PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1755267

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1755267

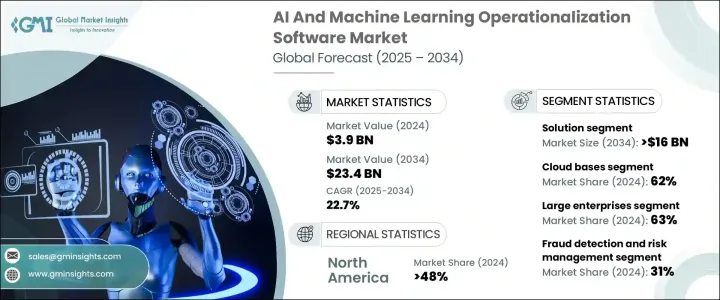

AI and Machine Learning Operationalization Software Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

The Global AI and Machine Learning Operationalization Software Market was valued at USD 3.9 billion in 2024 and is estimated to grow at a CAGR of 22.7% to reach USD 23.4 billion by 2034, propelled by increasing demand for data-driven decision-making and the growing need for scalable, automated model deployment across enterprises. Organizations are rapidly adopting these solutions to streamline AI workflows, reduce operational friction, ensure regulatory compliance, and accelerate innovation-especially within sectors like manufacturing, finance, healthcare, and e-commerce.

As artificial intelligence and machine learning applications become integral to core business operations, companies seek robust platforms to deploy, monitor, and maintain models in real-time. The inefficiency of manual model management is driving the market toward platforms that offer full lifecycle support for AI at scale, ensuring consistent accuracy and speed across operations. Enterprises seek platforms that maintain consistency, resilience, and flexibility across evolving operational landscapes. There's a clear shift toward tools that simplify the complexities of machine learning workflows, allowing organizations to move from experimentation to full-scale implementation efficiently. Businesses are now seeking platforms that abstract technical hurdles and streamline processes such as data ingestion, feature engineering, model validation, and post-deployment monitoring. This transition is reducing reliance on large data science teams and empowering cross-functional users-from analysts to IT teams-to collaborate on AI initiatives.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.9 Billion |

| Forecast Value | $23.4 Billion |

| CAGR | 22.7% |

In 2024, the solutions segment generated USD 2.3 billion and will reach USD 16 billion by 2034. This momentum underscores the increasing reliance on full-cycle AI software that streamlines everything from data preparation to real-time model monitoring. Enterprises are turning to these solutions to accelerate deployment timelines and drive value faster, particularly in environments where in-house data science expertise is limited. By offering automation and scalability, these platforms are becoming essential for business units across finance, operations, marketing, and customer experience.

Cloud-based deployment segment held a 62% share in 2024, driven by its adaptability, cost-effectiveness, and seamless integration with existing digital ecosystems. Cloud infrastructure allows enterprises to centralize and coordinate AI functions-like model versioning, governance, and collaboration-within distributed teams, ensuring consistent performance and faster iteration cycles. Its role in democratizing AI access has made it the preferred choice for scaling operations across diverse business environments.

North America AI and Machine Learning Operationalization Software Market held a 48% share in 2024, bolstered by mature AI implementation, robust cloud adoption, and continuous investment in AI R&D. In the U.S., heightened focus on regulatory compliance, operational transparency, and competitive agility is prompting companies to invest heavily in operationalizing AI at enterprise scale.

DataRobot, Google Cloud, IBM, H2O.ai, Microsoft, SAS Institute, Amazon Web Services (AWS), Dataiku, Databricks, C3.ai. Leading firms invest heavily in platform integration, user interface improvements, and cloud-native functionality. Many focus on building unified environments that offer full-lifecycle AI support-spanning model training, deployment, governance, and monitoring. Additionally, companies are forming strategic alliances with cloud providers and enterprise software vendors to expand reach and enhance functionality. Investments in automated MLOps capabilities, no-code/low-code environments, and prebuilt AI workflows enable wider adoption across non-technical teams.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariff analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Supplier landscape

- 3.3.1 Manufacturers

- 3.3.2 Component suppliers

- 3.3.3 Technology providers

- 3.3.4 Service providers

- 3.3.5 End use

- 3.4 Profit margin analysis

- 3.5 Technology & innovation landscape

- 3.6 Key news & initiatives

- 3.7 Patent analysis

- 3.8 Regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Increasing adoption of ai/ml across industries

- 3.9.1.2 Need for scalable and automated ml workflows

- 3.9.1.3 Rise of cloud-native ai solutions

- 3.9.1.4 Pressure to generate business value from ai investments

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 Lack of model transparency and explainability

- 3.9.2.2 Integration complexity with existing infrastructure

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Software

- 5.2.1 Model development and training software

- 5.2.2 Model deployment software

- 5.2.3 Model monitoring and management software

- 5.2.4 Data management software

- 5.3 Services

- 5.3.1 Professional services

- 5.3.2 Managed services

Chapter 6 Market Estimates & Forecast, By Deployment Mode, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 On-premises

- 6.3 Cloud based

Chapter 7 Market Estimates & Forecast, By Organization Size, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Small and medium enterprises (SMEs)

- 7.3 Large enterprises

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Predictive analytics

- 8.3 Fraud detection and risk management

- 8.4 Customer experience management

- 8.5 Natural language processing (NLP) and text analytics

- 8.6 Others

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 Banking, financial services, and insurance (BFSI)

- 9.3 Healthcare and life sciences

- 9.4 Retail and e-commerce

- 9.5 IT and telecommunications

- 9.6 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Alteryx

- 11.2 Amazon Web Services (AWS)

- 11.3 Aporia

- 11.4 C3.ai

- 11.5 Cloudera

- 11.6 Databricks

- 11.7 Dataiku

- 11.8 DataRobot

- 11.9 Domino Data Lab

- 11.10 Google Cloud

- 11.11 H2O.ai

- 11.12 IBM Watson

- 11.13 Infosys Nia

- 11.14 Microsoft Azure

- 11.15 Oracle

- 11.16 Palantir Technologies

- 11.17 Qlik

- 11.18 RapidMiner

- 11.19 SAS Institute

- 11.20 Seldon