PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1740930

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1740930

Water Desalination and Purification Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

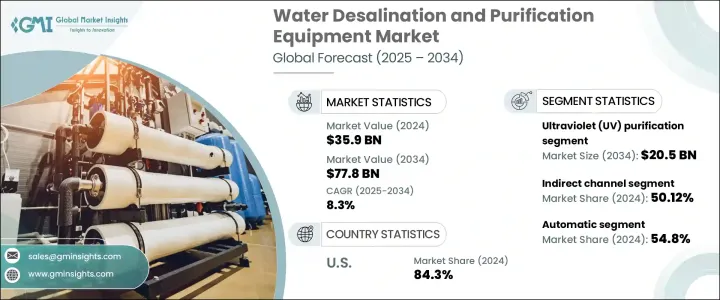

The Global Water Desalination and Purification Equipment Market was valued at USD 35.9 billion in 2024 and is estimated to grow at a CAGR of 8.3% to reach USD 77.8 billion by 2034. This growth is largely attributed to the rising pressure on freshwater supplies due to increasing population density and rapid urban expansion, especially in dry and semi-arid regions. As conventional water sources-such as rivers and underground aquifers-face depletion, pollution, and growing instability due to climate variability, alternative technologies for freshwater production are gaining traction. Among them, desalination stands out as a reliable option, particularly because it enables the transformation of saline and brackish water into clean drinking water. Technological improvements in processes like reverse osmosis and electrodialysis have significantly reduced operational costs and energy consumption, making them more attractive for large-scale deployment. With water being a critical resource across agriculture, industrial activities, and urban development, the demand for consistent and sustainable water solutions is driving the adoption of advanced desalination and purification systems across various sectors.

One of the fastest-growing segments in this market is ultraviolet (UV) purification. In 2024, the UV purification segment generated revenue of USD 8.8 billion and is anticipated to reach USD 20.5 billion by 2034. UV systems are gaining momentum across industries due to their ability to eliminate harmful microorganisms in water without producing toxic chemical by-products. As environmental sustainability becomes more central to global policy and industrial operations, UV purification is becoming a preferred choice thanks to its low energy requirements, minimal maintenance needs, and long-term cost-effectiveness. These systems are also adaptable and easy to integrate into both newly developed and pre-existing water treatment frameworks, increasing their appeal for use in both urban and rural applications. Advancements in UV lamp technology are enhancing system durability and performance, prompting greater adoption worldwide. As access to safe drinking water remains a pressing global concern, UV purification is being recognized as a critical component in securing water for both public and private use.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $35.9 Billion |

| Forecast Value | $77.8 Billion |

| CAGR | 8.3% |

Distribution channels play a significant role in how this equipment reaches end users. In 2024, the indirect distribution channel dominated the market, accounting for 50.12% of the overall share, and is projected to reach a valuation of USD 37.6 billion by 2034. This route has proven advantageous for manufacturers seeking to expand their geographical footprint without establishing a physical presence in every market. Through partnerships with resellers, agents, and third-party distributors, companies can leverage local market knowledge, regulatory familiarity, and pre-existing customer networks. This approach significantly reduces the time needed to introduce products to new markets while optimizing logistical and operational efficiency. Indirect distribution has therefore become a strategic tool in enhancing both reach and responsiveness across diverse regions.

When it comes to the mode of operation, automatic systems are leading the market. In 2024, automatic systems are expected to hold 54.8% of the total market share. These systems allow for real-time monitoring and automated control of critical operational parameters such as chemical dosing, pressure levels, and flow rates. Although the upfront cost of automatic systems is typically higher than their manual counterparts, the long-term benefits-including lower labor dependence, reduced maintenance, and enhanced energy efficiency-make them more viable for larger or remote facilities. Furthermore, integration with IoT and remote monitoring technologies enhances operational reliability and allows centralized management of distributed infrastructure, which is crucial for large-scale desalination plants.

Regionally, the United States held a commanding 84.30% share of the North American market in 2024 and is expected to continue expanding at a CAGR of 8.9% during the forecast years. The country's dominance is driven by high demand for advanced water treatment solutions, particularly in regions affected by drought and water scarcity. Leading domestic and international companies are actively involved in delivering innovative systems that support sustainable water use. These companies are heavily invested in R&D, offering comprehensive services from design to maintenance, and have established themselves as reliable partners for large-scale industrial and municipal projects.

The top five market players-Veolia North America, Aquatech International, SUEZ Water Technologies & Solutions, Xylem Inc., and IDE Technologies-collectively control about 40% to 50% of global revenue. These firms offer full-service solutions and cutting-edge technologies like reverse osmosis, UV systems, and membrane filtration to a global customer base. Their strong emphasis on energy efficiency, eco-friendly practices, and strategic collaborations with public and private sector entities further reinforce their leadership in the evolving landscape of water desalination and purification.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factors affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-Side Impact (Raw Materials)

- 3.2.2.2 Price volatility in key materials

- 3.2.2.3 Supply chain restructuring

- 3.2.2.4 Production cost implications

- 3.2.2.5 Demand-Side Impact (Selling Price)

- 3.2.2.6 Price transmission to end markets

- 3.2.2.7 Market share dynamics

- 3.2.2.8 Consumer response patterns

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and Future considerations

- 3.2.1 Impact on trade

- 3.3 Impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Water scarcity and increasing demand for freshwater

- 3.3.1.2 Government initiatives and regulations

- 3.3.1.3 Technological advancements

- 3.3.2 Industry pitfalls & challenges

- 3.3.2.1 High capital and operating costs

- 3.3.2.2 Lack of infrastructure and investment in developing regions

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Technology, 2021-2034 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Nanofiltration

- 5.3 Reverse osmosis (RO)

- 5.4 Multi-stage flash (MSF) distillation

- 5.5 Multi-effect distillation (MED)

- 5.6 Ultraviolet (UV) purification

- 5.7 Activated carbon filtration

- 5.8 Others (ultrafiltration, ion exchange, etc.)

Chapter 6 Market Estimates & Forecast, By Mode of Operation, 2021-2034 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Automatic systems

- 6.3 Manual systems

Chapter 7 Market Estimates & Forecast, By System Scale, 2021-2034 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Small-scale system

- 7.3 Medium-scale system

- 7.4 Large-scale systems

Chapter 8 Market Estimates & Forecast, By Application, 2021-2034 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Desalination

- 8.3 Water purification

- 8.4 Industrial water treatment

- 8.5 Household water treatment

- 8.6 Agricultural water treatment

- 8.7 Healthcare water treatment

- 8.8 Others

Chapter 9 Market Estimates & Forecast, By End Use 2021-2034 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Municipal

- 9.3 Industrial

- 9.4 Residential

- 9.5 Commercial

- 9.6 Others (healthcare, agriculture)

Chapter 10 Market Estimates & Forecast, By Distribution Channel 2021-2034 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 Direct

- 10.3 Indirect

Chapter 11 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn) (Thousand Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.6 MEA

- 11.6.1 UAE

- 11.6.2 South Africa

- 11.6.3 Saudi Arabia

Chapter 12 Company Profiles

- 12.1 Aquatech International

- 12.2 Doosan Heavy Industries and Construction

- 12.3 Dupont

- 12.4 GE Water and Process Technologies

- 12.5 Hyflux

- 12.6 IDE Technologies

- 12.7 Lenntech

- 12.8 Membranium

- 12.9 Pentair

- 12.10 Saudi Arabian Amiantit

- 12.11 Suez Water Technologies and Solutions

- 12.12 Tata Projects

- 12.13 Toray Industries

- 12.14 Veolia North America

- 12.15 Xylem