PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1755253

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1755253

ADAS Software Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

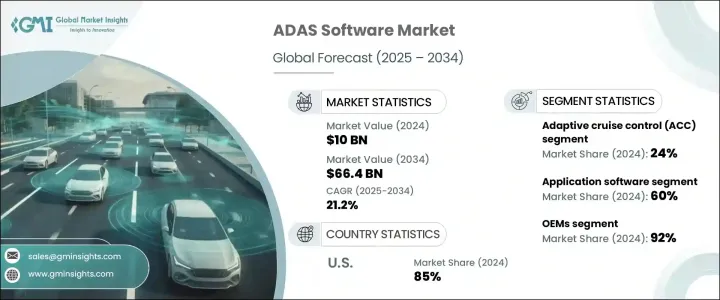

The Global ADAS Software Market was valued at USD 10 billion in 2024 and is estimated to grow at a CAGR of 21.2% to reach USD 66.4 billion by 2034. This significant expansion is largely fueled by rising consumer awareness regarding road safety and a growing appetite for vehicles equipped with automated support features. Increasing demand for functionalities such as automated lane keeping and braking assistance has made ADAS technologies a mainstream requirement in modern vehicles. In addition, technological innovations in sensor systems, including satellite, camera, and Lidar technologies, have made these systems more efficient, reliable, and accessible, ultimately enhancing overall performance while reducing operational costs.

Another major driver of market growth is the integration of artificial intelligence and machine learning into ADAS platforms. These capabilities allow vehicles to process real-time data and make predictive decisions, significantly improving situational awareness and responsiveness. With global regulatory bodies enforcing more stringent vehicle safety requirements, automotive companies are under pressure to incorporate advanced assistance systems to meet compliance. Consumers are also leaning toward semi-autonomous driving experiences, prompting a rapid adoption of sophisticated driver-assist features. As a result, the push toward higher levels of vehicle autonomy is encouraging manufacturers to invest heavily in software that can support increasingly complex driving functions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $10 Billion |

| Forecast Value | $66.4 Billion |

| CAGR | 21.2% |

The growing complexity of driver-assistance features means software plays a critical role in enabling systems like automated emergency response, smart navigation, and vehicle positioning. Automakers are focused on achieving seamless integration of ADAS software within the broader vehicle architecture. The rise in demand for intelligent, responsive systems has turned software into a differentiator in competitive vehicle offerings. Continued innovation in real-time sensor fusion and AI-driven contextual decision-making will shape the future of ADAS solutions.

By component, the ADAS software market is segmented into software platform, middleware, application software, and operating system. In 2024, the application software segment accounted for the largest market share, contributing approximately 60% of total revenue. It is also anticipated to grow at a CAGR exceeding 22% throughout the forecast period. This segment holds a critical position in the market as it enables direct interaction with vehicle sensors and algorithm-based decision-making processes. As the primary element responsible for real-time functionality, application software ensures the effective execution of advanced driver-assistance features across all vehicle types.

In terms of systems, the market is categorized into lane departure warning (LDW), adaptive cruise control (ACC), automatic emergency braking (AEB), parking assistance, blind spot detection (BSD), night vision systems, traffic sign recognition (TSR), and others. Adaptive cruise control led the market in 2024, holding a 24% revenue share. This dominance is attributed to its essential role in maintaining safe vehicle spacing and enhancing driver comfort, especially in traffic-heavy or high-speed conditions. The global preference for vehicles that offer partial automation has amplified the popularity of such systems in both urban and highway driving scenarios.

When analyzed by vehicle type, the ADAS software market is divided into commercial vehicles and passenger cars. Passenger cars dominated the market in 2024, driven by heightened demand for integrated safety and convenience technologies. This trend is especially strong in the mid-range and entry-level segments, where buyers are actively seeking vehicles with enhanced safety features. The mass integration of ADAS functionality in personal vehicles continues to be a key growth driver as automakers expand offerings to meet consumer expectations.

Based on end use, the market is split between original equipment manufacturers (OEMs) and aftermarket players. OEMs held a commanding share of around 92% in 2024. This is due to their capability to integrate ADAS software during vehicle production, which results in better optimization, increased data security, and a seamless user experience. Automakers are proactively embedding these features as standard, recognizing the growing demand for intelligent safety technologies among car buyers.

Regionally, the United States led the ADAS software market in 2024, generating approximately USD 3 billion and representing about 85% of the North American share. The growth in this region is closely tied to government safety initiatives and regulatory support for mandatory vehicle assistance features. Additionally, the focus on domestic innovation and national security has led to increased investment in homegrown ADAS technologies.

The market is also witnessing a shift toward vertical integration, as many automotive companies and Tier 1 suppliers aim to develop proprietary software ecosystems. This approach improves compatibility, security, and system control while reducing reliance on third-party developers. Another significant trend involves strategic collaborations with AI firms, semiconductor producers, and cloud service providers to strengthen R&D and accelerate innovation. These partnerships enable scalability and allow companies to adapt ADAS solutions to meet varying regulatory and road requirements across global markets.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 System

- 2.2.4 Vehicle

- 2.2.5 End use

- 2.2.6 Level of autonomy

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for autonomous and semi-autonomous vehicles

- 3.2.1.2 Increased integration of AI and machine learning

- 3.2.1.3 Technological advancements in sensors and connectivity

- 3.2.1.4 Rapid urbanization and smart mobility initiatives

- 3.2.1.5 Consumer demand for in-vehicle safety and convenience

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High development and integration costs

- 3.2.2.2 Complexity in sensor fusion and real-time processing

- 3.2.3 Market opportunities

- 3.2.3.1 Integration with electric vehicles (EVs)

- 3.2.3.2 The rise of cloud-native platforms

- 3.2.3.3 OEM-software supplier partnerships

- 3.2.3.4 AI and machine learning integration

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Patent analysis

- 3.9 Sustainability and environmental aspects

- 3.9.1 Sustainable practices

- 3.9.2 Waste reduction strategies

- 3.9.3 Energy efficiency in production

- 3.9.4 Eco-friendly initiatives

- 3.9.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 Software platform

- 5.3 Middleware

- 5.4 Application software

- 5.5 Operating system

Chapter 6 Market Estimates & Forecast, By System, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 Adaptive cruise control (ACC)

- 6.3 Lane departure warning (LDW)

- 6.4 Automatic emergency braking (AEB)

- 6.5 Blind spot detection (BSD)

- 6.6 Parking assistance

- 6.7 Traffic sign recognition (TSR)

- 6.8 Night vision system

- 6.9 Others

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 (USD Million)

- 7.1 Key trends

- 7.2 Passenger cars

- 7.2.1 Hatchbacks

- 7.2.2 Sedans

- 7.2.3 SUVs (Sport utility vehicles)

- 7.2.4 MPVs (Multi-purpose vehicles)

- 7.3 Commercial vehicles

- 7.3.1 Light commercial vehicles (LCVs)

- 7.3.2 Medium commercial vehicles (HCVs)

- 7.3.3 Heavy commercial vehicles (HCVs)

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 (USD Million)

- 8.1 Key trends

- 8.2 OEM (Original equipment manufacturers)

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Level of autonomy, 2021 - 2034 (USD Million)

- 9.1 Key trends

- 9.2 Level 1 (Driver assistance)

- 9.3 Level 2 (Partial automation)

- 9.4 Level 3 (Conditional automation)

- 9.5 Level 4 (High automation)

- 9.6 Level 5 (Full automation)

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Singapore

- 10.4.7 Malaysia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Ambarella

- 11.2 Aptiv

- 11.3 Baidu Apollo

- 11.4 Bosch

- 11.5 Continental

- 11.6 Innoviz Technologies

- 11.7 Luminar Technologies

- 11.8 Magna International

- 11.9 Mobileye (Intel)

- 11.10 Nvidia

- 11.11 NXP Semiconductors

- 11.12 Qualcomm

- 11.13 Renesas Electronics

- 11.14 Sony

- 11.15 Tesla

- 11.16 Valeo

- 11.17 Velodyne Lidar (Ouster)

- 11.18 Waymo (Alphabet)

- 11.19 XPeng

- 11.20 ZF Friedrichshafen