PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1741034

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1741034

Medical Electronics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

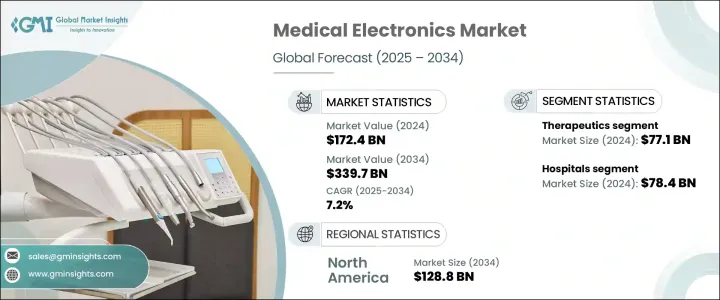

The Global Medical Electronics Market was valued at USD 172.4 billion in 2024 and is estimated to grow at a CAGR of 7.2% to reach USD 339.7 billion through 2034. This growth is driven by the expanding use of electronic systems and devices across healthcare sectors to support diagnosis, treatment, prevention, and patient monitoring. As the healthcare landscape becomes increasingly digitized, medical electronics are transforming how clinicians deliver care. From diagnostic imaging tools and wearable monitors to robotic surgery systems and connected therapeutics, these devices are reshaping patient experiences and clinical outcomes. The integration of smart technologies like AI, IoT, and cloud computing is redefining operational efficiency, enabling faster diagnostics, improving data accuracy, and reducing human error. Hospitals, clinics, and even home care environments now rely on interconnected medical electronics to streamline workflows, manage chronic diseases, and enhance patient engagement. With an aging global population and the rising incidence of non-communicable diseases, there's a clear shift toward tech-driven healthcare solutions. Consumers are demanding personalized, accessible, and real-time healthcare services, pushing companies to innovate faster and introduce more intuitive, reliable medical electronic devices.

The continuous rise in chronic and infectious diseases-including cardiovascular conditions, cancer, and respiratory disorders-is contributing heavily to the surging demand for advanced medical electronics. There's growing public awareness around early disease detection and preventive care, which is encouraging the widespread use of diagnostic technologies. At the same time, advancements in minimally invasive surgical techniques are accelerating the need for high-precision electronic tools. These innovations are helping improve real-time procedural accuracy, reduce recovery times, and enhance clinical outcomes for patients globally.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $172.4 Billion |

| Forecast Value | $339.7 Billion |

| CAGR | 7.2% |

The market is also seeing robust momentum from ongoing technological innovation in areas like medical robotics, remote monitoring, and wearable diagnostics. As consumers lean toward smarter, more connected healthcare tools, the integration of electronics in medical applications continues to gain traction. Rising global healthcare expenditures further support the adoption of sophisticated electronic devices, especially those designed to manage complex procedures and long-term care. This trend is particularly evident in specialized medical fields where demand for real-time data, enhanced imaging, and precision control remains critical.

In 2024, the therapeutics segment generated USD 77.1 billion, driven by the increasing use of implantable and external devices to manage chronic conditions. These therapeutic technologies combine advanced electronic features to improve safety, delivery accuracy, and personalized care-especially in cardiovascular, neurological, and respiratory treatment. Devices such as pacemakers, neurostimulators, and infusion pumps are being widely adopted to boost quality of life and reduce hospital visits.

Hospitals led end-user adoption in 2024, generating USD 78.4 billion and accounting for 45.5% of the market share. These institutions depend heavily on both diagnostic and therapeutic electronics to manage outpatient and inpatient care efficiently. With a focus on optimizing clinical workflows and minimizing treatment delays, hospitals continue to invest in next-generation monitoring equipment, surgical technologies, and imaging systems to drive better outcomes.

The U.S. Medical Electronics Market generated USD 57.4 billion in 2023, fueled by the growing burden of chronic diseases such as cardiovascular disorders, diabetes, cancer, and neurological conditions. With more patients requiring continuous monitoring and treatment, the demand for advanced electronic medical devices remains high. The U.S. also benefits from strong R&D infrastructure and early tech adoption, helping sustain its leadership in medical innovation.

Leading players in the Global Medical Electronics Market-including Olympus, Shenzhen Mindray Bio-Medical Electronics, Siemens Healthineers, Lepu Medical Technology, Boston Scientific, Toshiba Medical Systems, FUJIFILM Holdings, GE HealthCare, Abbott Laboratories, MicroPort Scientific, Samsung Electronics, Medtronic, Carestream Health, Koninklijke Philips, and Esaote-are implementing key strategies to strengthen their market presence. These include boosting R&D investments to fast-track innovation, collaborating with healthcare providers for real-time feedback, expanding into emerging markets, and leveraging AI and IoT to launch intelligent diagnostic and remote care platforms.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising burden of chronic and infectious diseases

- 3.2.1.2 Growing adoption of technologically advanced medical electronics

- 3.2.1.3 Increasing preference towards minimally invasive surgeries

- 3.2.1.4 Upsurge in leasing of capital-intensive machines and development of significant policies for foreign direct investment (FDI)

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Stringent regulatory scenario

- 3.2.2.2 Lack of skilled healthcare professionals

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Trump administration tariffs

- 3.5.1 Impact on trade

- 3.5.1.1 Trade volume disruptions

- 3.5.1.2 Country-wise response

- 3.5.2 Impact on the industry

- 3.5.2.1 Supply-side impact (Cost of manufacturing)

- 3.5.2.1.1 Price volatility in key materials

- 3.5.2.1.2 Supply chain restructuring

- 3.5.2.1.3 Production cost implications

- 3.5.2.2 Demand-side impact (Cost to consumers)

- 3.5.2.2.1 Price transmission to end markets

- 3.5.2.2.2 Market share dynamics

- 3.5.2.2.3 Consumer response patterns

- 3.5.2.1 Supply-side impact (Cost of manufacturing)

- 3.5.3 Key companies impacted

- 3.5.4 Strategic industry responses

- 3.5.4.1 Supply chain reconfiguration

- 3.5.4.2 Pricing and product strategies

- 3.5.4.3 Policy engagement

- 3.5.5 Outlook and future considerations

- 3.5.1 Impact on trade

- 3.6 Technological landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Therapeutics

- 5.2.1 Pacemakers

- 5.2.2 Implantable cardioverter-defibrillators

- 5.2.3 Neurostimulation devices

- 5.2.4 Surgical robots

- 5.2.5 Respiratory care devices

- 5.3 Diagnostics

- 5.3.1 Patient monitoring devices

- 5.3.2 PET-CT devices

- 5.3.3 MRI scanners

- 5.3.4 Ultrasound devices

- 5.3.5 X-rays devices

- 5.3.6 CT scanners

- 5.4 Other product types

Chapter 6 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Hospitals

- 6.3 Ambulatory surgical centers

- 6.4 Clinics

- 6.5 Other end use

Chapter 7 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 Middle East and Africa

- 7.6.1 Saudi Arabia

- 7.6.2 South Africa

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 Abbott Laboratories

- 8.2 Boston Scientific

- 8.3 Carestream Health

- 8.4 Esaote

- 8.5 FUJIFILM Holdings

- 8.6 GE HealthCare

- 8.7 Koninklijke Philips

- 8.8 Lepu Medical Technology

- 8.9 Medtronic

- 8.10 MicroPort Scientific

- 8.11 Olympus

- 8.12 Samsung Electronics

- 8.13 Shenzhen Mindray Bio-Medical Electronics

- 8.14 Siemens Healthineers

- 8.15 Toshiba Medical Systems