an extensive network of distributors, wholesalers, and HVAC contractors who bring products closer to end users while streamlining delivery and service operations. Wholesale distributors play a key role in ensuring product availability and timely installations, helping bridge the gap between manufacturers and consumers with efficient logistical networks and well-established partnerships across the region.

The U.S. residential unitary HVAC market alone captured a significant 69.6% share in 2024. This dominance reflects the country's large population base, varied climate zones, and rising demand for reliable heating and cooling systems. Warmer regions, particularly in the southern states, consistently generate high demand for air conditioning units to counter intense summer heat.

Leading manufacturers are focusing on improving energy efficiency, expanding product portfolios, and integrating digital technologies such as smart thermostats and app-based system controls. Many are forming strategic alliances with wholesalers and contractors to improve supply chain agility and customer reach. Brands are also targeting emerging markets within North America, offering customized solutions and attractive pricing to boost adoption.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast parameters

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for energy efficient and sustainable cooling solutions

- 3.2.1.2 Advancements in HVAC Technology

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Energy shortages and crisis

- 3.2.2.2 Complex regulatory landscape

- 3.2.1 Growth drivers

- 3.3 Technology & innovation landscape

- 3.4 Growth potential analysis

- 3.5 Pricing analysis

- 3.6 Regulatory landscape

- 3.7 Porter’s analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product Type, 2021-2034 (USD Billion) (Thousand Units)

- 5.1 Air conditioning equipment

- 5.1.1 Split ac (ducted)

- 5.1.2 Window ac (ducted)

- 5.2 Ducted heat pumps/ packaged terminal heat pumps (PTHPS)

- 5.3 Variable refrigerant flow (VRF) systems

- 5.4 Packaged heating & cooling unit

- 5.5 Others (air handlers, gas furnaces, evaporator coils, etc.)

Chapter 6 Market Estimates & Forecast, By Installation, 2021-2034 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 New construction

- 6.3 Replacement/retrofit

Chapter 7 Market Estimates & Forecast, By Mounting Type, 2021 – 2034, (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Wall-mounted units

- 7.3 Ceiling-mounted units

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2021 – 2034, (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Direct sales

- 8.3 Indirect sales

Chapter 9 Market Estimates & Forecast, By Country, 2021 – 2034, (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 U.S.

- 9.3 Canada

Chapter 10 Company Profiles (Business Overview, Financial Data, Product Landscape, Strategic Outlook, SWOT Analysis)

- 10.1 Carrier Group

- 10.2 Daikin Industries Inc.

- 10.3 Danfoss A/S

- 10.4 GREE Electric Appliances, Inc.

- 10.5 Haier Group

- 10.6 Hisense HVAC equipment Co., Ltd.

- 10.7 Johnson Controls Plc

- 10.8 Lennox International

- 10.9 LG Electronics

- 10.10 Midea Group

- 10.11 Mitsubishi Electric Group

- 10.12 Panasonic Corporation

- 10.13 Rheem Manufacturing Company

- 10.14 Robert Bosch GmbH

- 10.15 Trane Technologies