PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1740756

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1740756

Automotive Active Roll Control System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

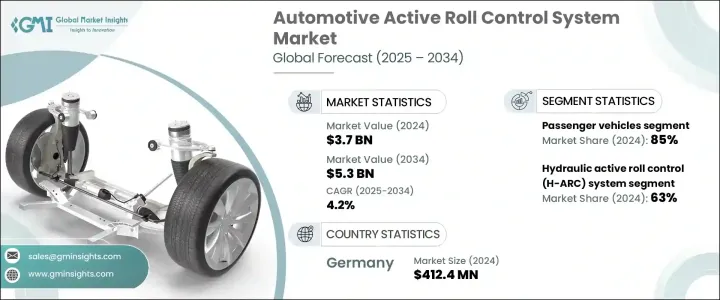

The Global Automotive Active Roll Control System Market was valued at USD 3.7 billion in 2024 and is estimated to grow at a CAGR of 4.2% to reach USD 5.3 billion by 2034, driven by the rising need for enhanced vehicle stability, safety, and ride comfort-especially in the growing SUV and luxury vehicle segments. As more consumers prioritize driving experience and on-road safety, the adoption of advanced suspension technologies like active roll control systems continues to accelerate. These systems play a vital role in reducing body roll when cornering or driving on uneven terrain, significantly improving handling precision and overall safety. With more automakers aiming to deliver a refined, performance-oriented ride without compromising comfort, active roll control systems are now seen as critical to modern vehicle design.

This market is witnessing increased momentum thanks to the surge in SUV and crossover vehicle sales, both of which have a higher center of gravity and require better dynamic control to ensure a smooth and safe ride. Consumers are also becoming more conscious of how vehicles perform in real-world driving conditions, especially with unpredictable road surfaces and high-speed cornering becoming more common in urban and suburban environments. Automakers are now integrating active roll control systems not only in premium vehicles but also in mid-range models to meet customer expectations and boost brand value. At the same time, the growing footprint of electric and hybrid vehicles-which often carry additional weight due to battery systems-calls for specialized suspension and stability systems, further fueling demand for active roll control technologies.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.7 Billion |

| Forecast Value | $5.3 Billion |

| CAGR | 4.2% |

Safety regulations across key regions like Europe and North America are playing a major role in pushing automakers to invest in cutting-edge technologies. As governments impose stricter compliance norms around vehicle safety and performance, manufacturers are under pressure to enhance the safety profiles of their vehicles. Active roll control systems help meet these regulatory demands while simultaneously offering a superior driving experience, making them a smart investment for OEMs looking to future-proof their product lines.

The automotive active roll control system market is segmented into two primary technologies: hydraulic active roll control (H-ARC) and electromechanical active roll control (eARC). As of 2024, hydraulic systems dominate the space, accounting for nearly 63% of the market share. Known for their high actuation force, reliability, and fast response times, H-ARC systems are widely used in SUVs and luxury vehicles where superior stability and performance are non-negotiable. These systems are particularly suited for heavier vehicles and continue to be the go-to solution for manufacturers prioritizing robust performance.

On the other hand, electromechanical active roll control systems are gradually gaining traction, especially as automakers explore more energy-efficient, compact, and electronically controlled solutions. While eARC still holds a smaller portion of the market, its integration into next-gen EVs and hybrids is expected to drive steady adoption over the next decade. The shift toward electrification and software-defined vehicles aligns well with the capabilities of eARC systems, which offer more precise control and integration with vehicle electronics.

Passenger cars represent the dominant vehicle category, capturing around 85% of the global market share in 2024. This segment's lead stems from the growing preference for cars that offer a premium driving experience coupled with top-tier safety features. As automakers ramp up the production of electric and hybrid cars, there is an increasing need for innovative suspension systems that can adapt to unique design and weight distribution challenges. Active roll control systems fit perfectly into this equation, offering enhanced control and comfort without sacrificing energy efficiency.

Germany stands out as a major player, holding a 29% share of the global automotive active roll control system market in 2024. With its robust automotive sector-home to some of the world's top luxury and performance car manufacturers-Germany continues to lead in the adoption of cutting-edge vehicle technologies. Strong R&D investment, a mature supplier base, and stringent regulatory frameworks have helped the country maintain a leadership position in deploying advanced stability systems across vehicle categories.

Key players in this market include ZF Friedrichshafen, ThyssenKrupp, Hyundai Mobis, Denso, Schaeffler, Robert Bosch, HELLA GmbH, Magna International, and Continental. These companies are doubling down on innovation by investing heavily in R&D to develop smarter, more cost-effective roll control solutions. Collaborations with global automakers are expanding their reach, especially in integrating these systems into EVs and hybrid models. A strong focus on regulatory alignment, technology advancement, and presence in emerging economies is allowing these companies to stay competitive while meeting rising demand for safety, comfort, and high-performance driving.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Component suppliers

- 3.2.2 Tier 1 suppliers

- 3.2.3 Automotive manufacturers (OEMs)

- 3.2.4 Software and technology providers

- 3.2.5 Research and development institutions

- 3.3 Profit margin analysis

- 3.4 Trump administration tariffs

- 3.4.1 Impact on trade

- 3.4.1.1 Trade volume disruptions

- 3.4.1.2 Retaliatory measures by other countries

- 3.4.2 Impact on the industry

- 3.4.2.1 Price Volatility in key materials

- 3.4.2.2 Supply chain restructuring

- 3.4.2.3 Production cost implications

- 3.4.3 Key companies impacted

- 3.4.4 Strategic industry responses

- 3.4.4.1 Supply chain reconfiguration

- 3.4.4.2 Pricing and product strategies

- 3.4.5 Outlook and future considerations

- 3.4.1 Impact on trade

- 3.5 Technology & innovation landscape

- 3.6 Price trends

- 3.7 Patent analysis

- 3.8 Key news & initiatives

- 3.9 Regulatory landscape

- 3.10 Impact forces

- 3.10.1 Growth drivers

- 3.10.1.1 Increasing demand for enhanced vehicle stability and handling

- 3.10.1.2 Increasing sales of SUVs and luxury vehicles

- 3.10.1.3 Stringent government regulations mandating safety features

- 3.10.1.4 Integration with advanced driver-assistance systems (ADAS) and autonomous driving technologies

- 3.10.1.5 Advancements in suspension technologies

- 3.10.2 Industry pitfalls & challenges

- 3.10.2.1 High initial cost

- 3.10.2.2 Complexity of integration and calibration

- 3.10.1 Growth drivers

- 3.11 Growth potential analysis

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Actuators

- 5.3 Electronic Control Units (ECUs)

- 5.4 Sensors

- 5.5 Linkages and mounts

Chapter 6 Market Estimates & Forecast, By Type, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Hydraulic active roll control (H-ARC) system

- 6.3 Electromechanical active roll control (eARC) system

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Passenger vehicles

- 7.2.1 Hatchback

- 7.2.2 Sedan

- 7.2.3 SUV

- 7.3 Commercial vehicles

- 7.3.1 Light Commercial Vehicles (LCV)

- 7.3.2 Medium Commercial Vehicles (MCV)

- 7.3.3 Heavy Commercial Vehicles (HCV)

Chapter 8 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 OEMs (Original Equipment Manufacturers)

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Benteler

- 10.2 BWI Group

- 10.3 Continental

- 10.4 Denso

- 10.5 Eibach

- 10.6 HELLA GmbH

- 10.7 Hitachi Astemo

- 10.8 Hyundai Mobis

- 10.9 Infineon Technologies

- 10.10 JTEKT Corporation

- 10.11 KYB Corporation

- 10.12 Magna International

- 10.13 Mando Corporation

- 10.14 Robert Bosch

- 10.15 Schaeffler

- 10.16 Tenneco

- 10.17 ThyssenKrupp

- 10.18 TRW Automotive

- 10.19 WABCO

- 10.20 ZF Friedrichshafen